With the Federal Reserve's benchmark rate now sitting at 3.64%, its lowest level since fall 2022, many income-focused investors have been moving out of traditional bonds and into dividend-paying stocks to find better yield.

That shift has already shown up in performance in early 2026. The Schwab U.S. Dividend Equity ETF (SCHD) is up more than 11.6% year-to-date (YTD), while the S&P 500 ($SPX) is in negative territory -5.38% over the same period. Also, energy stocks are out in front, offering an average yield of roughly 4.2% compared to about 1.3% for the broader market.

In this backdrop, Baker Hughes (BKR) is quietly reshaping its story beyond its past as a pure oilfield services name. On March 24, the company announced a collaboration with Google Cloud (GOOGL) to build AI-enabled power optimization and sustainability solutions for the fast-growing global data center industry. The unveiled deal at CERAWeek 2026 directly ties its technology to digital infrastructure.

This move comes after Baker Hughes already doubled its data center equipment order target to $3 billion between 2025 and 2027 in response to rising AI-driven power needs, and the Google Cloud partnership shows that push is picking up speed.

So with positioning itself at the intersection of industrial energy and AI infrastructure, is this the one dividend stock investors should be buying to ride the data center wave? Let’s find out.

Financial Strength That Supports the Story

Baker Hughes is an energy technology company that works across industrial equipment, power systems, and digital tools, which lines up neatly with what AI data centers need. Over the past 52 weeks, the stock has gained 41.66%, and it is already up 36.93% YTD, showing that investors are paying more attention to its growing role in power and data center infrastructure.

The shares are not cheap at current levels, trading at about 24.17 times forward earnings compared with a sector average of 15.26 times.

On the income side, Baker Hughes offers an annual dividend yield of about 1.47%, paying $0.23 per share every quarter, with a forward payout ratio of 35.20% and four straight years of dividend increases.

The latest numbers help support that payout. In the fourth quarter, the company booked $7.9 billion in orders, including $4.0 billion from IET, and reported record remaining performance obligations of $35.9 billion, with a record $32.4 billion from IET. Revenue came in at $7.4 billion, net income attributable to the company was $876 million, GAAP diluted EPS was $0.88, adjusted EPS was $0.78, and adjusted EBITDA rose 2% year-over-year (YOY) to $1.337 billion.

Cash flow was strong, with $1.662 billion from operations and $1.341 billion in free cash flow. For the full year, orders totaled $29.6 billion, including a record $14.9 billion from IET, while revenue held at $27.7 billion. Net income was $2.588 billion, GAAP and adjusted diluted EPS were both $2.60, adjusted EBITDA increased 5% to $4.825 billion, operating cash flow reached $3.81 billion, and free cash flow was $2.732 billion.

The Growth Engines Powering the Bull Case

Recently, Baker Hughes deepened its collaboration with Hydrostor, a long-duration energy storage developer, through a technology and equity deal. It will put Baker Hughes’ equipment into Hydrostor’s advanced compressed air energy storage design, with up to 1.4 GW of equipment orders tied to Hydrostor’s flagship projects. That agreement, announced at the 2026 Baker Hughes Annual Meeting in Florence, is aimed at building reliable and sustainable power systems for a grid that has to handle more data center demand.

On the data center side, Baker Hughes also secured an order from Twenty20 Energy for 10 Frame 5 gas turbines and related generator technology, supporting up to 250 MW of capacity. Initial deliveries are planned for 2027, and the units are earmarked for AI-focused data center projects in Georgia and Texas, as both companies work toward a wider deal for multi‑gigawatt power generation equipment for next‑generation AI and digital infrastructure.

In parallel, Baker Hughes won a 1.21 GW generator order from Boom Supersonic to supply 25 BRUSH Power Generation electric generators, AVRs, and cubicles for AI data centers. These generators will be paired with Boom’s 42 MW Superpower natural gas turbines for Crusoe, providing flexible, reliable base load power designed for high‑performance computing and AI workloads.

Wall Street’s Take and What Comes Next

For the March 2026 quarter, analysts expect Baker Hughes to earn $0.53 per share, up from $0.51 a year ago, which works out to 3.92% YOY growth. For the June 2026 quarter, the estimate is $0.63, the same as the prior-year period. Looking at the full year, Wall Street is modeling fiscal 2026 earnings of $2.63 per share versus $2.60 last year, a 1.15% increase.

