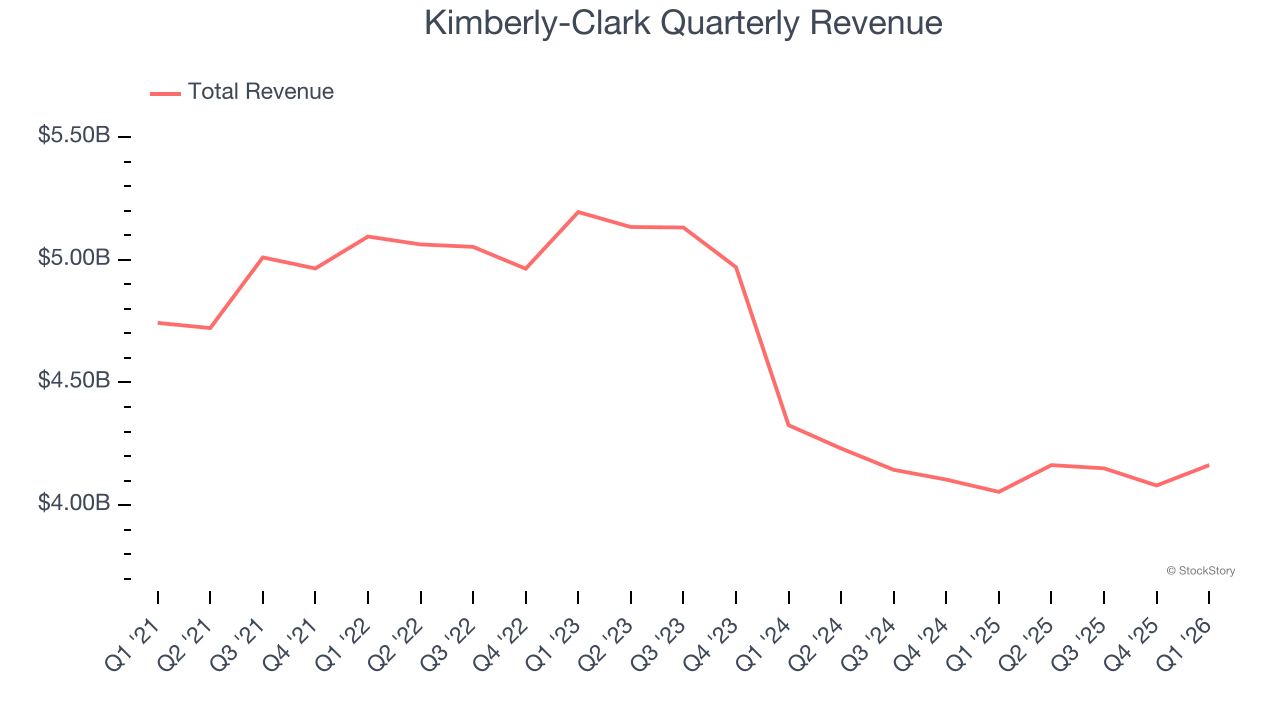

Household products company Kimberly-Clark (NASDAQ: KMB) announced better-than-expected revenue in Q1 CY2026, with sales up 2.7% year on year to $4.16 billion. Its non-GAAP profit of $1.97 per share was 2.2% above analysts’ consensus estimates.

Is now the time to buy Kimberly-Clark? Find out by accessing our full research report, it’s free.

Kimberly-Clark (KMB) Q1 CY2026 Highlights:

- Revenue: $4.16 billion vs analyst estimates of $4.1 billion (2.7% year-on-year growth, 1.6% beat)

- Adjusted EPS: $1.97 vs analyst estimates of $1.93 (2.2% beat)

- Adjusted EBITDA: $969 million vs analyst estimates of $897.2 million (23.3% margin, 8% beat)

