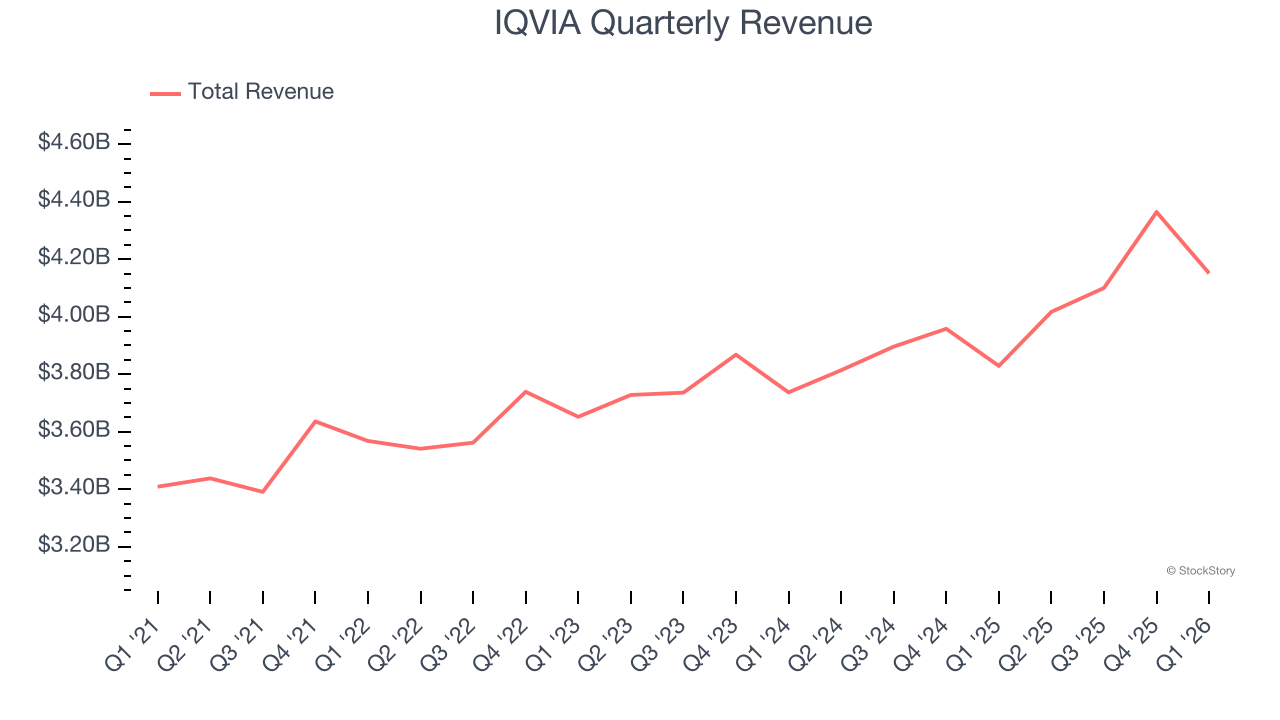

Clinical research company IQVIA (NYSE: IQV) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 8.4% year on year to $4.15 billion. The company expects the full year’s revenue to be around $17.25 billion, close to analysts’ estimates. Its non-GAAP profit of $2.90 per share was 2.9% above analysts’ consensus estimates.

Is now the time to buy IQVIA? Find out by accessing our full research report, it’s free.

IQVIA (IQV) Q1 CY2026 Highlights:

- Revenue: $4.15 billion vs analyst estimates of $4.1 billion (8.4% year-on-year growth, 1.1% beat)

- Adjusted EPS: $2.90 vs analyst estimates of $2.82 (2.9% beat)

- Adjusted EBITDA: $932 million vs analyst estimates of $926.4 million (22.5% margin, 0.6% beat)

- The company reconfirmed its revenue guidance for the full year of $17.25 billion at the midpoint

- Management slightly raised its full-year Adjusted EPS guidance to $12.80 at the midpoint

- EBITDA guidance for the full year is $4 billion at the midpoint, in line with analyst expectations

