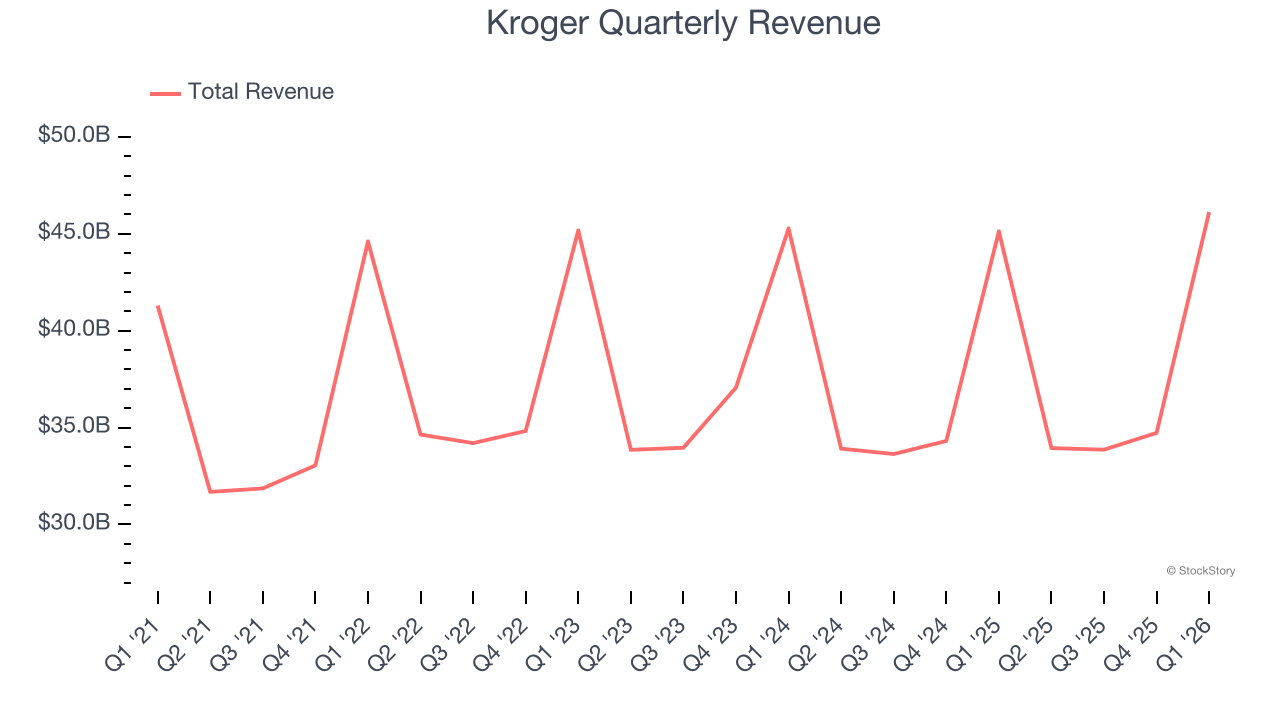

Grocery retail giant Kroger (NYSE: KR) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 2.2% year on year to $46.12 billion. Its GAAP profit of $1.46 per share was 8.6% below analysts’ consensus estimates.

Is now the time to buy Kroger? Find out by accessing our full research report, it’s free.

Kroger (KR) Q1 CY2026 Highlights:

- Revenue: $46.12 billion vs analyst estimates of $45.46 billion (2.2% year-on-year growth, 1.4% beat)

- EPS (GAAP): $1.46 vs analyst expectations of $1.60 (8.6% miss)

- EPS (GAAP) guidance for the full year is $5.20 at the midpoint, beating analyst estimates by 1.2%

