Over the past six months, Reynolds’s stock price fell to $20.84. Shareholders have lost 16.5% of their capital, which is disappointing considering the S&P 500 has climbed by 4%. This might have investors contemplating their next move.

Is now the time to buy Reynolds, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Reynolds Will Underperform?

Despite the more favorable entry price, we're cautious about Reynolds. Here are three reasons we avoid REYN and a stock we'd rather own.

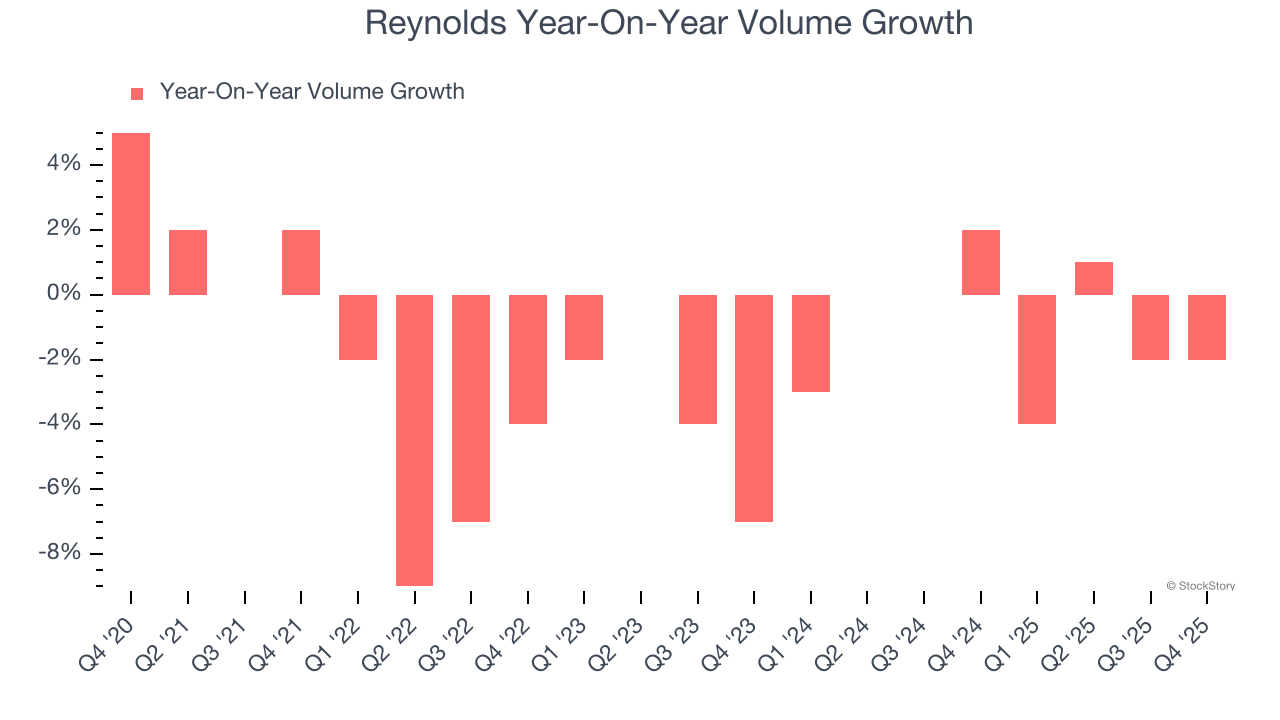

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Reynolds’s average quarterly sales volumes have shrunk by 1% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Reynolds’s revenue to stall. This projection is underwhelming and suggests its newer products will not catalyze better top-line performance yet.

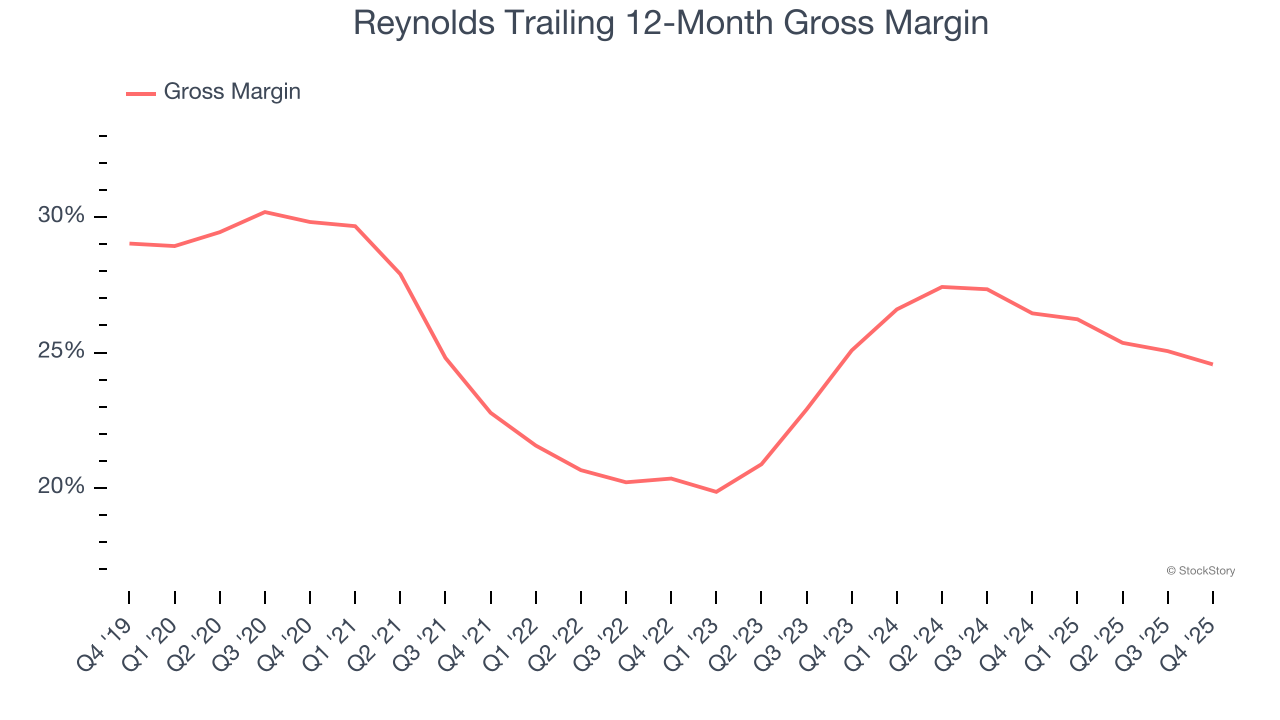

3. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Reynolds has bad unit economics for a consumer staples company, giving it less room to reinvest and develop new products. As you can see below, it averaged a 25.5% gross margin over the last two years. Said differently, for every $100 in revenue, a chunky $74.50 went towards paying for raw materials, production of goods, transportation, and distribution.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Reynolds, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 13.1× forward P/E (or $20.84 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.