Over the last six months, Molson Coors’s shares have sunk to $38.94, producing a disappointing 15.8% loss - a stark contrast to the S&P 500’s 10.9% gain. This might have investors contemplating their next move.

Is now the time to buy Molson Coors, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Molson Coors Will Underperform?

Even though the stock has become cheaper, we don’t have much confidence in Molson Coors. Here are three reasons we avoid TAP, plus one stock we’d rather own.

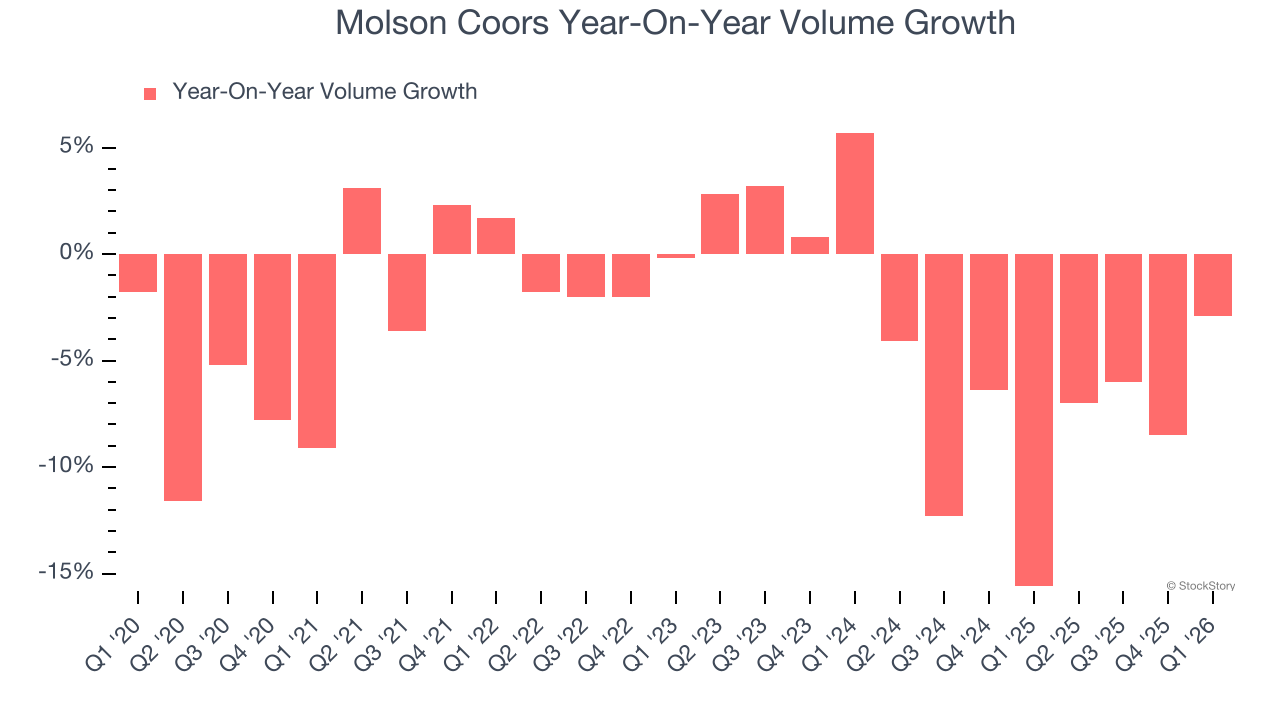

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Molson Coors’s average quarterly sales volumes have shrunk by 7.9% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

2. Shrinking Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Molson Coors’s operating margin decreased by 34.6 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Molson Coors’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 20.2%.

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Molson Coors historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.6%, lower than the typical cost of capital (how much it costs to raise money) for consumer staples companies.

Final Judgment

We see the value of companies helping consumers, but in the case of Molson Coors, we’re out. Following the recent decline, the stock trades at 8.3× forward P/E (or $38.94 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Molson Coors

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.