- Operating Margin: 3.1%, in line with the same quarter last year

- Free Cash Flow Margin: 1%, down from 2.4% in the same quarter last year

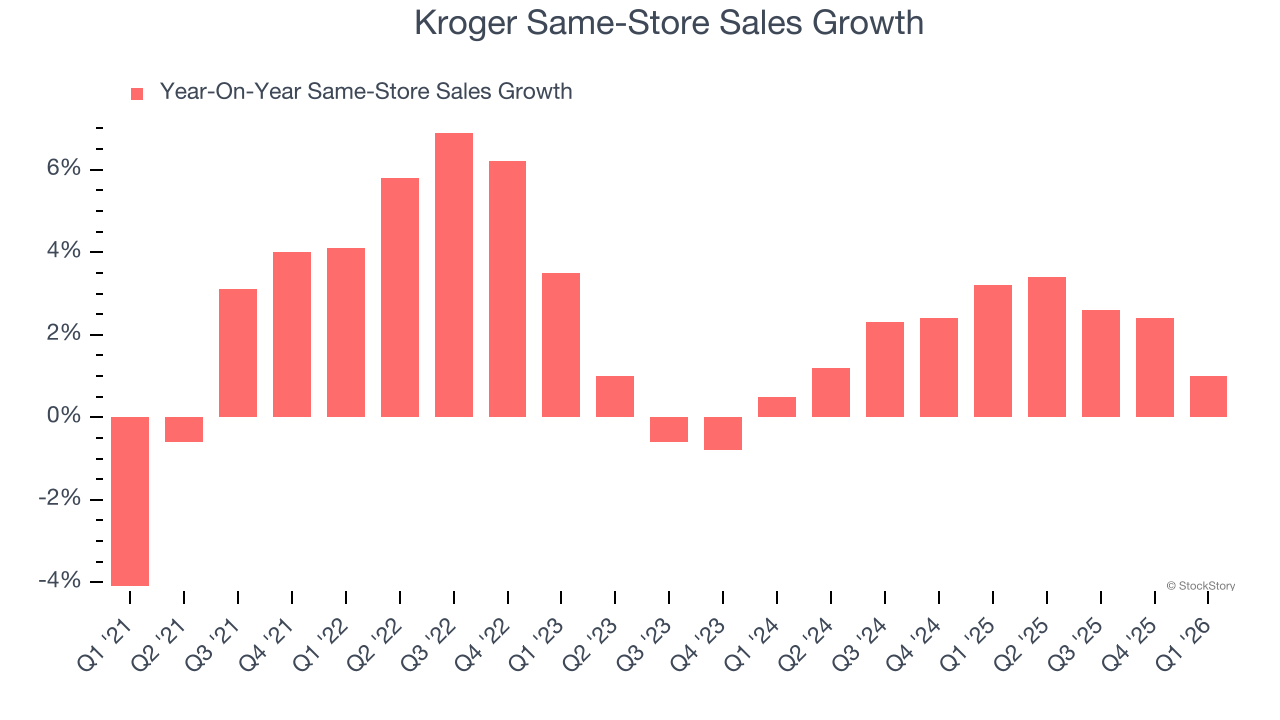

- Same-Store Sales rose 1% year on year (3.2% in the same quarter last year)

- Market Capitalization: $39.28 billion

Company Overview

With a sprawling network of over 2,400 locations offering digital pickup services, Kroger (NYSE: KR) operates supermarkets, pharmacies, and fuel centers across 35 states, offering customers groceries, household items, and private-label products.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $148.6 billion in revenue over the past 12 months, Kroger is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To expand meaningfully, Kroger likely needs to tweak its prices or enter new markets.

As you can see below, Kroger struggled to increase demand as its $148.6 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it didn’t open many new stores.

This quarter, Kroger reported modest year-on-year revenue growth of 2.2% but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 1.6% over the next 12 months. Although this projection indicates its newer products will fuel better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

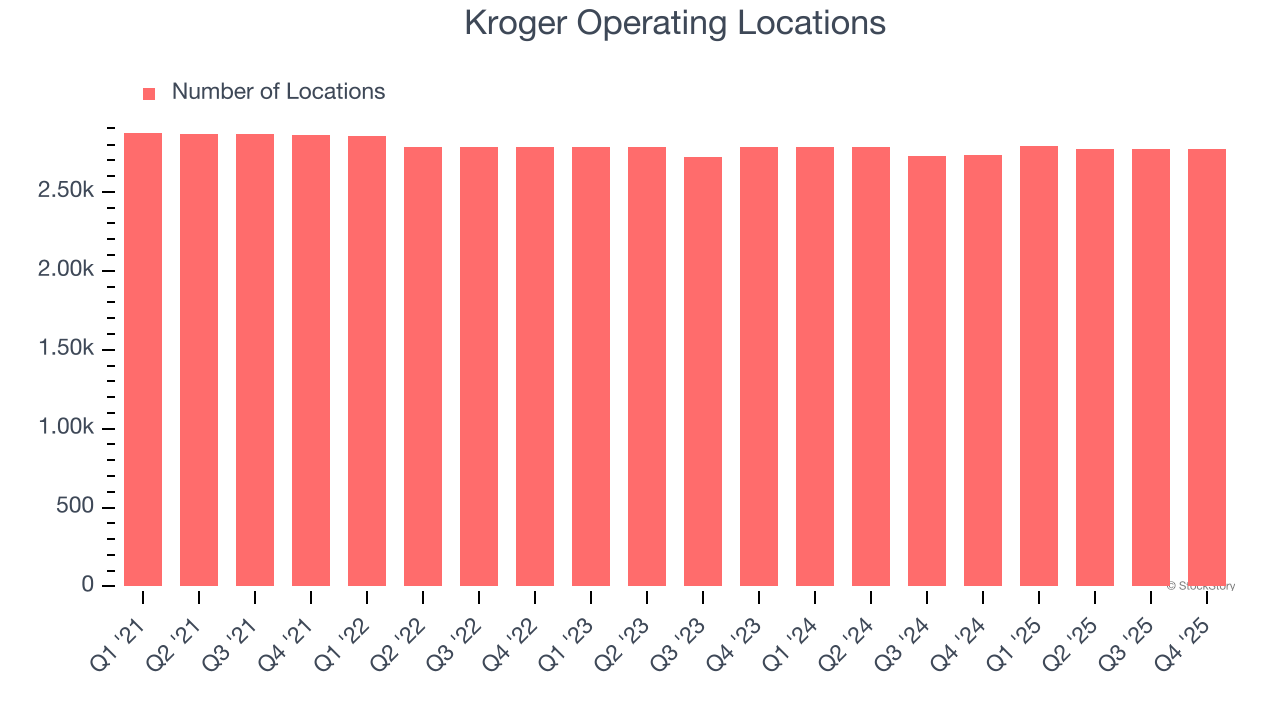

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Kroger has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Kroger reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company’s store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Kroger’s demand rose over the last two years and slightly outpaced the industry. On average, the company’s same-store sales have grown by 2.3% per year. Given its flat store base over the same period, this performance stems from not only increased foot traffic at existing locations but also higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, Kroger’s same-store sales rose 1% year on year. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Kroger can reaccelerate growth.

Key Takeaways from Kroger’s Q1 Results

It was good to see Kroger narrowly top analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance slightly exceeded Wall Street’s estimates. On the other hand, its gross margin and EPS both fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.1% to $59.90 immediately following the results.

The latest quarter from Kroger’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).