The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Boyd Gaming (NYSE: BYD) and the rest of the consumer discretionary - casino operator stocks fared in Q1.

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Casino operators run gaming resorts and facilities that generate revenue from gambling, hospitality, food and beverage, and entertainment offerings. Tailwinds include pent-up travel demand, expansion into new jurisdictions legalizing gaming, and growing interest in integrated resort developments in Asia and the Middle East. However, the industry faces notable headwinds: heavy regulatory and licensing requirements limit operational flexibility, capital expenditure for property development and renovation is substantial, and revenue is highly sensitive to macroeconomic conditions and consumer confidence. Rising competition from online gambling platforms, regional saturation in mature markets, and geopolitical risks in key international jurisdictions add further uncertainty.

The 9 consumer discretionary - casino operator stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 1.6%.

Luckily, consumer discretionary - casino operator stocks have performed well with share prices up 11.3% on average since the latest earnings results.

Boyd Gaming (NYSE: BYD)

Run by the Boyd family, Boyd Gaming (NYSE: BYD) is a diversified operator of gaming entertainment properties across the United States, offering casino games, hotel accommodations, and dining.

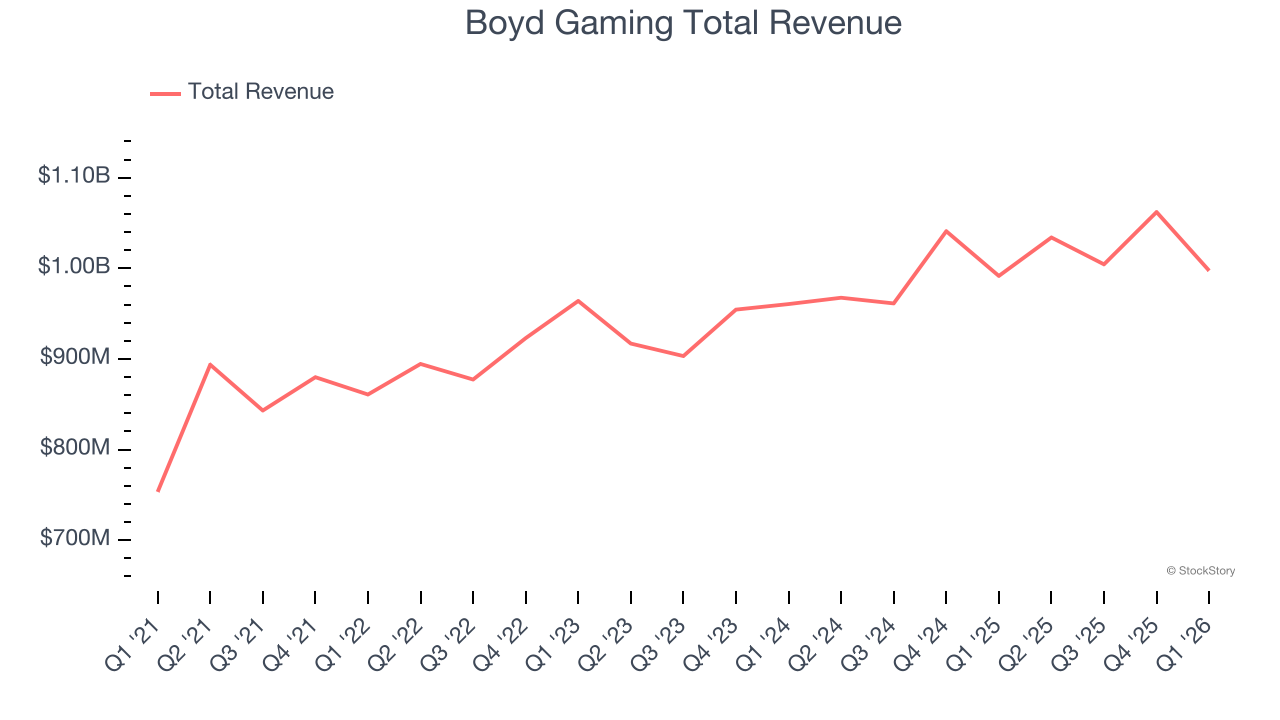

Boyd Gaming reported revenues of $997.4 million, flat year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with a miss of analysts’ adjusted operating income and EPS estimates.

Keith Smith, President and Chief Executive Officer of Boyd Gaming, said: "Our first-quarter results reflect the benefits of our diversified business, our successful focus on operating efficiencies and our ongoing capital investment program. On a property-level basis, we achieved year-over-year revenue and Adjusted EBITDAR growth, as property margins once again exceeded 39%. These results were supported by continued growth in play from both core and retail customers on a Companywide basis, driven by broad-based strength in our Midwest & South segment. During the quarter we continued to invest in enhancing our properties and building our development pipeline. We opened Cadence Crossing Casino, our newest Las Vegas Locals property, and continued development of our $750 million resort in Virginia. We also secured regulatory approval for our proposed expansion and modernization of our Par-A-Dice property in Illinois, and plan to begin construction on this project next year. At the same time, we maintained our robust program of returning capital to our shareholders, with nearly $170 million in share repurchases and dividends during the first quarter. Looking ahead, we believe that our strong balance sheet, diversified portfolio, balanced approach to capital allocation and experienced management team all position us well to continue creating long-term value for our shareholders."

Boyd Gaming delivered the slowest revenue growth of the whole group. Unsurprisingly, the stock is down 4.7% since reporting and currently trades at $84.96.