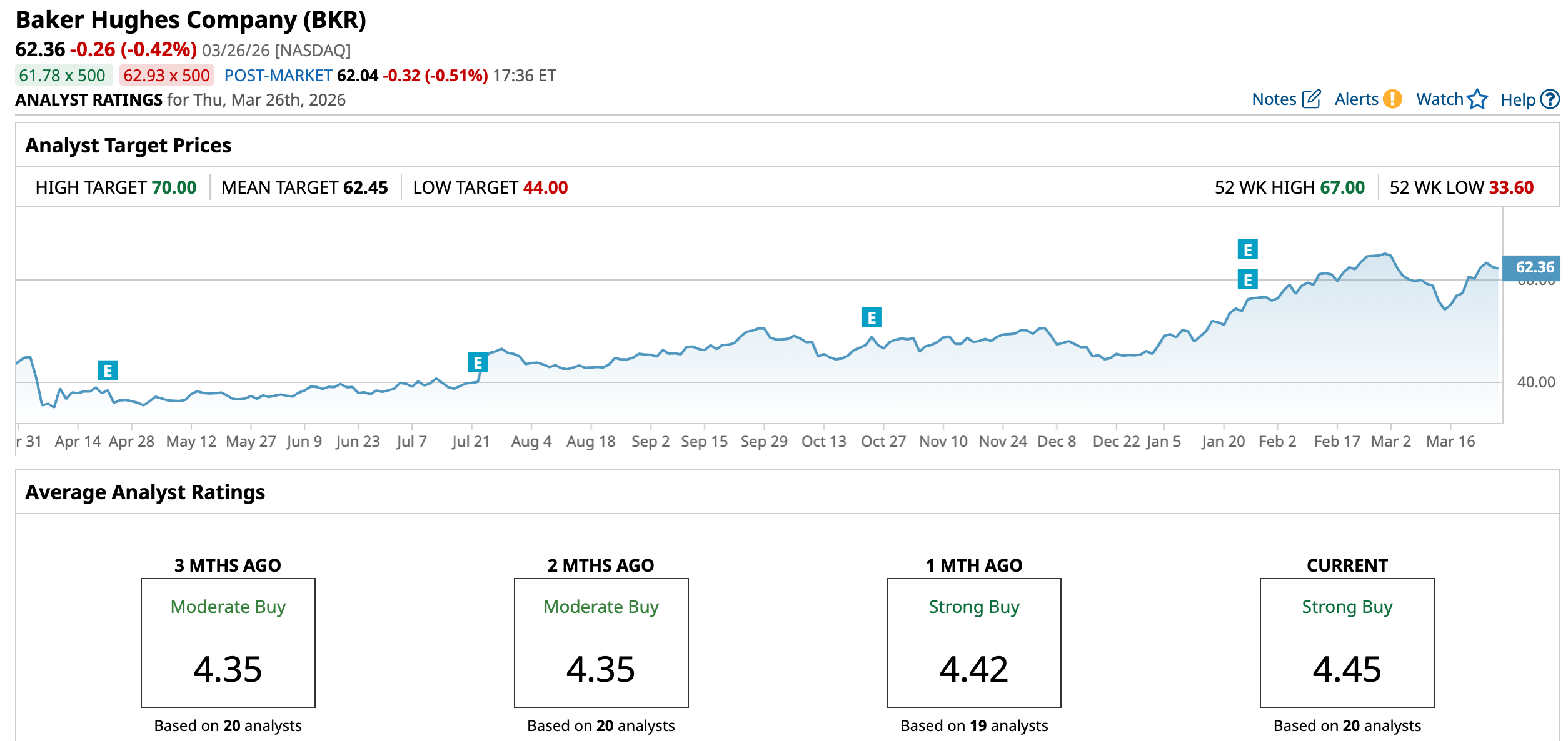

That outlook lines up with BofA Securities’ view earlier this year. On Feb. 2, the firm raised its price target to $65 and kept a “Buy” rating in place, citing Baker Hughes’ growing role in AI power infrastructure.

