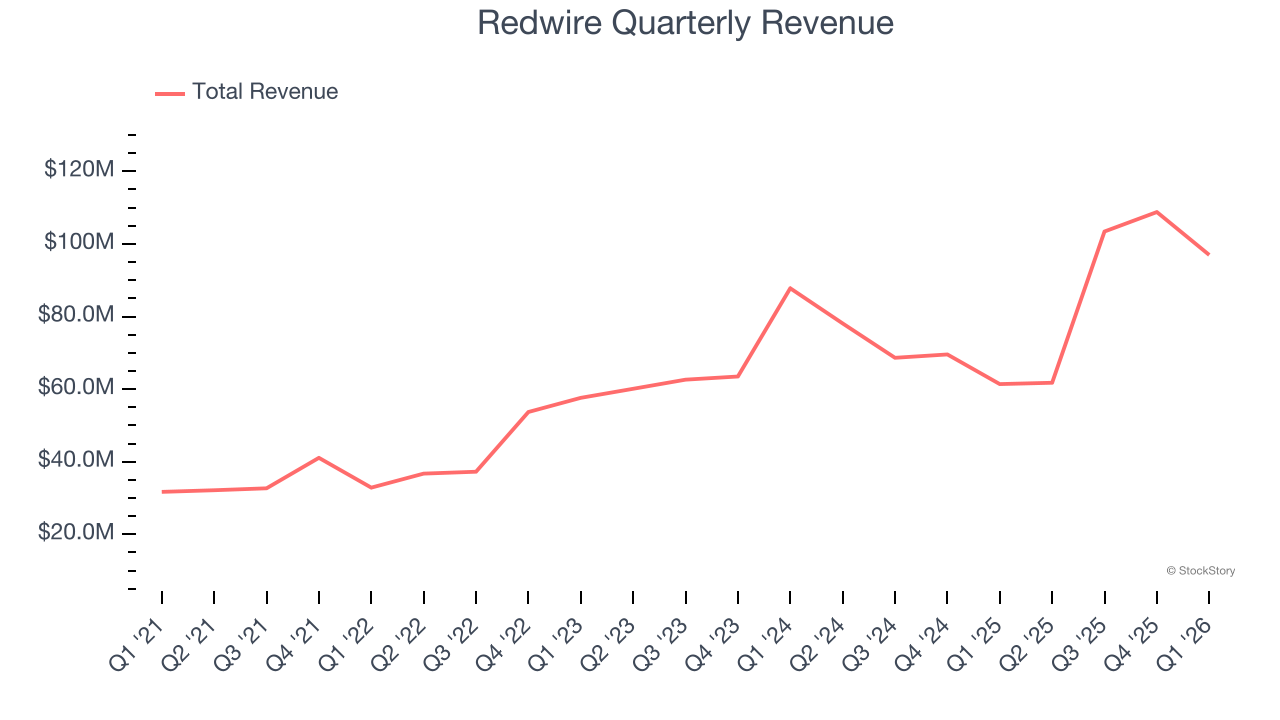

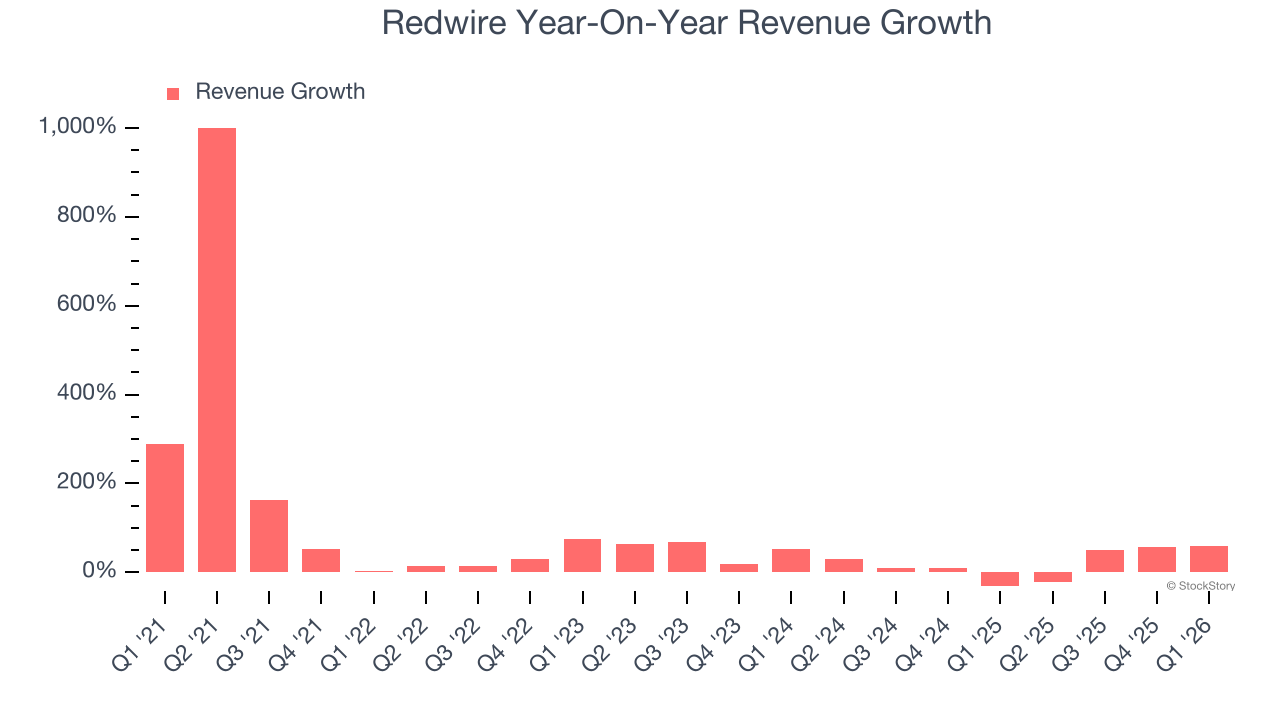

Aerospace and defense company Redwire (NYSE: RDW) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 57.9% year on year to $96.97 million. On the other hand, the company’s full-year revenue guidance of $475 million at the midpoint came in 0.8% above analysts’ estimates. Its GAAP loss of $0.40 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Redwire? Find out by accessing our full research report, it’s free.

Redwire (RDW) Q1 CY2026 Highlights:

- Revenue: $96.97 million vs analyst estimates of $104.6 million (57.9% year-on-year growth, 7.3% miss)

- EPS (GAAP): -$0.40 vs analyst estimates of -$0.15 (significant miss)

- Adjusted EBITDA: -$9.2 million (-9.5% margin, 306% year-on-year decline)

- The company reconfirmed its revenue guidance for the full year of $475 million at the midpoint

- Adjusted EBITDA Margin: -9.5%, down from -3.7% in the same quarter last year

- Free Cash Flow was -$11.42 million compared to -$46.87 million in the same quarter last year

- Backlog: $498.1 million at quarter end, up 71% year on year

- Market Capitalization: $1.91 billion

Company Overview

Based in Jacksonville, Florida, Redwire (NYSE: RDW) is a provider of systems and components used in space infrastructure.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Redwire’s 40.4% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Redwire’s annualized revenue growth of 16.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Redwire achieved a magnificent 57.9% year-on-year revenue growth rate, but its $96.97 million of revenue fell short of Wall Street’s lofty estimates.

Looking ahead, sell-side analysts expect revenue to grow 33.3% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will catalyze better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

