The U.S. stock market has commenced December 2025 on a cautious note, with futures for the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite all pointing lower on the first trading day of the month. This early downturn signals a shift in investor sentiment, following a robust close to November, as market participants grapple with a confluence of macroeconomic factors, impending economic data releases, and a notable dip in the cryptocurrency market. The "risk-off" mood is particularly pronounced in technology and crypto-related assets, setting a tentative tone for the traditionally strong year-end trading period.

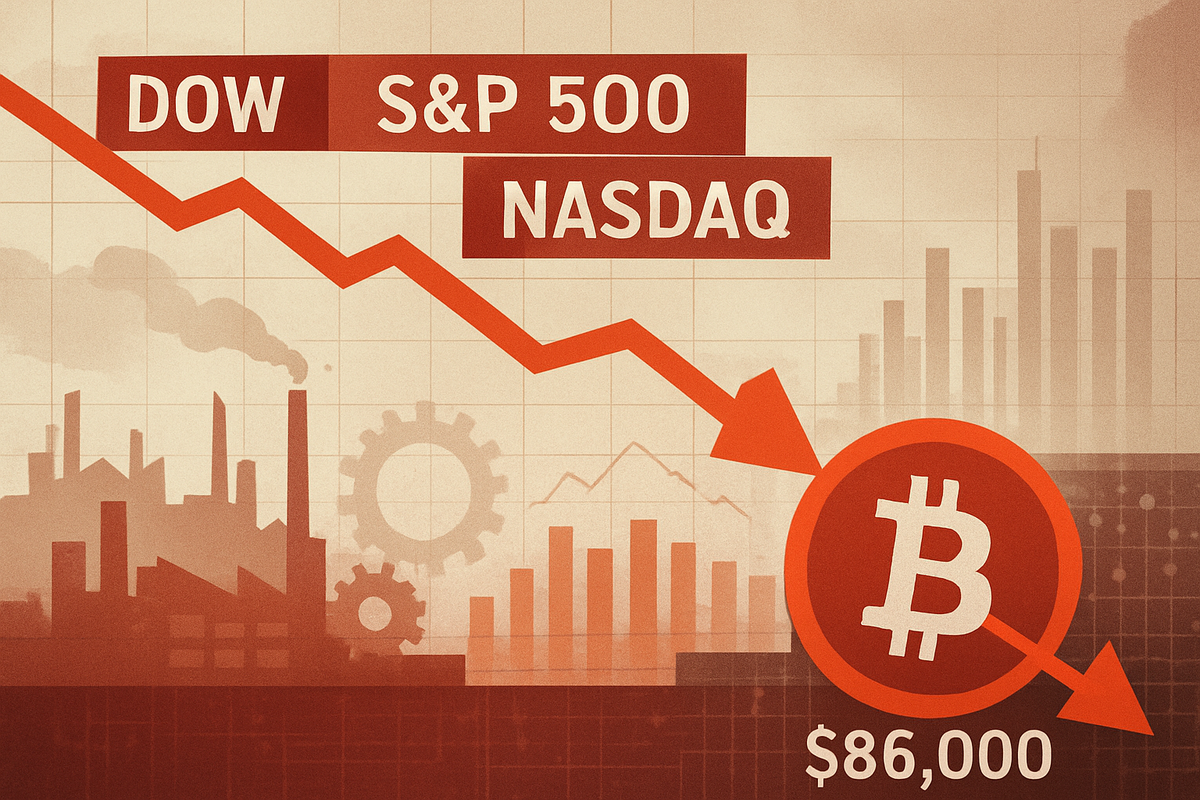

This initial deceleration comes as investors keenly await crucial manufacturing data, which is expected to offer fresh insights into the health of the global economy and potentially influence the Federal Reserve's monetary policy decisions. Adding to the market's unease, Bitcoin, the world's largest cryptocurrency, has experienced a significant retreat, trading below the $87,000 mark. This decline is reverberating through firms with substantial exposure to digital assets, further contributing to the cautious start to the new month.

Market Indices Face Headwinds Amidst Economic Crosscurrents

December 1, 2025, has ushered in a period of apprehension for U.S. equity markets. Futures for the Dow Jones Industrial Average (NYSEARCA: DIA) are down approximately 0.4-0.5%, while S&P 500 (NYSEARCA: SPY) futures have declined by 0.5-0.8%. The technology-heavy Nasdaq Composite (NASDAQ: QQQ) is experiencing the most significant pressure, with futures indicating a drop of 0.7-1%. This downward trajectory follows a strong finish to November, where the S&P 500 and Dow both ended the month slightly higher, extending a seven-month streak of gains. In contrast, the Nasdaq Composite recorded its first monthly loss since March, falling 1.5% in November, primarily due to concerns over elevated valuations within the artificial intelligence (AI) sector.

