What a fantastic six months it’s been for Patterson-UTI. Shares of the company have skyrocketed 84.1%, hitting $10.46. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now still a good time to buy PTEN? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does Patterson-UTI Spark Debate?

Operating 135 Tier-1 super-spec rigs that can handle the industry's most demanding drilling projects, Patterson-UTI (NASDAQ: PTEN) provides contract drilling rigs, hydraulic fracturing, and drill bits to oil and gas operators.

Two Things to Like:

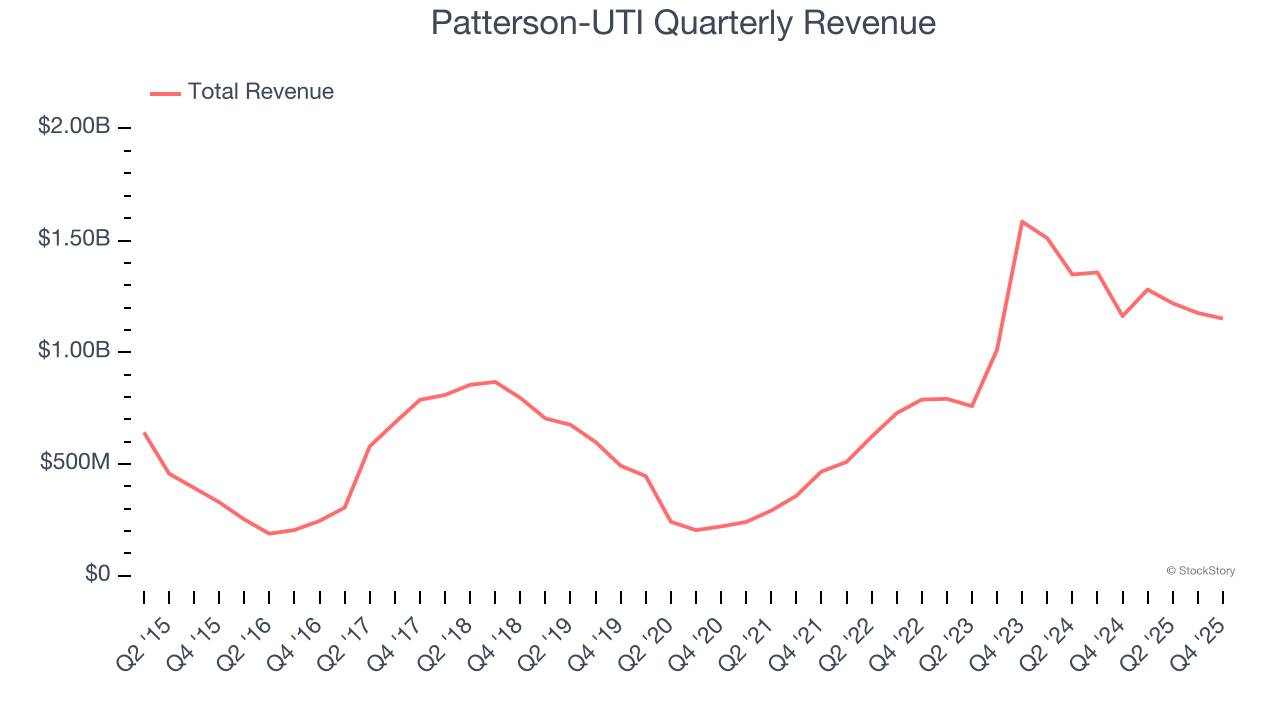

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Thankfully, Patterson-UTI’s 34.1% annualized revenue growth over the last five years was incredible. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Patterson-UTI’s $4.83 billion of revenue in the last year is mid-sized for the industry.

One Reason to be Careful:

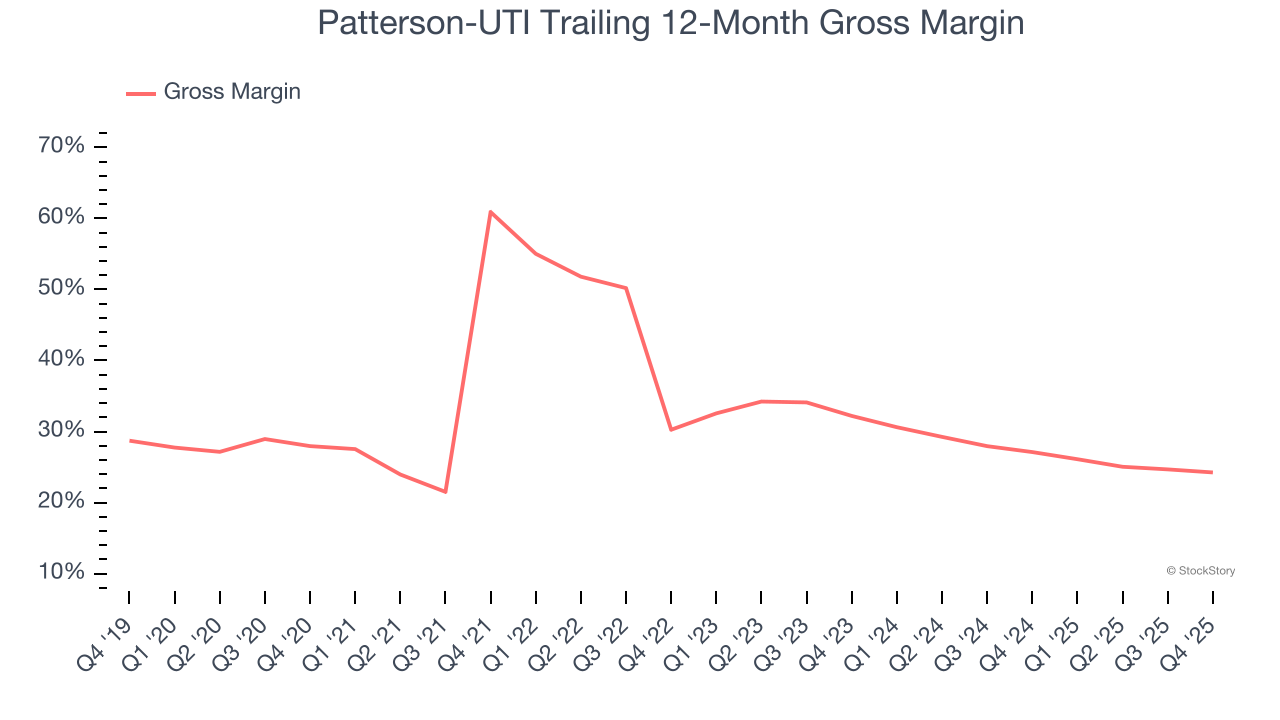

Low Gross Margin Reveals Weak Structural Profitability

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Patterson-UTI, which averaged 30.5% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

Final Judgment

Patterson-UTI’s positive characteristics outweigh the negatives, and after the recent rally, the stock trades at 5.8× forward EV-to-EBITDA (or $10.46 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Patterson-UTI

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.