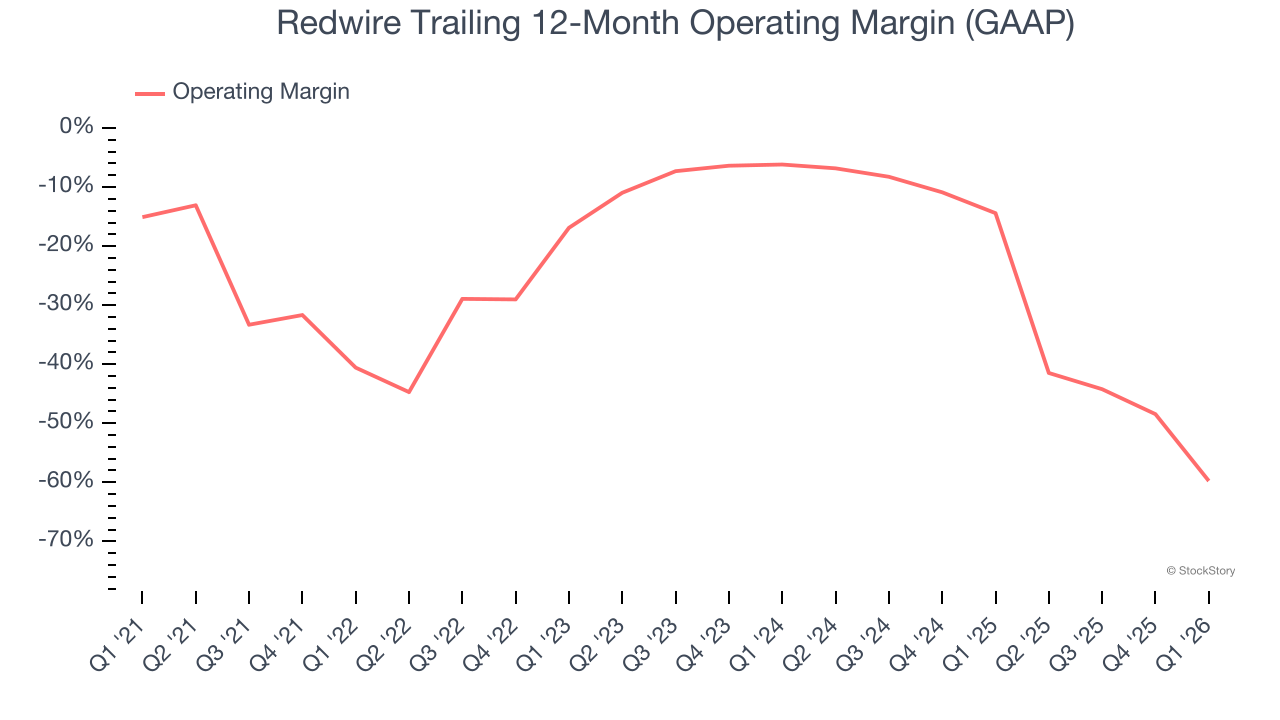

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Redwire’s high expenses have contributed to an average operating margin of negative 29.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Redwire’s operating margin decreased by 19.2 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Redwire’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Redwire’s operating margin was negative 71.9% this quarter.

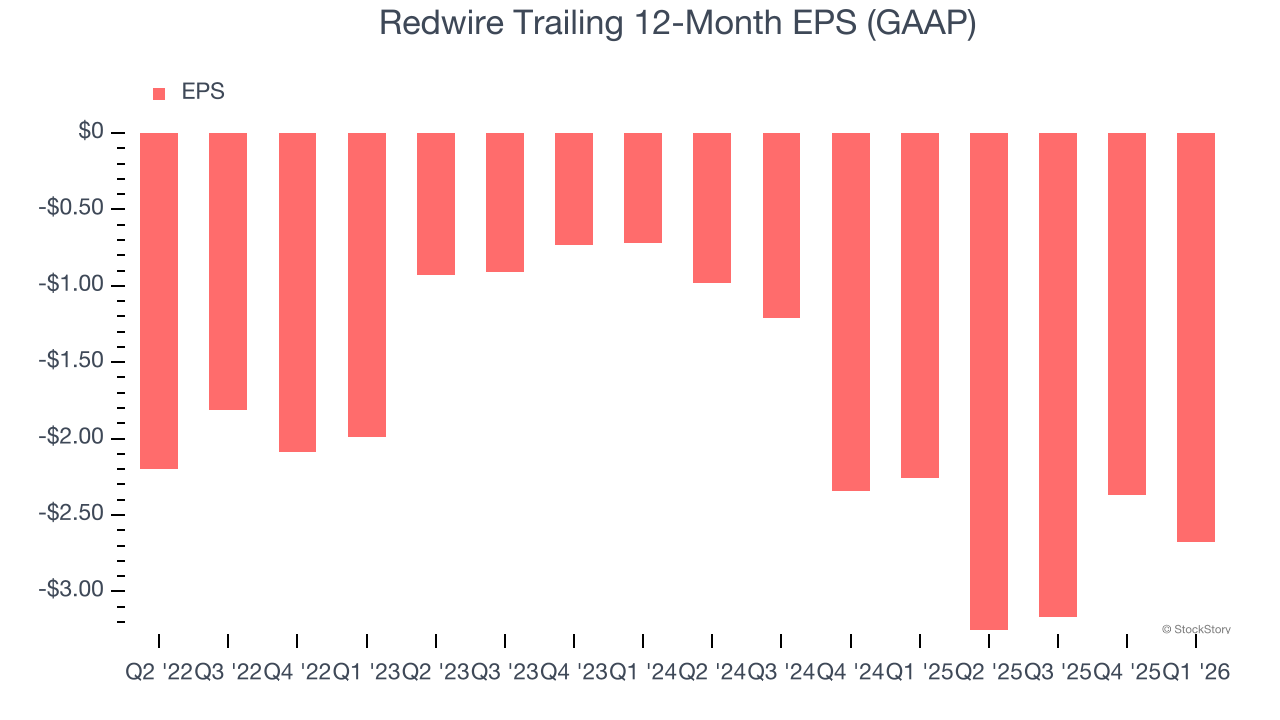

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Redwire’s earnings losses deepened over the last four years as its EPS dropped 6.7% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Redwire’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Redwire, its two-year annual EPS declines of 92.9% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, Redwire reported EPS of negative $0.40, down from negative $0.09 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Redwire’s Q1 Results

We were impressed by how significantly Redwire blew past analysts’ adjusted operating income expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 10.5% to $8.67 immediately following the results.

Redwire’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).