Over the past six months, W. R. Berkley’s shares (currently trading at $66.20) have posted a disappointing 8.8% loss, well below the S&P 500’s 3.9% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Given the weaker price action, is now a good time to buy WRB? Find out in our full research report, it’s free.

Why Do Investors Watch WRB Stock?

Founded in 1967 and operating through more than 50 specialized insurance units across the globe, W. R. Berkley (NYSE: WRB) underwrites commercial insurance and reinsurance through specialized subsidiaries serving industries from healthcare to construction to transportation.

Three Positive Attributes:

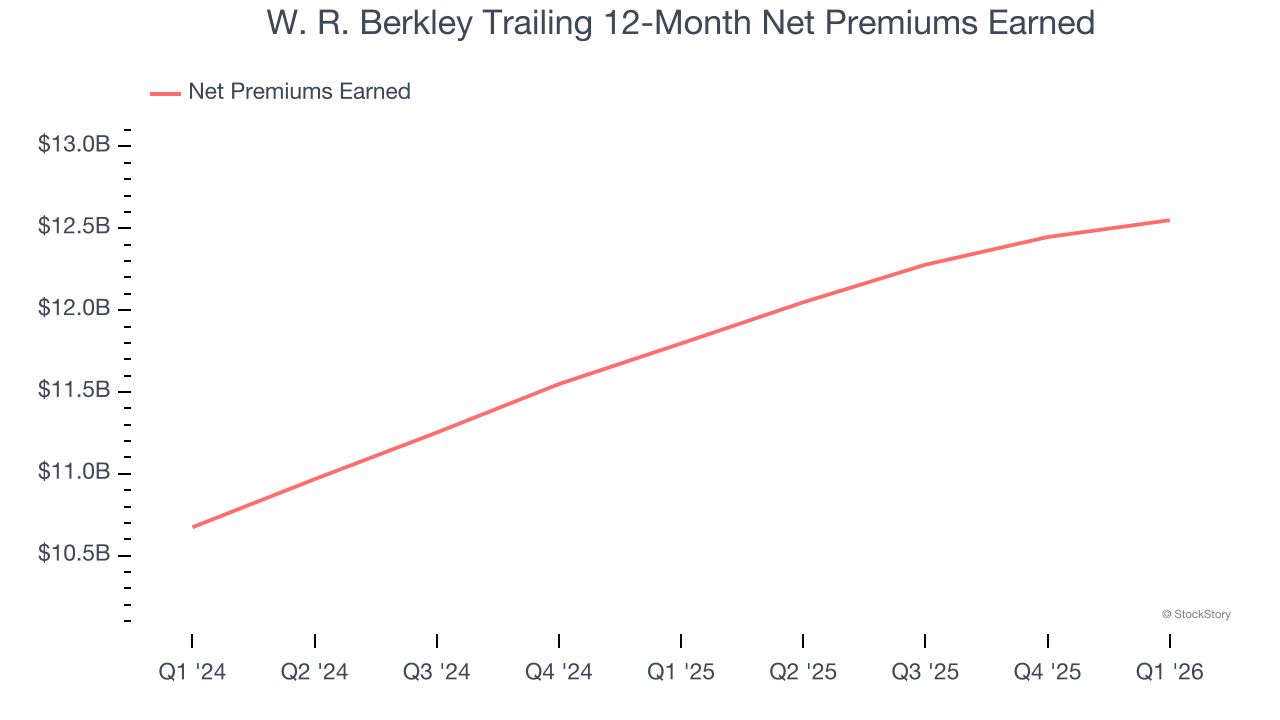

1. Net Premiums Earned Skyrocket, Fueling Growth Opportunities

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

W. R. Berkley’s net premiums earned has grown at a 12.1% annualized rate over the last five years, better than the broader insurance industry and in line with its total revenue.