- Operating Margin: 12.4%, in line with the same quarter last year

- Free Cash Flow Margin: 11.8%, similar to the same quarter last year

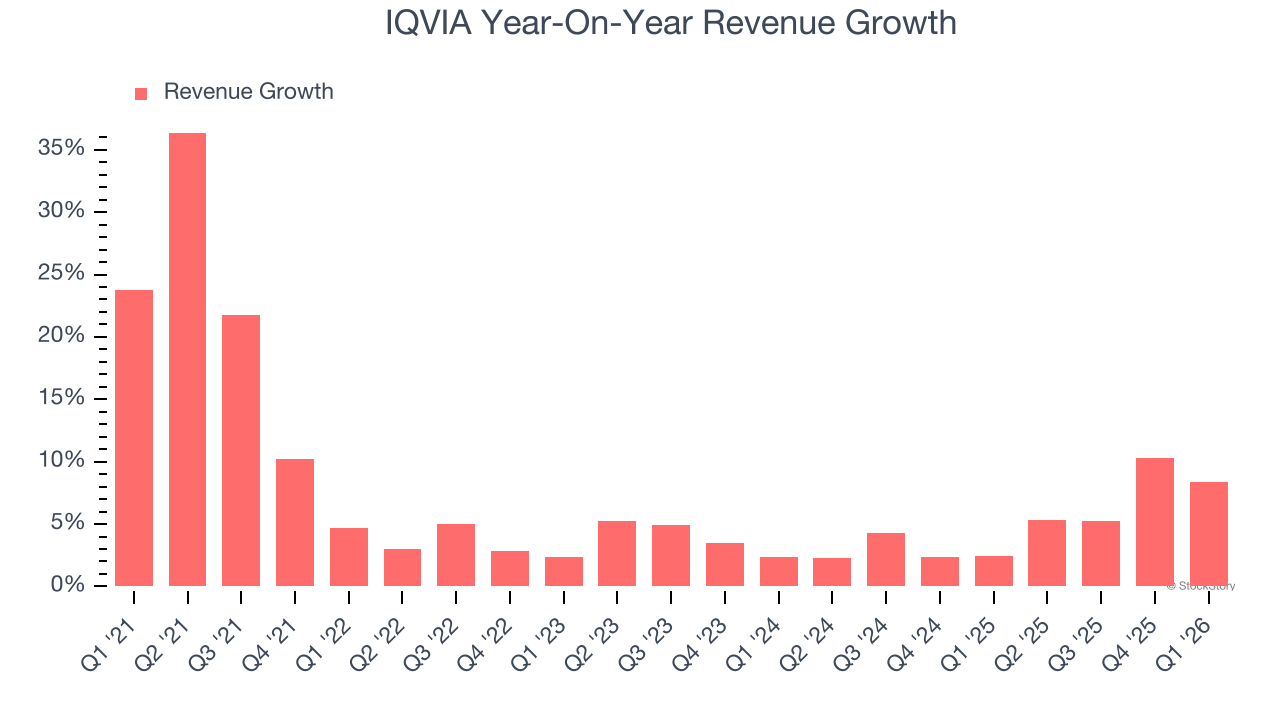

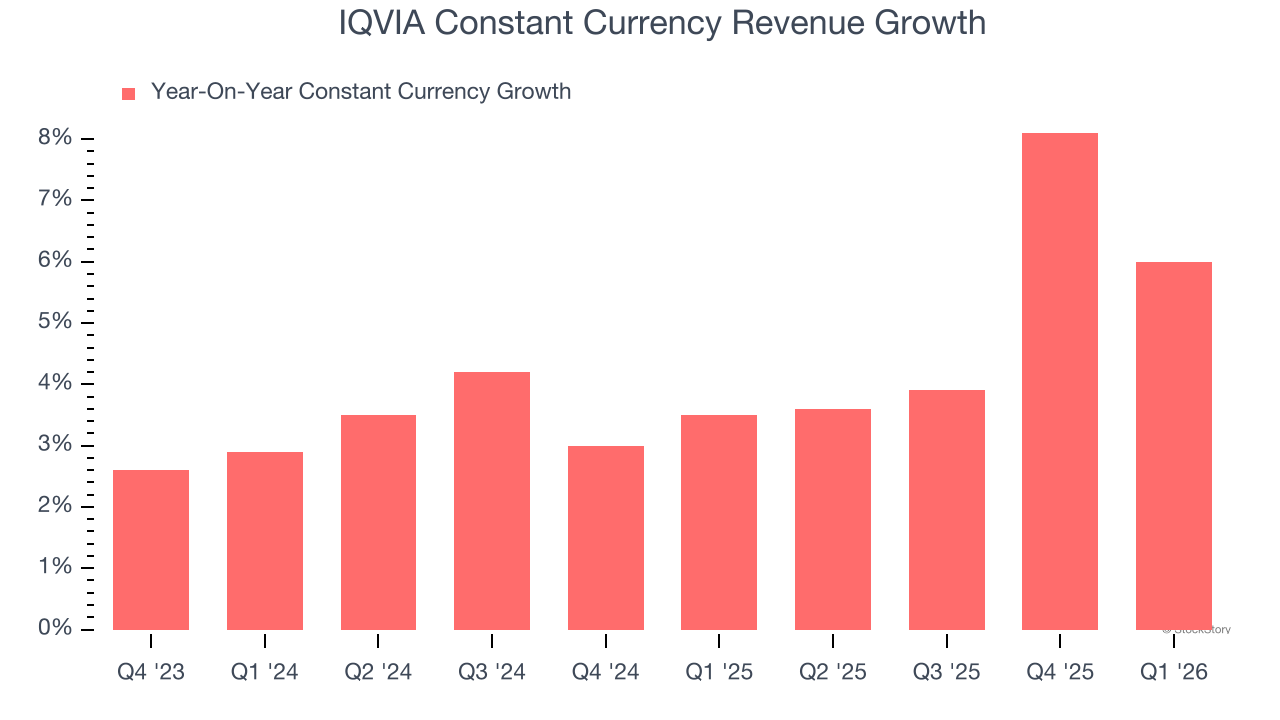

- Constant Currency Revenue rose 6% year on year (3.5% in the same quarter last year)

- Market Capitalization: $27.02 billion

"IQVIA delivered an outstanding start to the year, with organic revenue growth accelerating more than anticipated, Adjusted Diluted EPS exceeding the high-end of our expectations and Free Cash Flow at 100% of Adjusted Net Income,” said Ari Bousbib, chairman and CEO of IQVIA.

Company Overview

Created from the 2016 merger of Quintiles (a clinical research organization) and IMS Health (a healthcare data specialist), IQVIA (NYSE: IQV) provides clinical research services, data analytics, and technology solutions to help pharmaceutical companies develop and market medications more effectively.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, IQVIA’s sales grew at a mediocre 6.7% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. IQVIA’s recent performance shows its demand has slowed as its annualized revenue growth of 5.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 4.5% year-on-year growth. Because this number aligns with its reported revenue growth, we can see that foreign exchange has not had a meaningful impact on topline.

This quarter, IQVIA reported year-on-year revenue growth of 8.4%, and its $4.15 billion of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 5.1% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and indicates its newer products and services will help support its recent top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

