Looking back on non-discretionary retail stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including Grocery Outlet (NASDAQ: GO) and its peers.

Food is non-discretionary because it's essential for life (maybe not those Oreos?), so consumers naturally need a place to buy it. Selling food is a notoriously tough business, however, as the costs of procuring and transporting oftentimes perishable products and operating stores fit to sell those products can be high. Competition is also fierce because the alternatives are numerous. While online competition threatens all of retail, grocery is one of the least penetrated because of the nature of the product. Still, we could be one startup or innovation away from a paradigm shift.

The 9 non-discretionary retail stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.5% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 5% on average since the latest earnings results.

Grocery Outlet (NASDAQ: GO)

Due to its differentiated procurement and buying approach, Grocery Outlet (NASDAQ: GO) is a discount grocery store chain that offers substantial discounts on name-brand products.

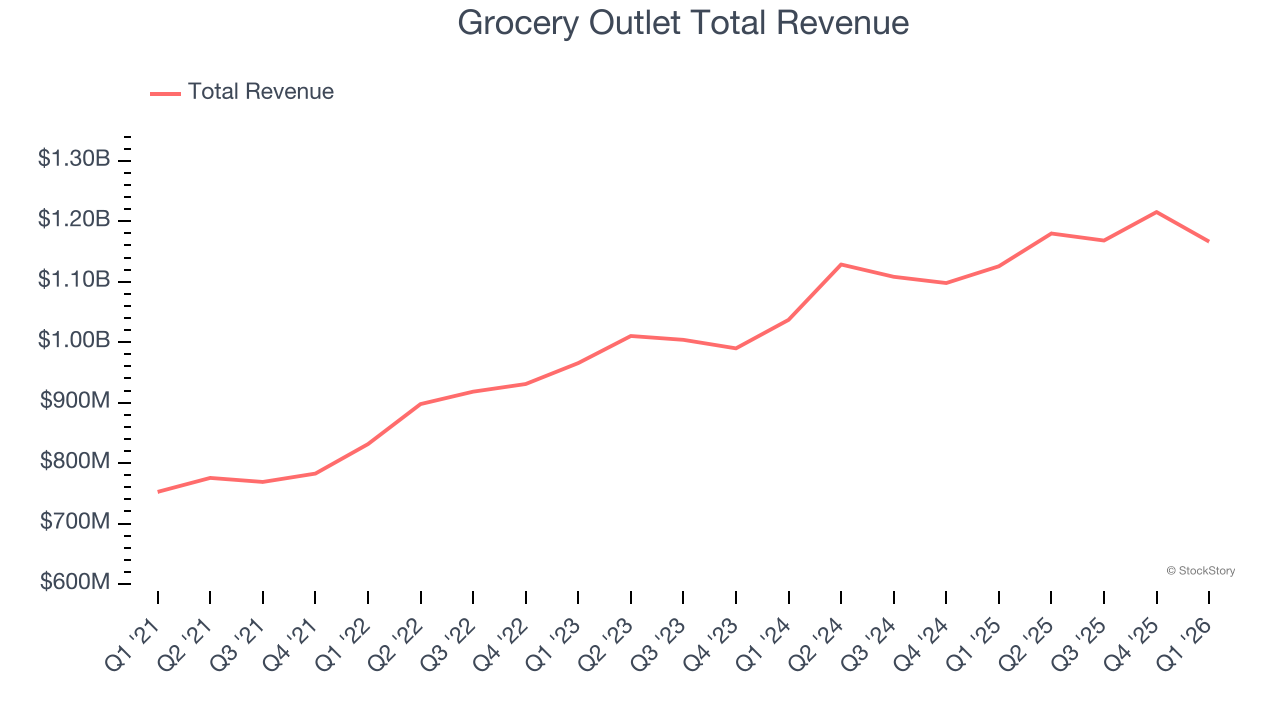

Grocery Outlet reported revenues of $1.17 billion, up 3.6% year on year. This print exceeded analysts’ expectations by 1.4%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS and EBITDA estimates.

Grocery Outlet scored the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 26.6% since reporting and currently trades at $9.80.

Is now the time to buy Grocery Outlet? Access our full analysis of the earnings results here, it’s free.

Best Q1: Target (NYSE: TGT)

With a higher focus on style and aesthetics compared to other large general merchandise retailers, Target (NYSE: TGT) serves the suburban consumer who is looking for a wide range of products under one roof.

