Viking has been on fire lately. In the past six months alone, the company’s stock price has rocketed 44.7%, setting a new 52-week high of $104.60 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Viking, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Viking Will Underperform?

Despite the momentum, we’re cautious about Viking. Here are three reasons why VIK doesn’t excite us, plus one stock we’d rather own.

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend.

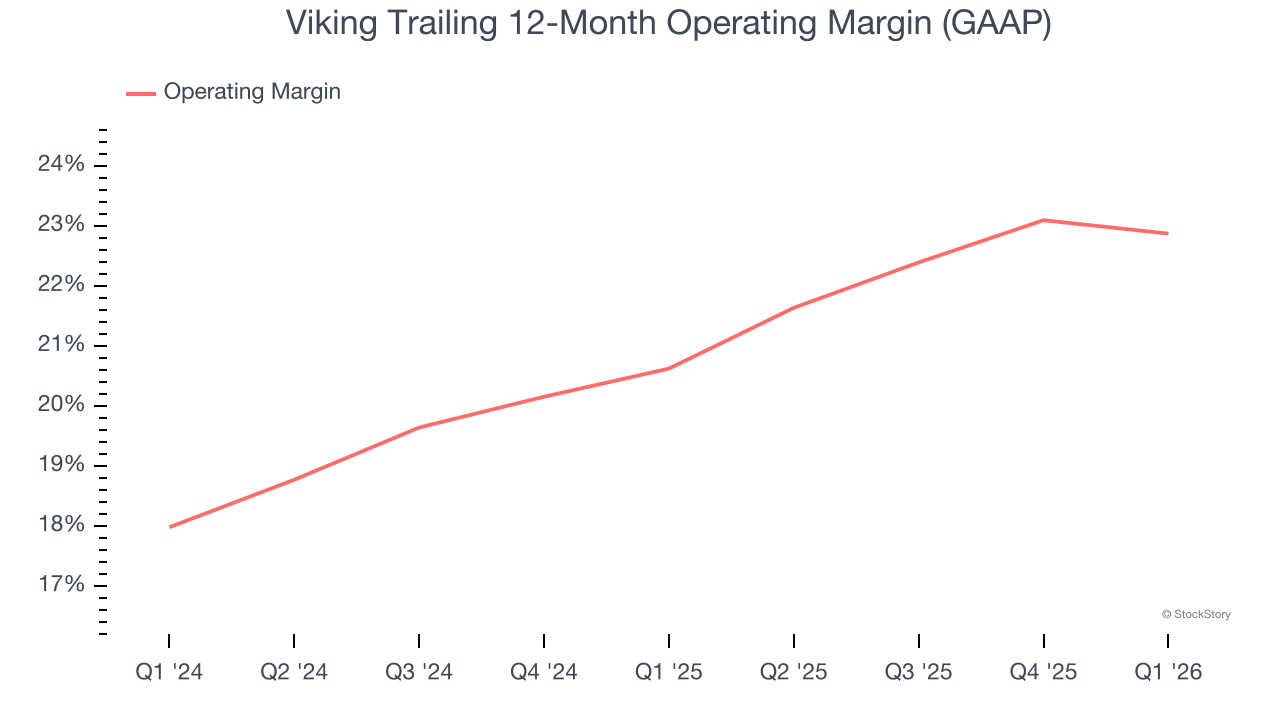

2. Weak Operating Margin Could Cause Trouble

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Viking’s operating margin has risen over the last 12 months and averaged 21.9% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

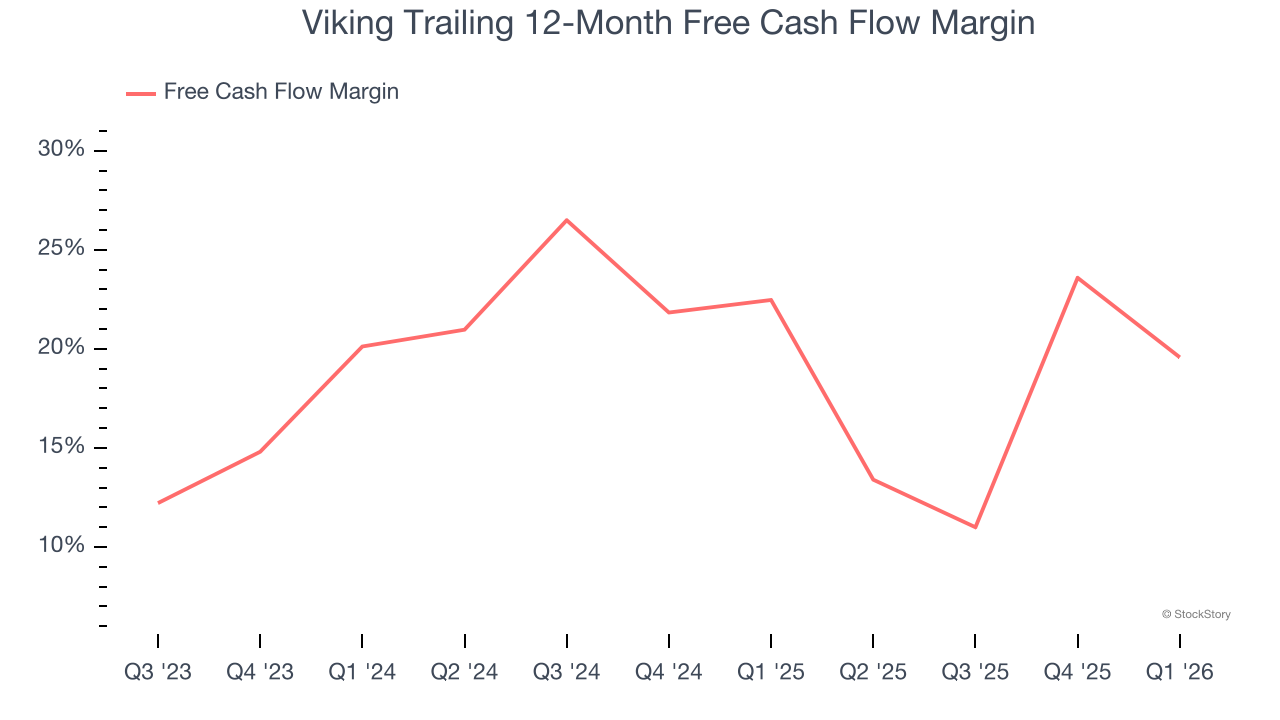

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Viking has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 20.9%, below what we’d expect for a consumer discretionary business.

Final Judgment

Viking falls short of our quality standards. After the recent rally, the stock trades at 31.4× forward P/E (or $104.60 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at a dominant aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.