Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at Select Medical (NYSE: SEM) and its peers.

The outpatient and specialty care industry delivers targeted medical services in non-hospital settings that are often cost-effective compared to inpatient alternatives. This means that they are more desired as rising healthcare costs and ways to combat them become more and more top-of-mind. Outpatient and specialty care providers boast revenue streams that are stable due to the recurring nature of treatment for chronic conditions and long-term patient relationships. However, their reliance on government reimbursement programs like Medicare means stroke-of-the-pen risk. Additionally, scaling a network of facilities can be capital-intensive with uneven return profiles amid competition from integrated healthcare systems. Looking ahead, the industry is positioned to grow as demand for outpatient services expands, driven by aging populations, a rising prevalence of chronic diseases, and a shift toward value-based care models. Tailwinds include advancements in medical technology that support more complex procedures in outpatient settings and the increasing focus on preventive care, which can be aided by data and AI. However, headwinds such as reimbursement rate cuts, labor shortages, and the financial strain of digitization may temper growth.

The 7 outpatient & specialty care stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

While some outpatient & specialty care stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.7% since the latest earnings results.

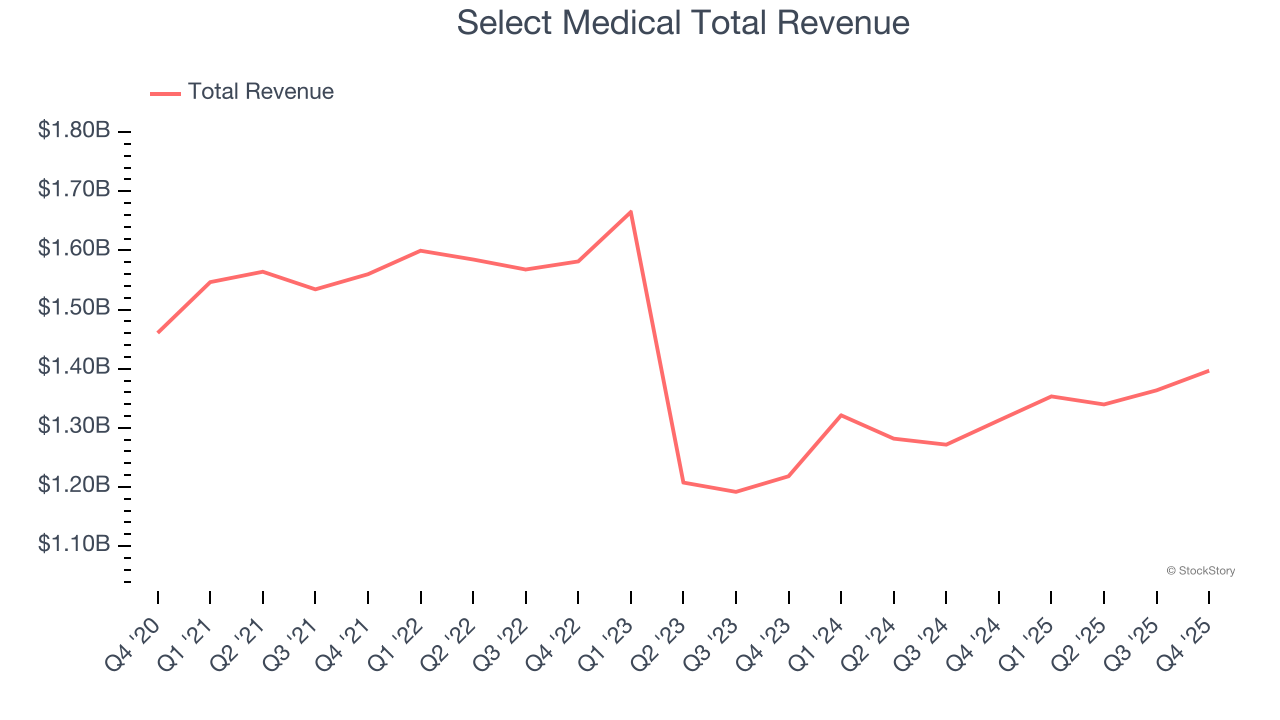

Select Medical (NYSE: SEM)

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE: SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

Select Medical reported revenues of $1.40 billion, up 6.4% year on year. This print exceeded analysts’ expectations by 2.3%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ full-year EPS guidance estimates and a significant miss of analysts’ EPS estimates.

Select Medical achieved the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 1.2% since reporting and currently trades at $16.27.

Read our full report on Select Medical here, it’s free.

