Since April 2021, the S&P 500 has delivered a total return of 60.2%. But one standout stock has more than doubled the market - over the past five years, Marriott has surged 134% to $348.15 per share. Its momentum hasn’t stopped as it’s also gained 30.8% in the last six months, beating the S&P by 32.6%.

Is there a buying opportunity in Marriott, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Marriott Will Underperform?

We’re glad investors have benefited from the price increase, but we're swiping left on Marriott for now. Here are three reasons why MAR doesn't excite us and a stock we'd rather own.

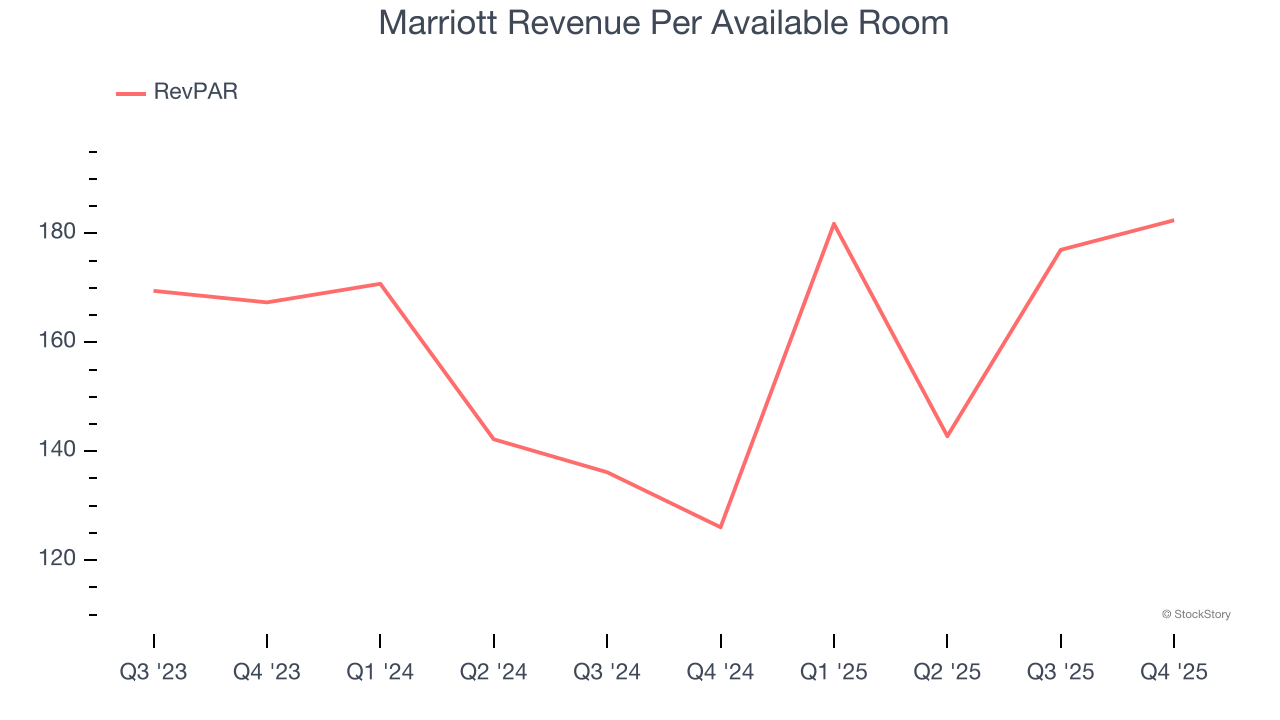

1. Weak RevPAR Growth Points to Soft Demand

We can better understand Consumer Discretionary - Travel and Vacation Providers companies by analyzing their RevPAR, or revenue per available room. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Marriott’s demand characteristics.

Marriott’s RevPAR came in at $182.43 in the latest quarter, and over the last two years, its year-on-year growth averaged 6.2%. This performance was underwhelming and suggests it might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

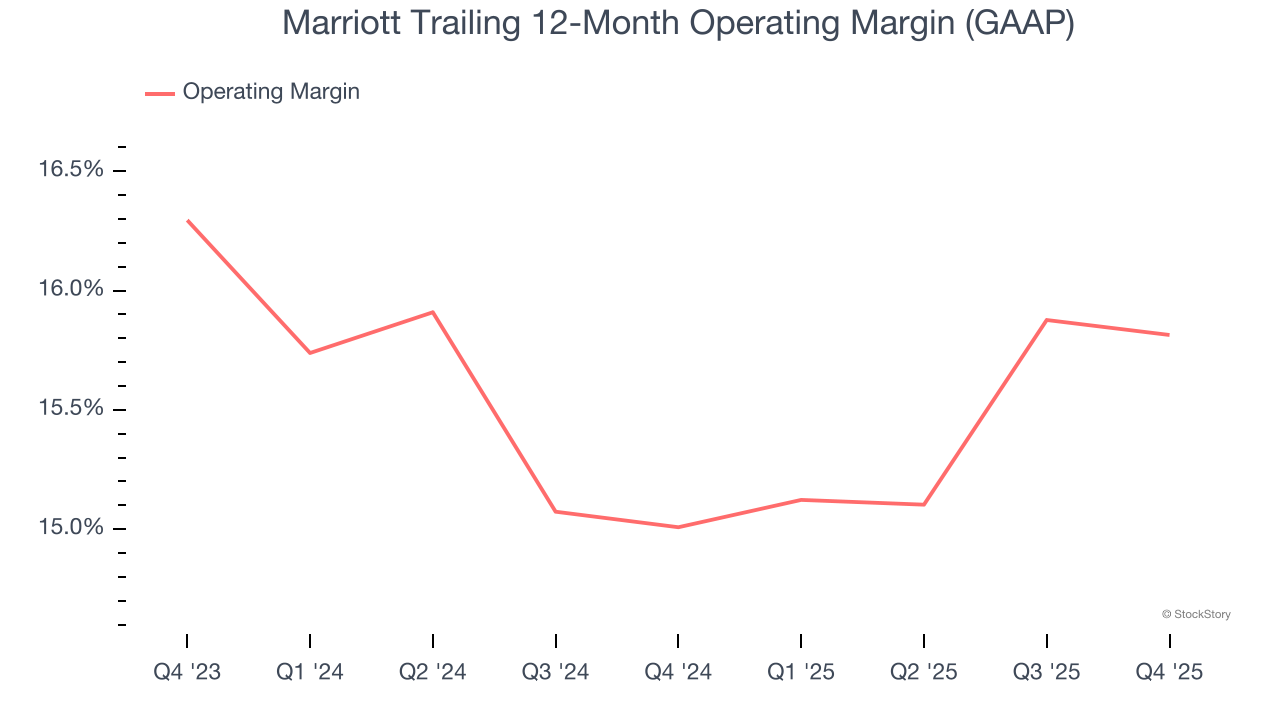

2. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Marriott’s operating margin has generally stayed the same over the last 12 months, and we generally like to see margin increases due to economies of scale and cost efficiency over time.

3. Projected Free Cash Flow Gains to Pump Profits

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Marriott’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 10% for the last 12 months will increase to 11.4%.

Final Judgment

Marriott doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 28.7× forward P/E (or $348.15 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than Marriott

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.