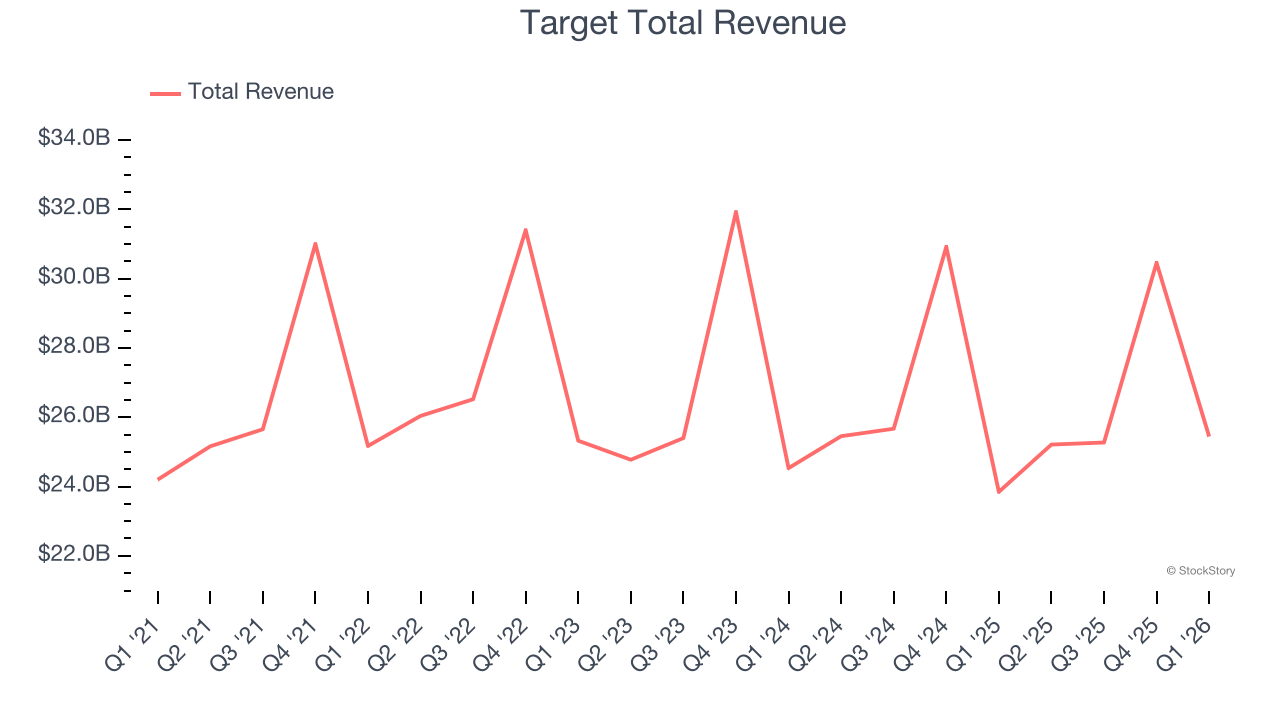

Target reported revenues of $25.44 billion, up 6.7% year on year, outperforming analysts’ expectations by 3.4%. The business had an exceptional quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems happy with the results as the stock is up 5.1% since reporting. It currently trades at $133.75.

Is now the time to buy Target? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Walmart (NASDAQ: WMT)

Known for its large-format Supercenters, Walmart (NASDAQ: WMT) is a retail pioneer that serves a budget-conscious consumer who is looking for a wide range of products under one roof.

Walmart reported revenues of $177.8 billion, up 7.3% year on year, exceeding analysts’ expectations by 1.6%. Still, it was a slower quarter as it posted full-year EPS guidance missing analysts’ expectations and EPS guidance for next quarter missing analysts’ expectations.

Walmart delivered the weakest guidance update in the group. As expected, the stock is down 12.4% since the results and currently trades at $114.66.

Read our full analysis of Walmart’s results here.

Dollar Tree (NASDAQ: DLTR)

A treasure hunt because there’s no guarantee of consistent product selection, Dollar Tree (NASDAQ: DLTR) is a discount retailer that sells general merchandise and select packaged food at extremely low prices.

Dollar Tree reported revenues of $4.98 billion, up 7.2% year on year. This number was in line with analysts’ expectations. Overall, it was a very strong quarter as it also produced EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

Dollar Tree delivered the highest guidance raise but had the weakest full-year guidance update among its peers. The stock is up 27.6% since reporting and currently trades at $122.38.

Read our full, actionable report on Dollar Tree here, it’s free.

Kroger (NYSE: KR)

With a sprawling network of over 2,400 locations offering digital pickup services, Kroger (NYSE: KR) operates supermarkets, pharmacies, and fuel centers across 35 states, offering customers groceries, household items, and private-label products.

Kroger reported revenues of $46.12 billion, up 2.2% year on year. This result beat analysts’ expectations by 1.4%. Taking a step back, it was a mixed quarter as it also logged full-year EPS guidance slightly topping analysts’ expectations but a miss of analysts’ gross margin estimates.

Kroger had the slowest revenue growth among its peers. The stock is down 12.8% since reporting and currently trades at $55.89.

Read our full, actionable report on Kroger here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.