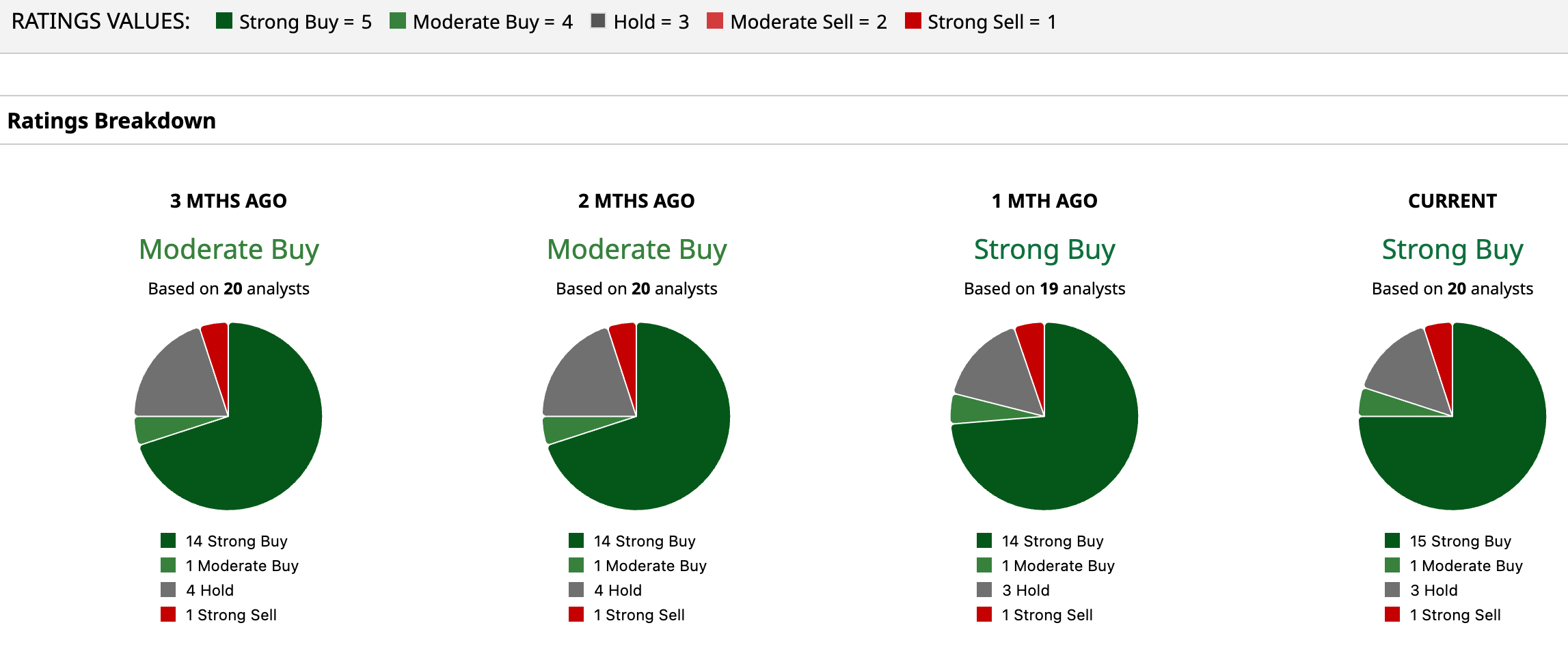

The broader analyst stance is similarly positive. Of 20 analysts surveyed, 15 rate the stock a “Strong Buy,” one rates it a “Moderate Buy,” three are listed as “Hold,” and the remaining one analyst is a “Strong Sell.” The mean price target is $62.45, while the shares are close to that level, suggesting targets may need to move higher if Baker Hughes continues to win data center-linked power deals and can show that this trend feeds into faster earnings growth.

Conclusion

Putting it all together, Baker Hughes looks like a credible way to get dividend exposure to the AI data center buildout rather than just another crowded chip trade. The yield is modest, but it is backed by solid free cash flow, a growing backlog, and a pipeline of power and storage projects that are explicitly tied to AI and data center demand. Earnings are expected to grind higher in 2026 and then accelerate into 2027, and Wall Street is already leaning strongly toward a “Strong Buy.” So if Baker Hughes keeps executing on data center-linked orders, and the Google Cloud partnership gains traction, shares are more likely to trend higher over the next couple of years.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart