Sonos’s stock price has taken a beating over the past six months, shedding 24% of its value and falling to $13.75 per share. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Sonos, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Sonos Will Underperform?

Even though the stock has become cheaper, we’re cautious about Sonos. Here are three reasons we avoid SONO, plus one stock we’d rather own.

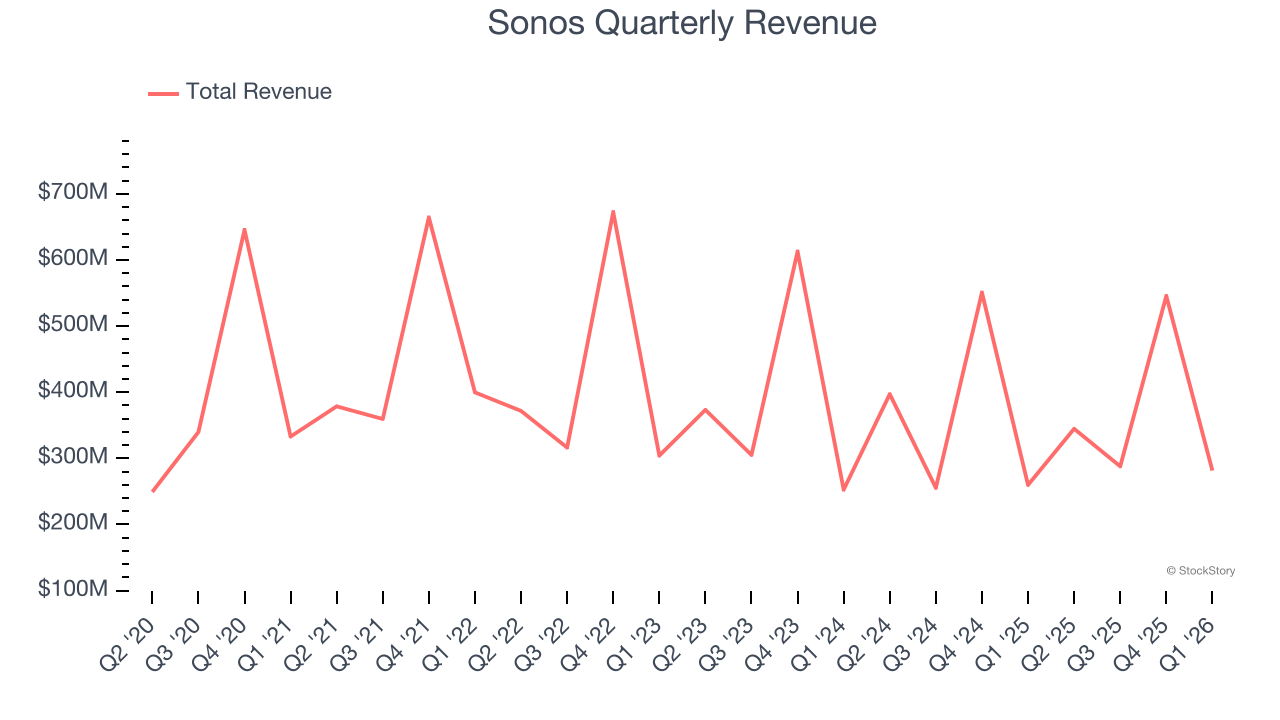

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Sonos’s demand was weak and its revenue declined by 1.4% per year. This was below our standards and is a sign of poor business quality.

