BJ's has had an impressive run over the past six months as its shares have beaten the S&P 500 by 17%. The stock now trades at $38.07, marking a 22.1% gain. This run-up might have investors contemplating their next move.

Is there a buying opportunity in BJ's, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think BJ's Will Underperform?

Despite the momentum, we don't have much confidence in BJ's. Here are three reasons there are better opportunities than BJRI and a stock we'd rather own.

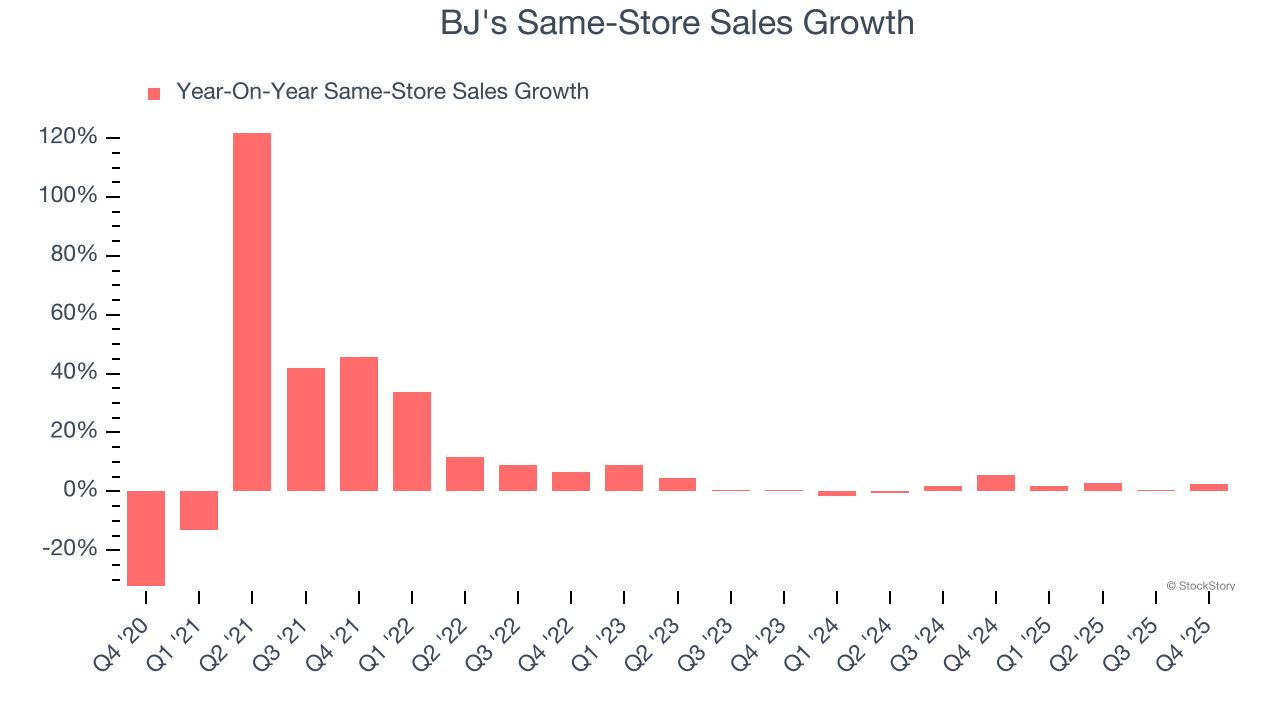

1. Same-Store Sales Falling Behind Peers

Same-store sales is an industry measure of whether revenue is growing at existing restaurants, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

BJ’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.6% per year.

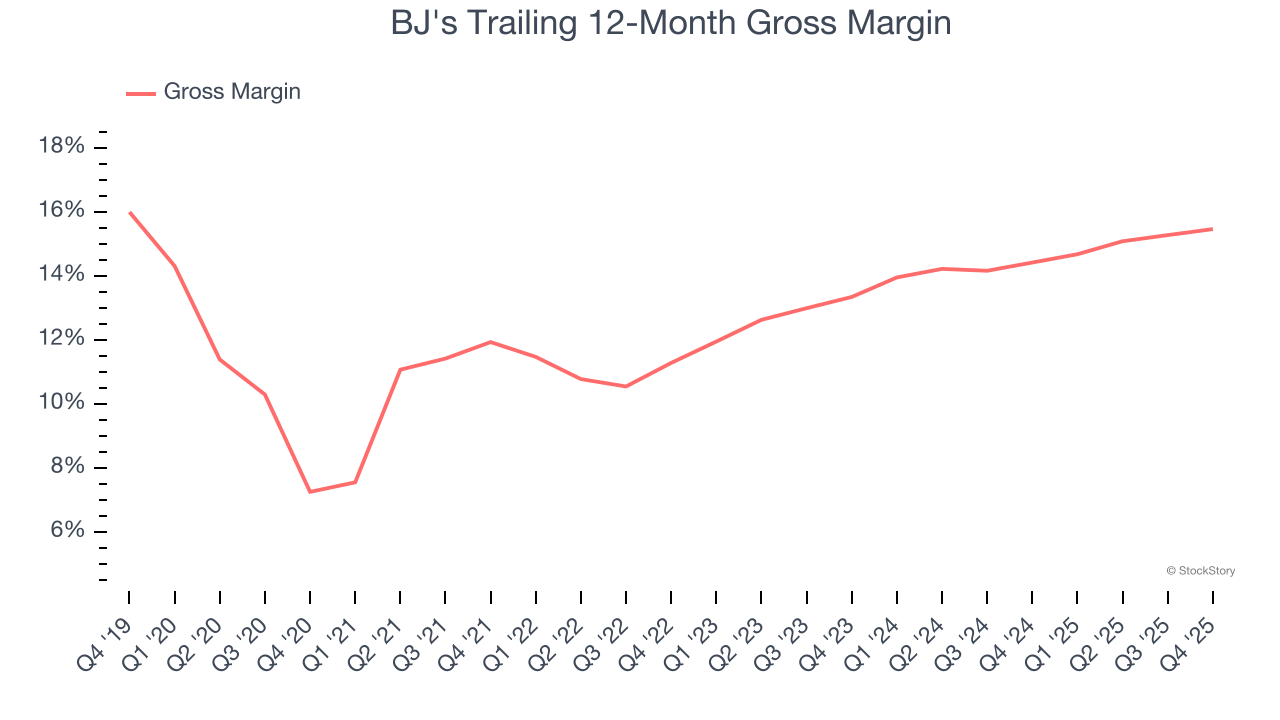

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margins tell us how much money a restaurant gets to keep after paying for the direct costs of the meals it sells, like ingredients, and indicate its level of pricing power.

BJ's has bad unit economics for a restaurant company, signaling it operates in a competitive market and has little room for error if demand unexpectedly falls. As you can see below, it averaged a 14.9% gross margin over the last two years. Said differently, BJ's had to pay a chunky $85.06 to its suppliers for every $100 in revenue.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

BJ's historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.5%, lower than the typical cost of capital (how much it costs to raise money) for restaurant companies.

Final Judgment

BJ's falls short of our quality standards. With its shares outperforming the market lately, the stock trades at 16.5× forward P/E (or $38.07 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere. We’d recommend looking at a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of BJ's

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.