Read our full report on Boyd Gaming here, it’s free.

Best Q1: Monarch (NASDAQ: MCRI)

Established in 1993, Monarch (NASDAQ: MCRI) operates luxury casinos and resorts, offering high-end gaming, dining, and hospitality experiences.

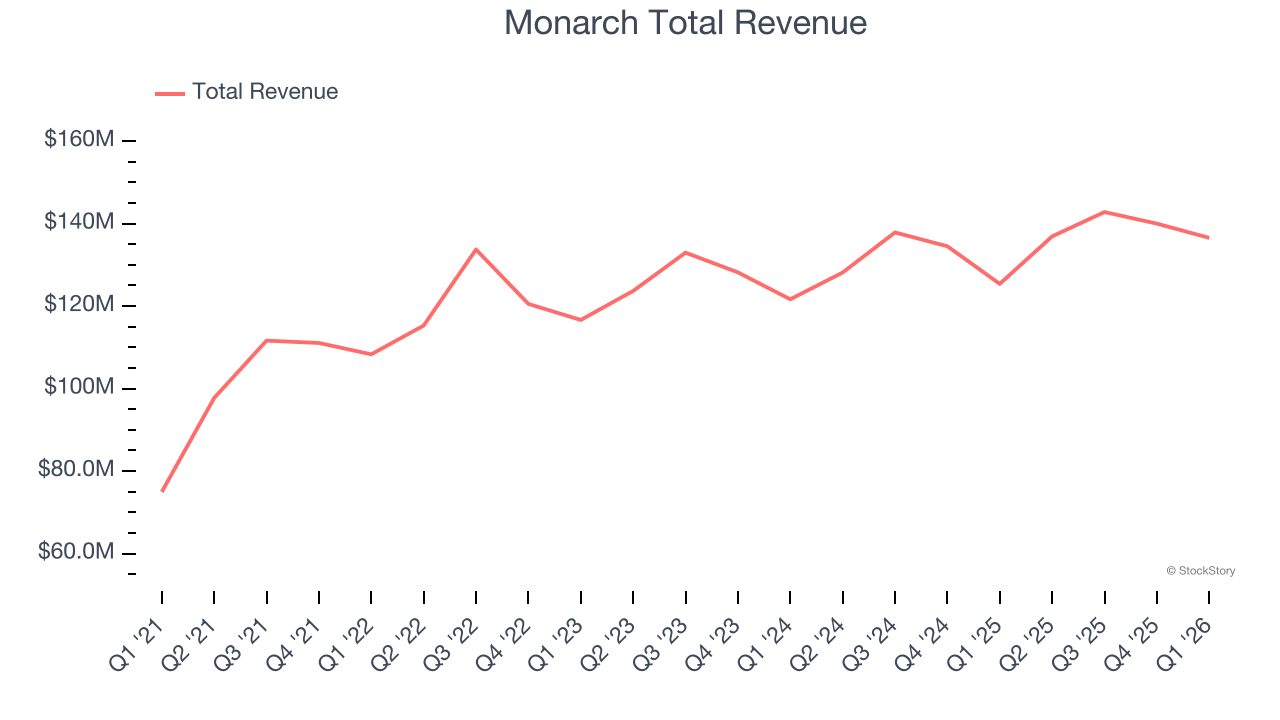

Monarch reported revenues of $136.6 million, up 8.9% year on year, outperforming analysts’ expectations by 5.2%. The business had an exceptional quarter with a beat of analysts’ EPS and adjusted operating income estimates.

Monarch achieved the biggest analyst estimate beat among its peers. The market seems happy with the results as the stock is up 20.7% since reporting. It currently trades at $118.98.

Is now the time to buy Monarch? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: MGM Resorts (NYSE: MGM)

Operating several properties on the Las Vegas Strip, MGM Resorts (NYSE: MGM) is a global hospitality and entertainment company known for its resorts and casinos.

MGM Resorts reported revenues of $4.45 billion, up 4.2% year on year, exceeding analysts’ expectations by 2%. Still, it was a softer quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Interestingly, the stock is up 23.5% since the results and currently trades at $48.50.

Read our full analysis of MGM Resorts’s results here.

Caesars Entertainment (NASDAQ: CZR)

Formerly Eldorado Resorts, Caesars Entertainment (NASDAQ: CZR) is a global gaming and hospitality company operating numerous casinos, hotels, and resort properties.

Caesars Entertainment reported revenues of $2.87 billion, up 2.7% year on year. This result surpassed analysts’ expectations by 0.6%. Zooming out, it was a slower quarter as it produced a significant miss of analysts’ EPS and EBITDA estimates.

The stock is up 6.9% since reporting and currently trades at $29.20.

Read our full, actionable report on Caesars Entertainment here, it’s free.

Wynn Resorts (NASDAQ: WYNN)

Founded by the former Mirage Resorts CEO, Wynn Resorts (NASDAQ: WYNN) is a global developer and operator of high-end hotels and casinos, known for its luxurious properties and premium guest services.

Wynn Resorts reported revenues of $1.86 billion, up 9.2% year on year. This number topped analysts’ expectations by 1.8%. More broadly, it was a slower quarter as it logged a miss of analysts’ EBITDA estimates.

The stock is down 1.8% since reporting and currently trades at $104.92.

Read our full, actionable report on Wynn Resorts here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.