Since October 2025, Zeta Global has been in a holding pattern, posting a small loss of 1.9% while floating around $17.49. The stock also fell short of the S&P 500’s 5.4% gain during that period.

Does this present a buying opportunity for ZETA? Or is its underperformance reflective of its story and business quality? Find out in our full research report, it’s free.

Why Are We Positive On Zeta Global?

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE: ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

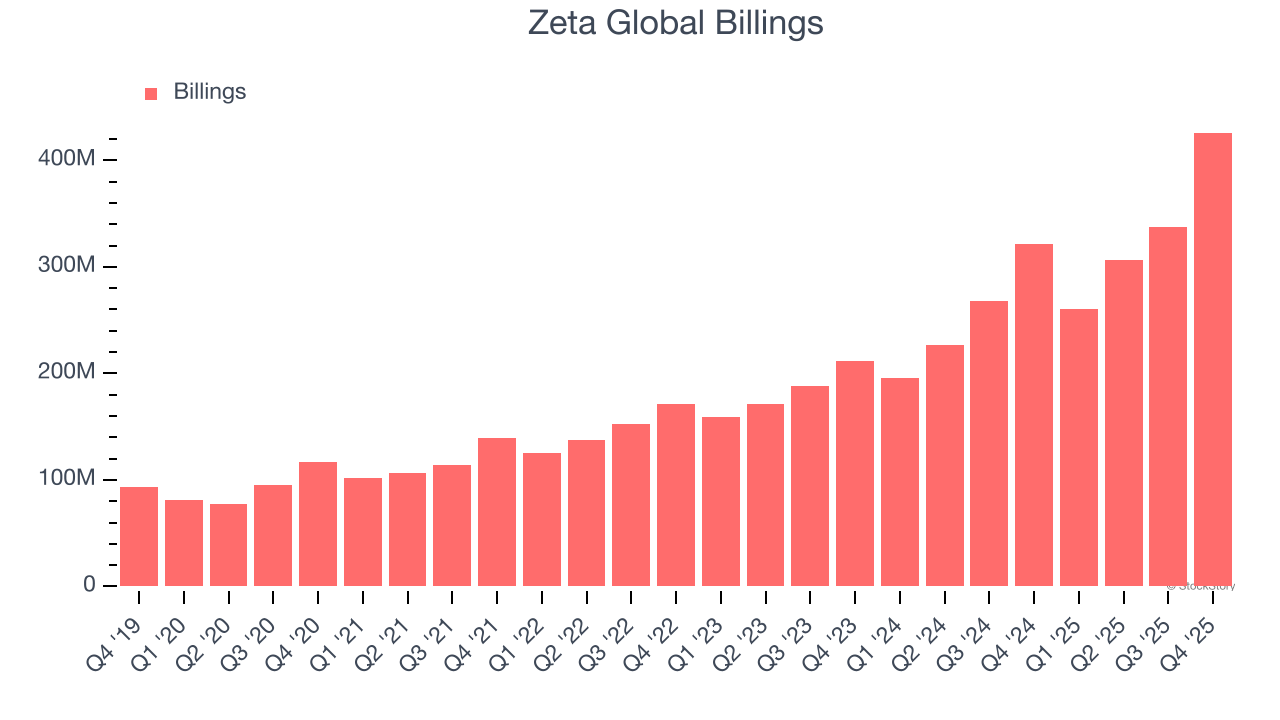

1. Billings Surge, Boosting Cash On Hand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zeta Global’s billings punched in at $426 million in Q4, and over the last four quarters, its year-on-year growth averaged 31.5%. This performance was fantastic, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Zeta Global’s revenue to rise by 34.7%, close to its 28.8% annualized growth for the past five years. This projection is eye-popping and suggests the market is baking in success for its products and services.

3. Customer Acquisition Costs Are Recovered in Record Time

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Zeta Global is extremely efficient at acquiring new customers, and its CAC payback period checked in at 5.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Zeta Global more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Final Judgment

These are just a few reasons why we think Zeta Global is a high-quality business. With its shares underperforming the market lately, the stock trades at 2.3× forward price-to-sales (or $17.49 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.