A significant driver of current market sentiment is the anticipation surrounding upcoming manufacturing data. Investors are particularly focused on the release of Purchasing Managers' Index (PMI) figures for both the U.S. and global economies. These reports are critical barometers of economic activity, providing insights into factory output, new orders, and employment. A weaker-than-expected reading could signal a slowdown in global demand and manufacturing output, potentially reinforcing fears of an economic contraction and influencing the Federal Reserve's stance on interest rates. Conversely, stronger data could alleviate some concerns but might also temper expectations for aggressive rate cuts.

Adding another layer of complexity to the market landscape is the performance of the cryptocurrency market. Bitcoin's (NASDAQ: MSTR) recent tumble below $87,000, alongside sharp sell-offs in other major cryptocurrencies like Ethereum (NASDAQ: ETHE) and Solana (NASDAQ: SOL), has had a tangible impact on broader market sentiment. This decline is partly driven by the broader "risk-off" mood but also by specific factors within the crypto ecosystem, including regulatory uncertainties and profit-taking after a period of significant gains. Firms with substantial investments in or exposure to digital assets are feeling the direct effects, with their stock prices often mirroring the volatility of the crypto market. The interplay between traditional equities and the increasingly influential digital asset space is a growing consideration for investors and analysts alike.

Sectoral Shifts: Winners and Losers in a Volatile Environment

The current market dynamics, characterized by a "risk-off" sentiment and concerns over economic data, are likely to create distinct winners and losers across various sectors. Companies heavily reliant on robust economic growth and strong consumer spending, such as those in the industrial (NYSEARCA: XLI) and consumer discretionary (NYSEARCA: XLY) sectors, could face headwinds if manufacturing data indicates a slowdown. Industrials, in particular, are sensitive to production and order volumes, making them vulnerable to any negative surprises in the upcoming PMI reports. Similarly, luxury goods retailers and automotive manufacturers might see reduced demand if economic uncertainty leads consumers to tighten their belts.

Conversely, defensive sectors often perform better during periods of market uncertainty. Utilities (NYSEARCA: XLU), consumer staples (NYSEARCA: XLP), and healthcare (NYSEARCA: XLV) companies tend to be more resilient as demand for their products and services remains relatively stable regardless of economic fluctuations. These sectors could attract increased investor interest seeking stability amidst the current volatility. Furthermore, companies with strong balance sheets, consistent cash flows, and attractive dividend yields may also be favored as investors prioritize capital preservation over aggressive growth.

The technology sector, particularly companies with high valuations in the AI space, faces a mixed outlook. While the long-term potential of AI remains strong, the current "risk-off" environment, coupled with concerns over elevated valuations, could lead to further corrections in this segment. Companies like Nvidia (NASDAQ: NVDA) or Microsoft (NASDAQ: MSFT), which have seen significant runs, might experience profit-taking. However, established tech giants with diversified revenue streams and strong fundamentals could weather the storm more effectively. The cryptocurrency sell-off directly impacts companies with significant exposure to Bitcoin or other digital assets, such as MicroStrategy (NASDAQ: MSTR), which holds substantial Bitcoin reserves, or cryptocurrency exchanges like Coinbase (NASDAQ: COIN). These firms are likely to see their stock prices fluctuate in tandem with the crypto market's performance, presenting both risks and potential buying opportunities for long-term investors.

Broader Implications: Navigating a Complex Economic Landscape

The current market jitters at the start of December 2025 are not isolated events but rather fit into broader industry trends shaped by evolving monetary policy expectations and geopolitical considerations. The dominant factor remains the Federal Reserve's (FED) anticipated rate cut, with markets pricing in a high probability of a 25 basis point reduction at the December 10th FOMC meeting. This expectation has been a significant tailwind for equities in recent months. However, the hawkish comments from Bank of Japan (BOJ) Governor Kazuo Ueda, hinting at a potential rate hike on December 19th, introduce a counteracting force. Concerns about the unwinding of the yen carry trade could impact global liquidity and disproportionately affect risk assets, including tech and cryptocurrencies, creating a delicate balance for global financial markets.