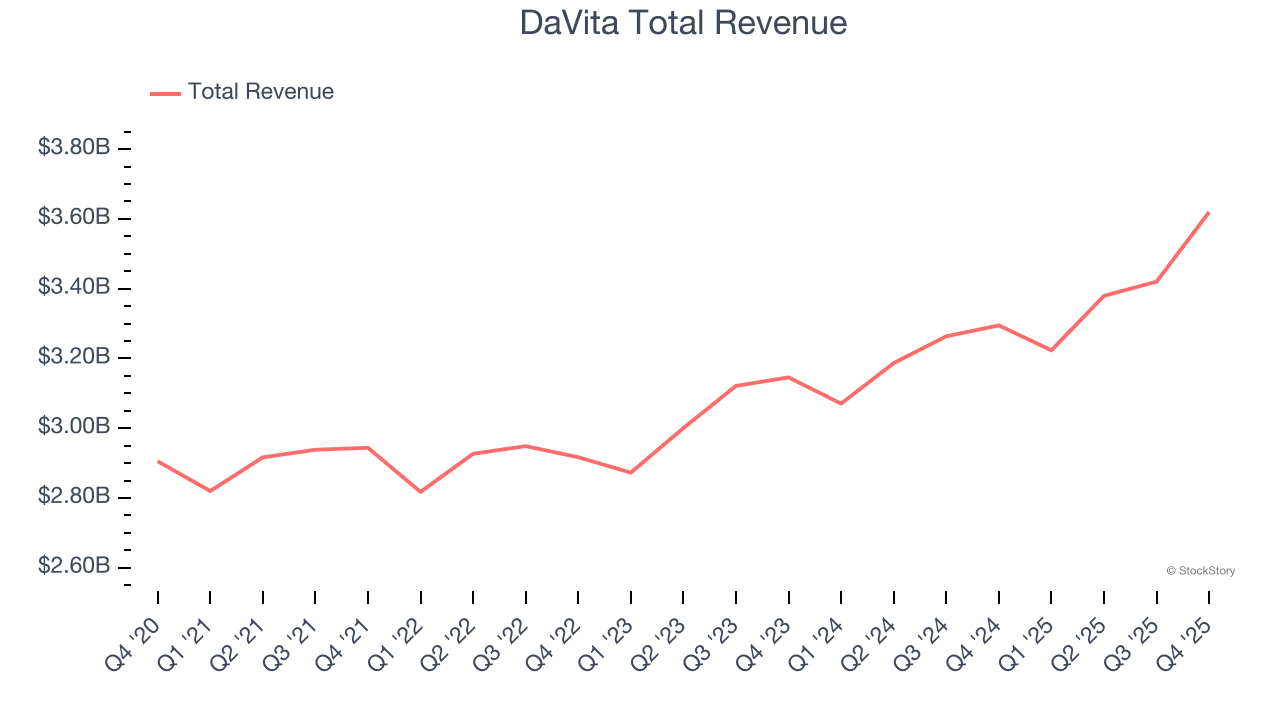

Best Q4: DaVita (NYSE: DVA)

With over 2,600 dialysis centers across the United States and a presence in 13 countries, DaVita (NYSE: DVA) operates a network of dialysis centers providing treatment and care for patients with chronic kidney disease and end-stage kidney disease.

DaVita reported revenues of $3.62 billion, up 9.9% year on year, outperforming analysts’ expectations by 3.2%. The business had a very strong quarter with an impressive beat of analysts’ full-year EPS guidance estimates and a solid beat of analysts’ revenue estimates.

The market seems happy with the results as the stock is up 41.7% since reporting. It currently trades at $157.51.

Is now the time to buy DaVita? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Surgery Partners (NASDAQ: SGRY)

With more than 180 locations across 33 states serving as alternatives to traditional hospital settings, Surgery Partners (NASDAQ: SGRY) operates a national network of outpatient surgical facilities including ambulatory surgery centers and short-stay surgical hospitals.

Surgery Partners reported revenues of $885 million, up 2.4% year on year, exceeding analysts’ expectations by 1.9%. Still, it was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EBITDA guidance missing analysts’ expectations significantly.

Surgery Partners delivered the slowest revenue growth and weakest full-year guidance update in the group. As expected, the stock is down 24.4% since the results and currently trades at $12.

Read our full analysis of Surgery Partners’s results here.

LifeStance Health Group (NASDAQ: LFST)

With over 6,600 licensed mental health professionals treating more than 880,000 patients annually, LifeStance Health (NASDAQ: LFST) provides outpatient mental health services through a network of clinicians offering psychiatric evaluations, psychological testing, and therapy across 33 states.

LifeStance Health Group reported revenues of $382.2 million, up 17.4% year on year. This number surpassed analysts’ expectations by 1%. It was a very strong quarter as it also produced a beat of analysts’ EPS estimates and full-year EBITDA guidance beating analysts’ expectations.

LifeStance Health Group achieved the fastest revenue growth among its peers. The stock is down 9.6% since reporting and currently trades at $6.46.

Read our full, actionable report on LifeStance Health Group here, it’s free.

Encompass Health (NYSE: EHC)

With a network of 161 specialized facilities across 37 states and Puerto Rico, Encompass Health (NYSE: EHC) operates inpatient rehabilitation hospitals that help patients recover from strokes, hip fractures, and other debilitating conditions.

Encompass Health reported revenues of $1.54 billion, up 9.9% year on year. This result met analysts’ expectations. Taking a step back, it was a satisfactory quarter as it also produced an impressive beat of analysts’ full-year EPS guidance estimates but full-year revenue guidance meeting analysts’ expectations.

Encompass Health had the weakest performance against analyst estimates among its peers. The stock is down 2.1% since reporting and currently trades at $97.51.

Read our full, actionable report on Encompass Health here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.