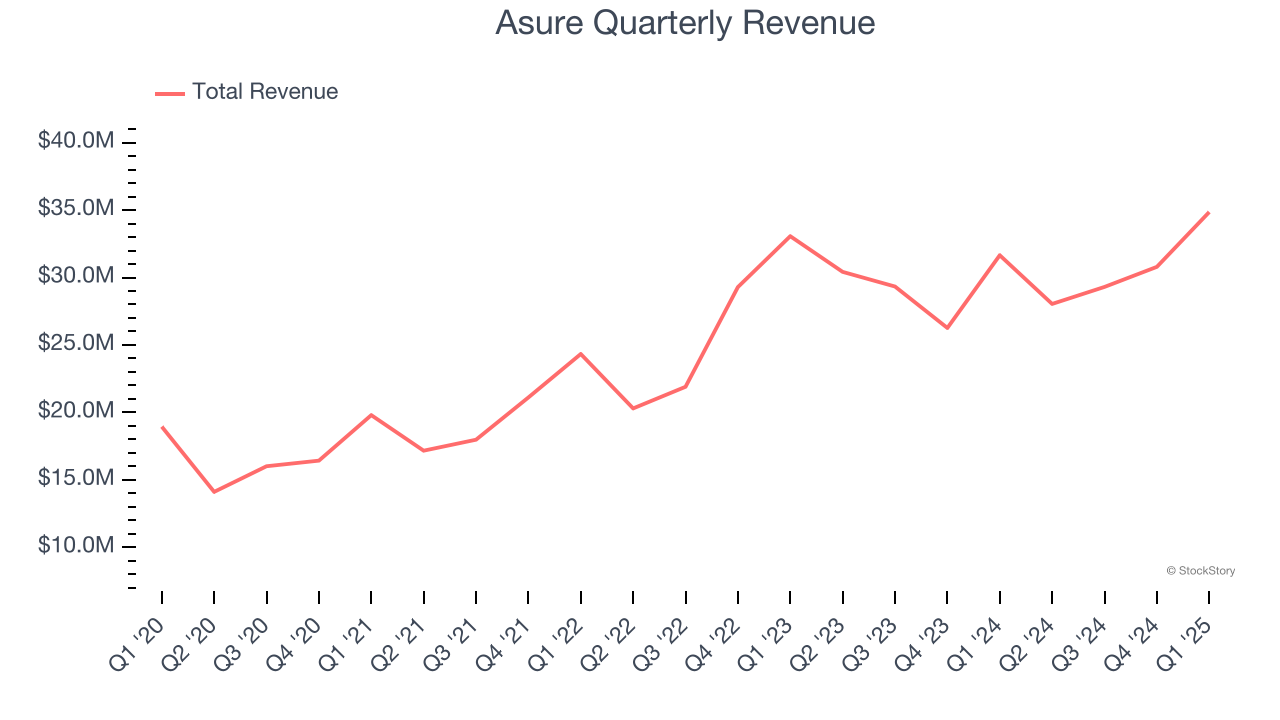

Online payroll and human resource software provider Asure (NASDAQ: ASUR) announced better-than-expected revenue in Q1 CY2025, with sales up 10.1% year on year to $34.85 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $31 million was less impressive, coming in 2.2% below expectations. Its GAAP loss of $0.09 per share was 40.6% below analysts’ consensus estimates.

Is now the time to buy Asure? Find out by accessing our full research report, it’s free.

Asure (ASUR) Q1 CY2025 Highlights:

- Revenue: $34.85 million vs analyst estimates of $34.25 million (10.1% year-on-year growth, 1.7% beat)

- EPS (GAAP): -$0.09 vs analyst expectations of -$0.06 (miss)

- Adjusted EBITDA: $7.32 million vs analyst estimates of $6.55 million (21% margin, 11.7% beat)

- The company reconfirmed its revenue guidance for the full year of $136 million at the midpoint

- EBITDA guidance for the full year is $31.96 million at the midpoint, above analyst estimates of $31.48 million

- Operating Margin: -5.8%, down from -1.4% in the same quarter last year

- Free Cash Flow Margin: 5.2%, down from 23.1% in the previous quarter

- Market Capitalization: $275.9 million

“We are excited to be off to a great start to 2025 with healthy results for our first quarter of 2025 with our revenues increasing 10% from the prior year first quarter. Our results were driven by strong performance coming from our Payroll Tax Management and initial contribution from our recently acquired product offerings,” said Asure Chairman and CEO Pat Goepel.

Company Overview

Created from the merger of two small workforce management companies in 2007, Asure (NASDAQ: ASUR) provides cloud based payroll and HR software for small and medium-sized businesses (SMBs).

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Asure grew its sales at a 15.1% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, Asure reported year-on-year revenue growth of 10.1%, and its $34.85 million of revenue exceeded Wall Street’s estimates by 1.7%. Company management is currently guiding for a 10.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.7% over the next 12 months, a slight deceleration versus the last three years. Despite the slowdown, this projection is above average for the sector and implies the market is baking in some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Asure is extremely efficient at acquiring new customers, and its CAC payback period checked in at 10.5 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from Asure’s Q1 Results

We were impressed by how significantly Asure blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed significantly and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.8% to $9.40 immediately following the results.

So should you invest in Asure right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.