The potential ripple effects extend beyond direct competitors and partners. A significant slowdown indicated by manufacturing data could trigger a re-evaluation of corporate earnings forecasts across various industries, leading to downward revisions and further market volatility. This could also impact supply chains, especially for companies heavily reliant on global manufacturing hubs. Regulatory and policy implications are also at play. The political landscape, with President Donald Trump's stated decision on the next Fed Chair and his potential second-term policies (such as looser regulations or tariffs), adds another layer of uncertainty that investors are closely monitoring. These policy shifts could have profound impacts on specific sectors and the broader economic outlook for 2025 and beyond.

Historically, market pullbacks at year-end or due to concerns over economic data are not uncommon. Comparisons can be drawn to periods where manufacturing indices signaled impending economic shifts, often leading to temporary market corrections. However, the unique combination of anticipated Fed rate cuts, hawkish signals from another major central bank, significant crypto market volatility, and a specific political context makes the current situation distinct. The market's ability to absorb these crosscurrents will be a key determinant of whether this early December dip is a temporary blip or the precursor to a more sustained period of correction.

What Comes Next: Navigating the Short-Term and Long-Term Outlook

The immediate future for the markets hinges significantly on the upcoming economic data releases and central bank pronouncements. The manufacturing PMIs for the U.S. and other major economies, alongside Fed Chair Powell's speech, U.S. labor data (JOLTS, ADP, jobless claims), and Friday's Personal Consumption Expenditure (PCE) inflation numbers, will be critical in shaping short-term market direction. A surprisingly strong PCE report, for instance, could dampen rate cut expectations, leading to further market downside, while weaker manufacturing data could reinforce recessionary fears. Investors will also be closely watching the Federal Open Market Committee (FOMC) meeting on December 10th for confirmation of the expected rate cut and any forward guidance on monetary policy.

In the long term, companies may need to strategically pivot or adapt to a potentially more volatile and uncertain economic environment. This could involve strengthening supply chain resilience, diversifying revenue streams, focusing on cost efficiencies, and investing in innovation that offers long-term growth regardless of short-term economic fluctuations. For example, companies in the technology sector might need to justify their high valuations with tangible profitability and sustainable growth rather than speculative potential. Market opportunities may emerge in defensive sectors or in companies that are undervalued due to the broader market sell-off but possess strong fundamentals. Conversely, challenges will persist for highly leveraged companies or those with business models sensitive to interest rate changes or economic downturns.

Potential scenarios range from a quick recovery, fueled by confirmed Fed rate cuts and resilient economic data, to a more prolonged period of market consolidation or correction if data disappoints and global central banks diverge significantly in their policy approaches. The "Santa Claus rally," a historical tendency for stocks to rise in December, remains a possibility, but analysts suggest it might be milder this year given the substantial rallies already observed. Investors should prepare for increased volatility and remain agile in their strategies, focusing on fundamental analysis and risk management in the coming months.

Comprehensive Wrap-Up: Key Takeaways and Future Watchpoints

The start of December 2025 has delivered a clear message of caution to financial markets. The primary takeaway is a palpable "risk-off" sentiment driven by a complex interplay of impending manufacturing data, central bank policy divergence, and a significant correction in the cryptocurrency market. While hopes for a Federal Reserve rate cut remain high, hawkish signals from the Bank of Japan and concerns over elevated valuations in certain sectors, particularly tech and AI, are contributing to the current unease. Bitcoin's struggle around the $86,000 mark further underscores the fragility in risk assets.

Moving forward, the market will be highly sensitive to incoming economic data, especially manufacturing and inflation reports, which will heavily influence the Federal Reserve's trajectory. Investors should also pay close attention to the communication from central banks globally, as coordinated or divergent policies could have significant ripple effects. The performance of the technology sector, particularly those firms with high growth expectations, will be a key indicator of broader market confidence. Furthermore, the resilience of companies with exposure to digital assets will be tested by continued volatility in the crypto space.

The lasting impact of these events will depend on whether the current downturn is a temporary adjustment or the beginning of a more sustained shift in market sentiment. While the prospect of a "Santa Claus rally" lingers, investors should exercise prudence and focus on building diversified portfolios that can withstand potential turbulence. Watching for clarity on monetary policy, signs of economic stabilization, and the earnings performance of key companies will be paramount in the coming months to navigate what promises to be a dynamic and challenging market environment.

This content is intended for informational purposes only and is not financial advice