- Operating Margin: 18.1%, up from 15.6% in the same quarter last year

- Free Cash Flow Margin: 7.7%, up from 3% in the same quarter last year

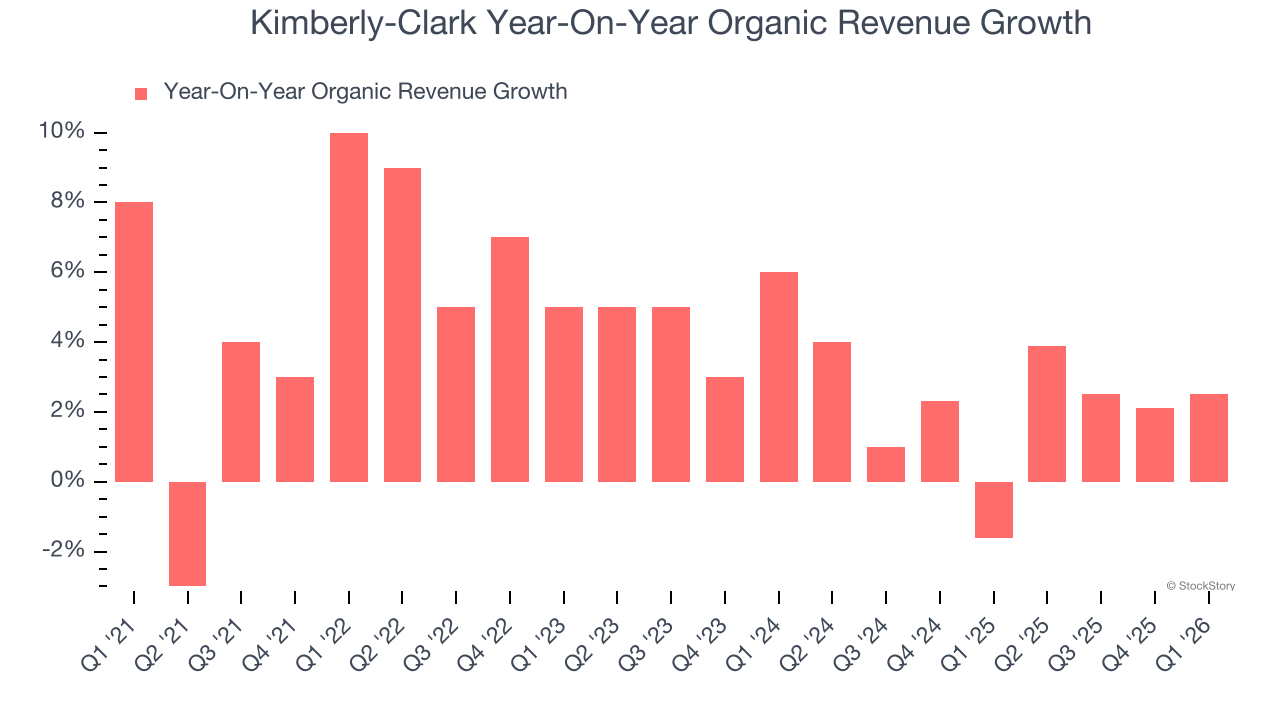

- Organic Revenue rose 2.5% year on year (beat)

- Market Capitalization: $32.61 billion

"Our first quarter results highlight the strength and resilience of the growth engine we've built through Powering Care," said Kimberly-Clark Chairman and CEO Mike Hsu.

Company Overview

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NASDAQ: KMB) is now a household products powerhouse known for personal care and tissue products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $16.56 billion in revenue over the past 12 months, Kimberly-Clark is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. For Kimberly-Clark to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, Kimberly-Clark struggled to generate demand over the last three years. Its sales dropped by 6.5% annually despite consumers buying more of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Kimberly-Clark reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 2% over the next 12 months. While this projection implies its newer products will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Kimberly-Clark’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 2.1%.

In the latest quarter, Kimberly-Clark’s organic sales rose by 2.5% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Kimberly-Clark’s Q1 Results

We were impressed by how significantly Kimberly-Clark blew past analysts’ EBITDA expectations this quarter. We were also happy its adjusted operating income outperformed Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 1% to $99.26 immediately after reporting.

Indeed, Kimberly-Clark had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).