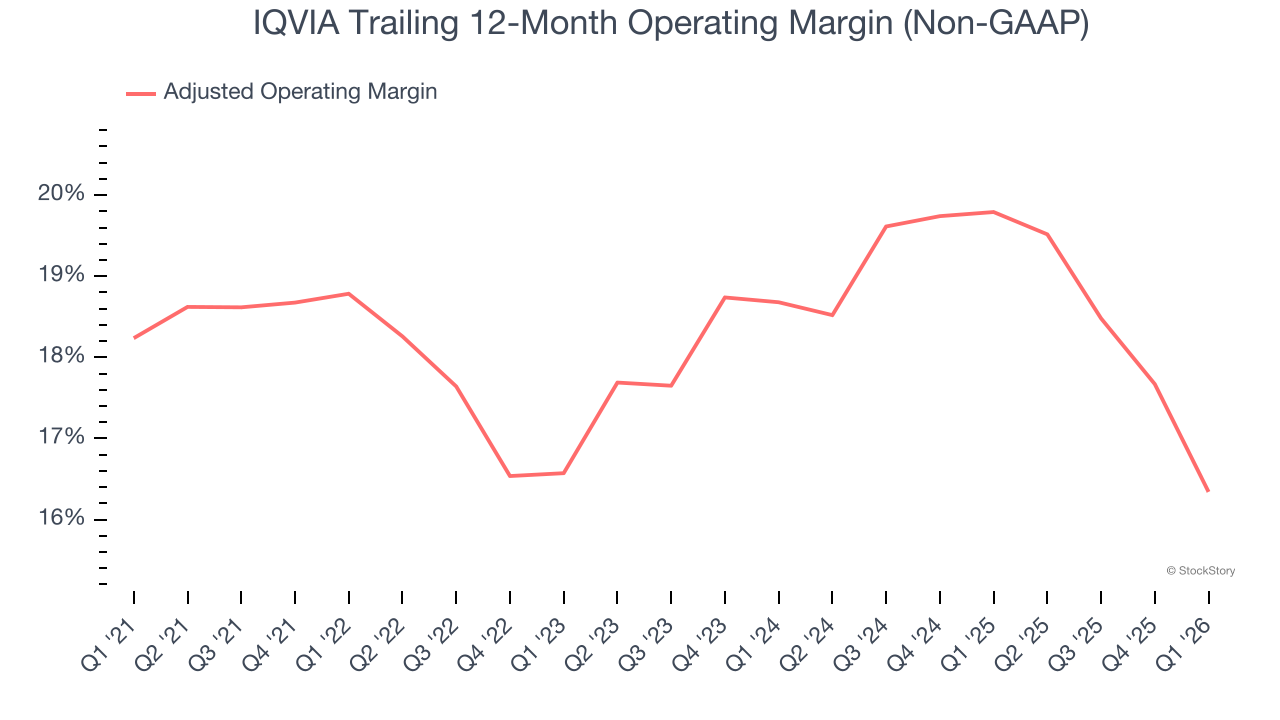

IQVIA has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average adjusted operating margin of 18%.

Looking at the trend in its profitability, IQVIA’s adjusted operating margin decreased by 2.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 2.3 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, IQVIA generated an adjusted operating margin profit margin of 13.9%, down 5.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

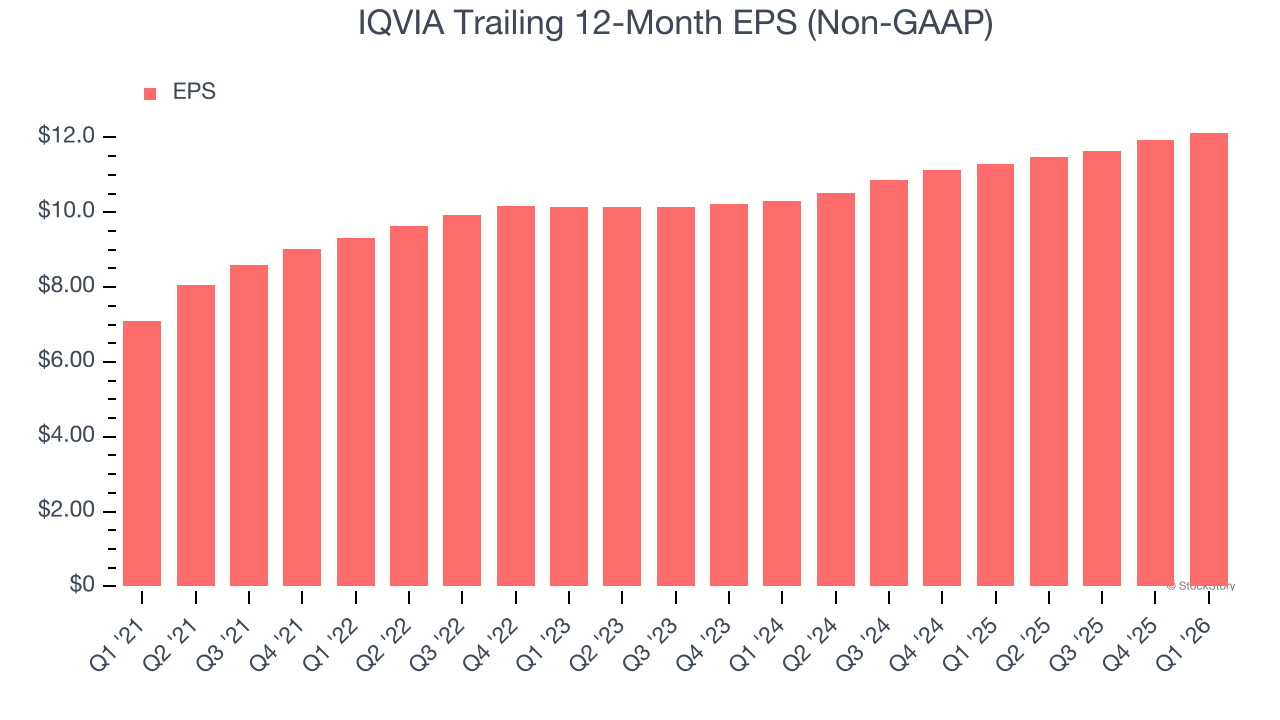

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

IQVIA’s EPS grew at 11.3% compounded annual growth rate over the last five years, higher than its 6.7% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its adjusted operating margin didn’t improve.

