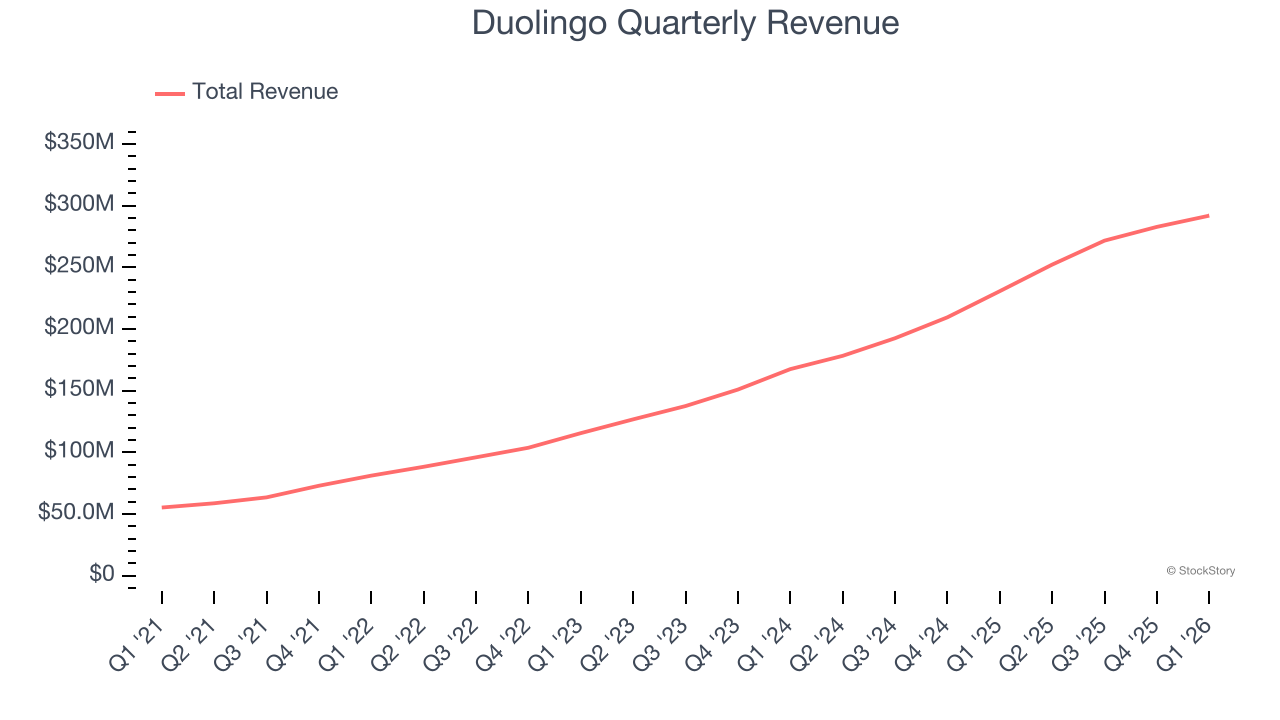

Language-learning app Duolingo (NASDAQ: DUOL) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 26.5% year on year to $292 million. Guidance for next quarter’s revenue was better than expected at $295.5 million at the midpoint, 0.7% above analysts’ estimates. Its GAAP profit of $0.89 per share was 18.4% above analysts’ consensus estimates.

Is now the time to buy Duolingo? Find out by accessing our full research report, it’s free.

Duolingo (DUOL) Q1 CY2026 Highlights:

- Revenue: $292 million vs analyst estimates of $288.6 million (26.5% year-on-year growth, 1.2% beat)

- EPS (GAAP): $0.89 vs analyst estimates of $0.75 (18.4% beat)

- Adjusted EBITDA: $83.4 million vs analyst estimates of $73.64 million (28.6% margin, 13.3% beat)

- Q2 and full-year bookings guidance both missed

- The company reconfirmed its revenue guidance for the full year of $1.21 billion at the midpoint

- EBITDA guidance for the full year is $310 million at the midpoint, above analyst estimates of $301.7 million