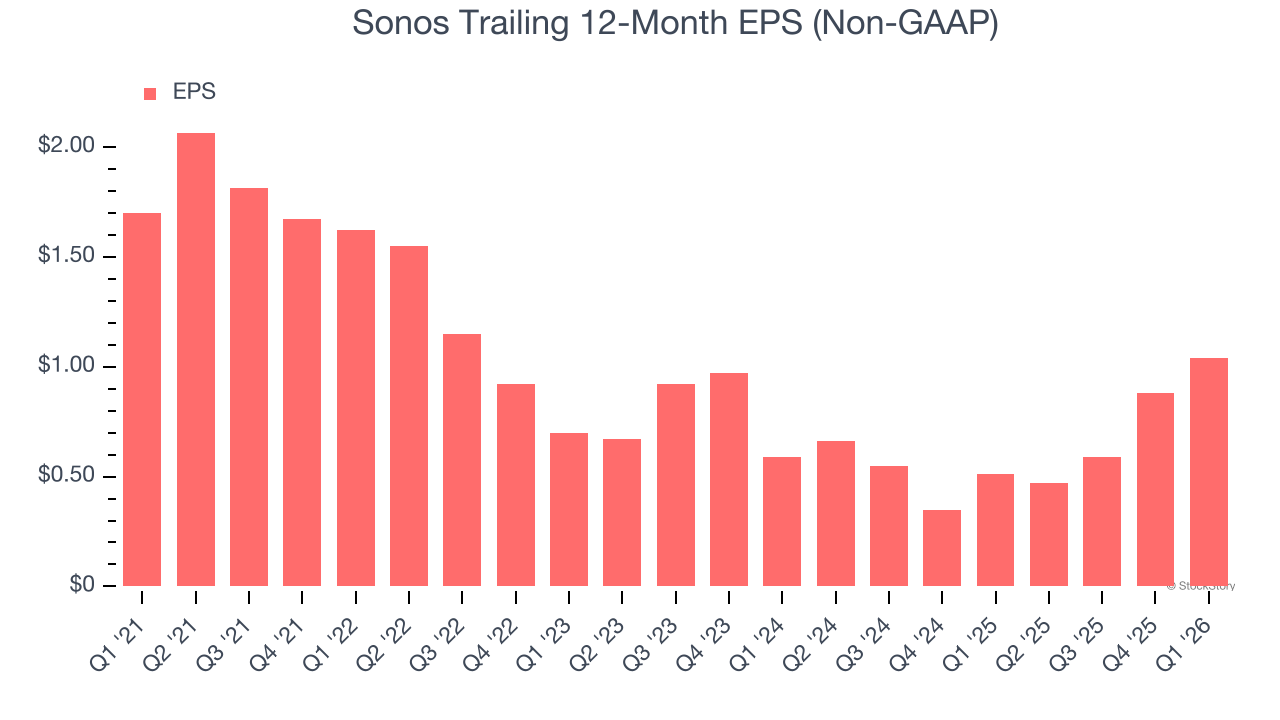

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Sonos, its EPS declined by 9.3% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

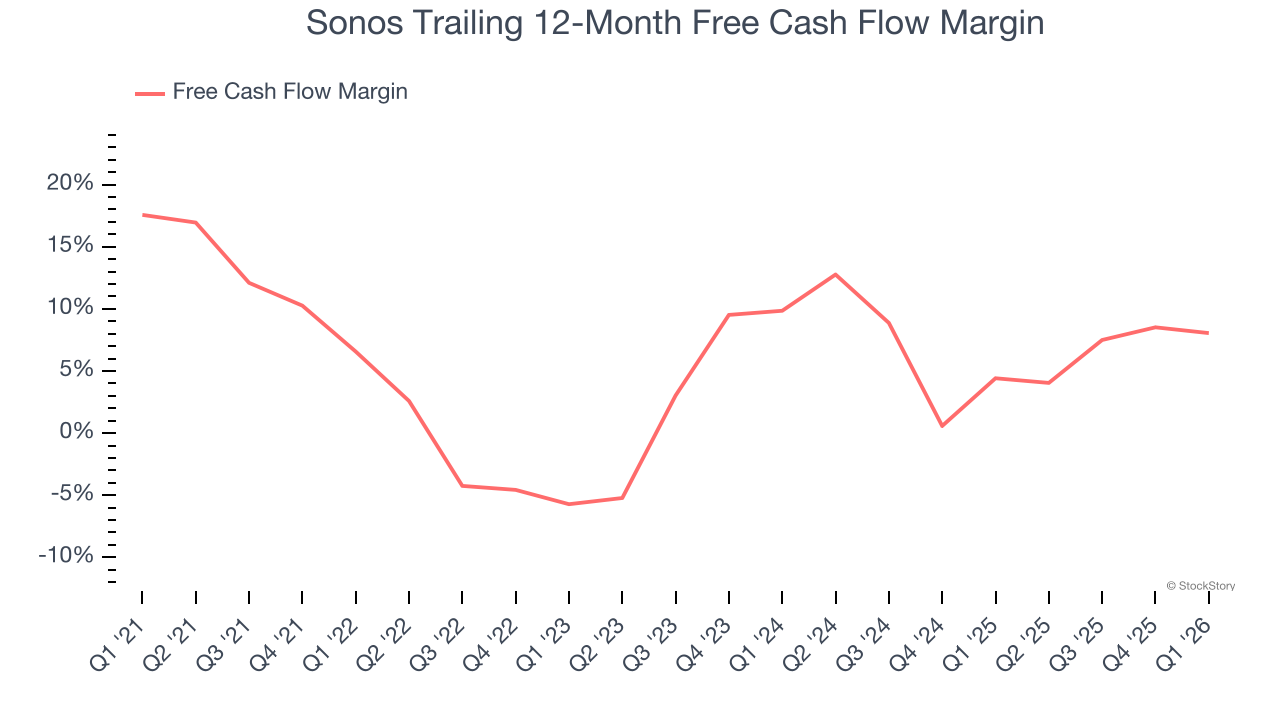

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Sonos has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6.2%, below what we’d expect for a consumer discretionary business.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Sonos, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 13.3× forward P/E (or $13.75 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are better investments elsewhere. We’d recommend looking at the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Sonos

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.