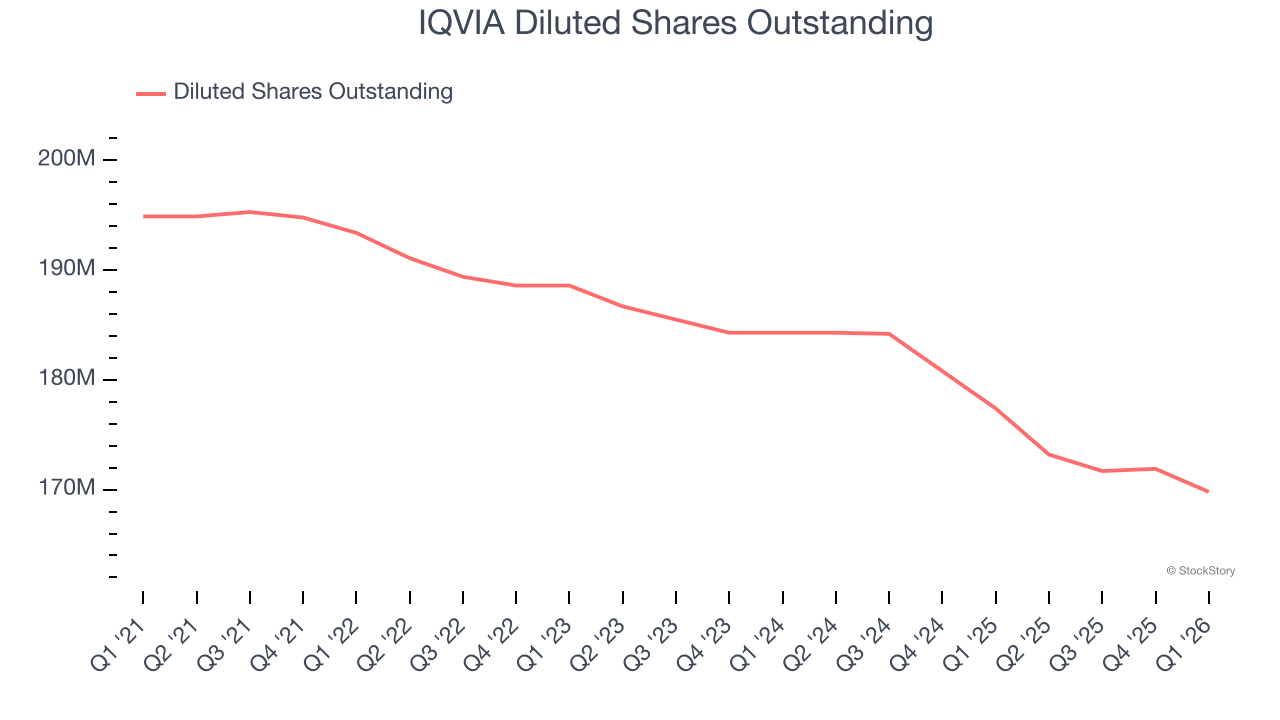

Diving into IQVIA’s quality of earnings can give us a better understanding of its performance. A five-year view shows that IQVIA has repurchased its stock, shrinking its share count by 12.9%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, IQVIA reported adjusted EPS of $2.90, up from $2.70 in the same quarter last year. This print beat analysts’ estimates by 2.9%. Over the next 12 months, Wall Street expects IQVIA’s full-year EPS of $12.13 to grow 7.4%.

Key Takeaways from IQVIA’s Q1 Results

It was good to see IQVIA narrowly top analysts’ revenue expectations this quarter. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 4.9% to $152.98 immediately after reporting.

So should you invest in IQVIA right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).