- Operating Margin: 15.3%, up from 10.2% in the same quarter last year

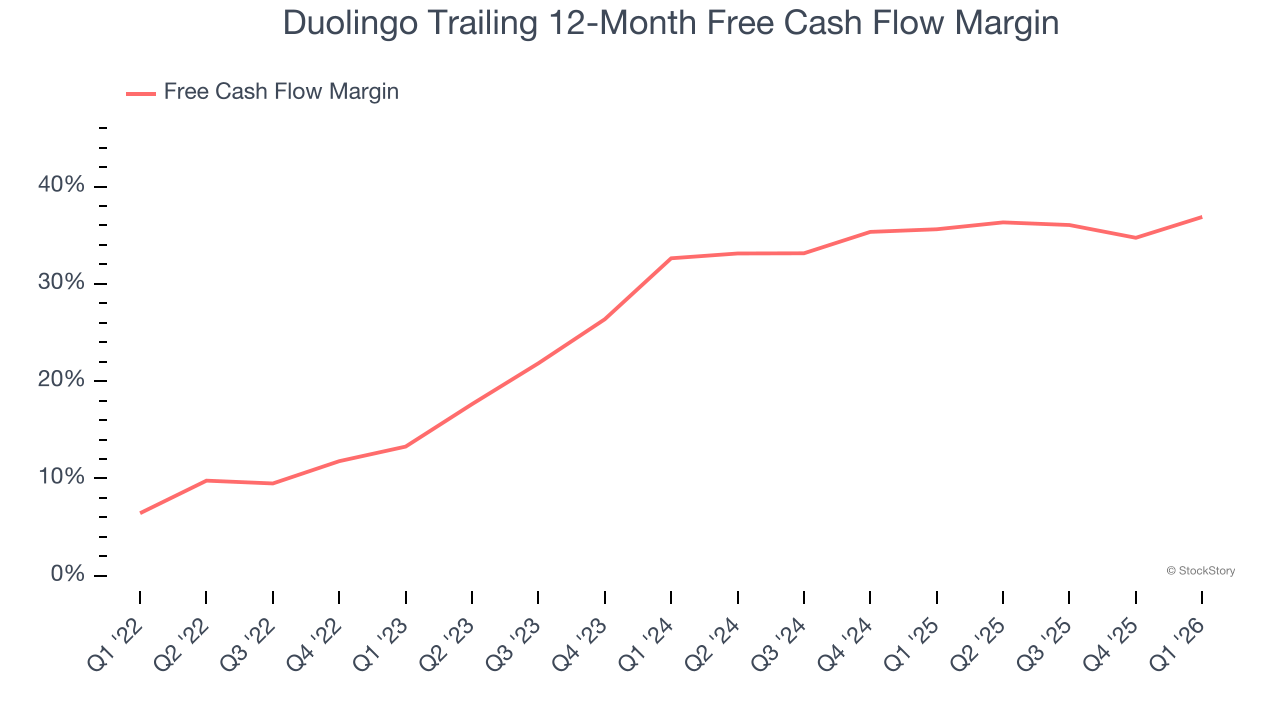

- Free Cash Flow Margin: 50.6%, up from 33.1% in the previous quarter

- Market Capitalization: $5.20 billion

Company Overview

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ: DUOL) is a mobile app helping people learn new languages.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Duolingo grew its sales at an incredible 39.6% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Duolingo reported robust year-on-year revenue growth of 26.5%, and its $292 million of revenue topped Wall Street estimates by 1.2%. Company management is currently guiding for a 17.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.1% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is noteworthy and indicates the market is forecasting success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Duolingo has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 36.3% over the last two years.

Taking a step back, we can see that Duolingo’s margin expanded by 23.6 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Duolingo’s free cash flow clocked in at $147.8 million in Q1, equivalent to a 50.6% margin. This result was good as its margin was 6 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Duolingo’s Q1 Results

We liked that Duolingo beat analysts’ revenue and EBITDA expectations this quarter. On the other hand, its Q2 2026 and full-year bookings guidance both missed, and this is weighing on shares. The market seemed to be hoping for more, and the stock traded down 13.9% to $95.41 immediately after reporting.

Is Duolingo an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).