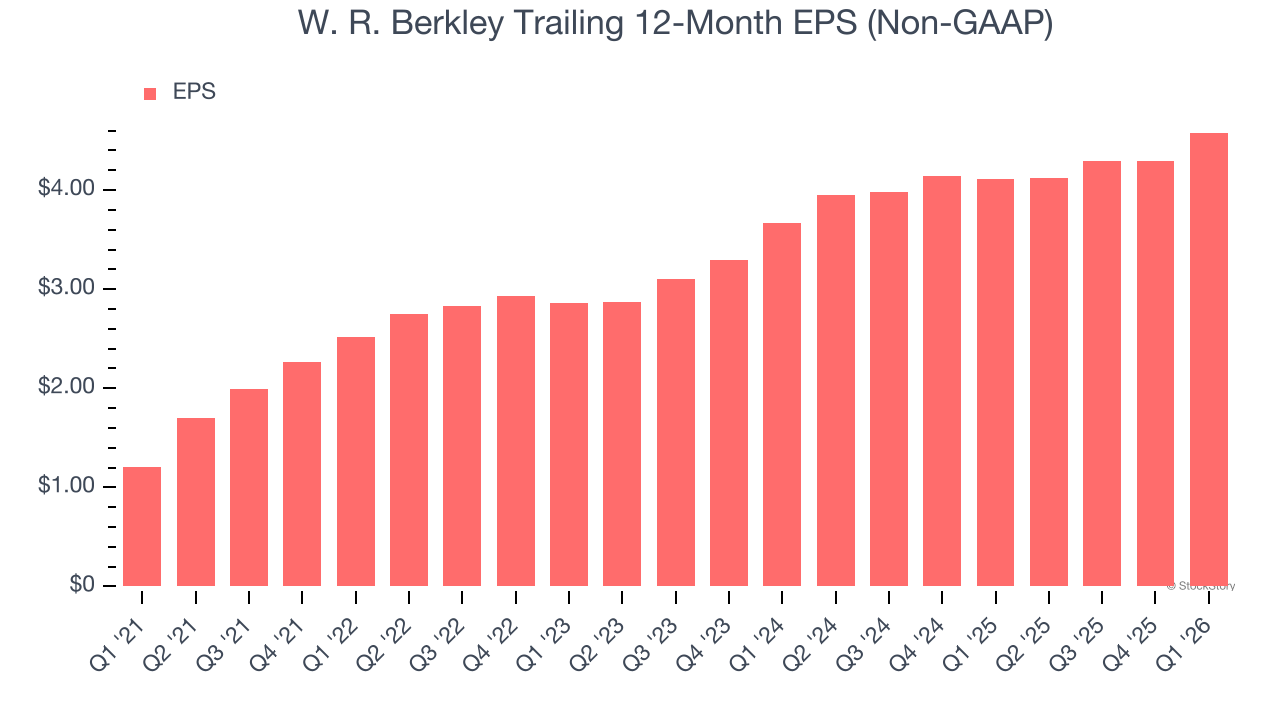

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

W. R. Berkley’s EPS grew at 30.6% compounded annual growth rate over the last five years, higher than its 12% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

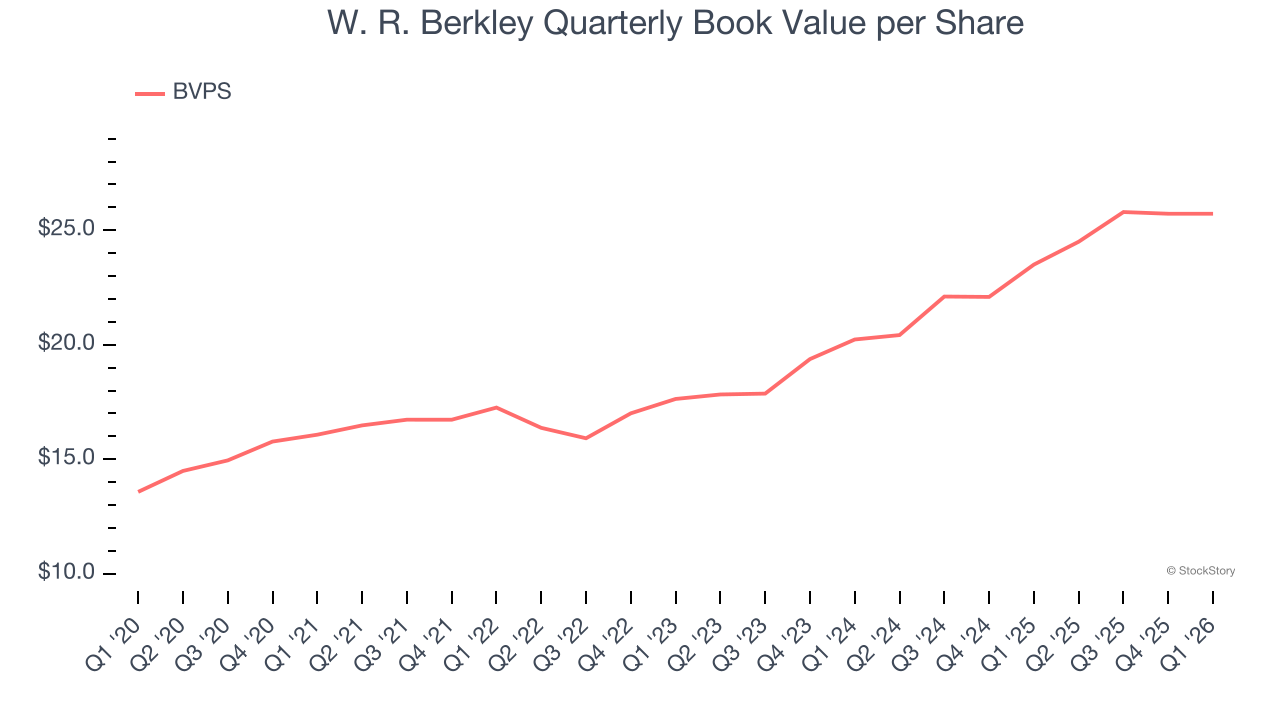

3. Projected BVPS Growth Is Remarkable

An insurer’s book value per share (BVPS) increases when it maintains a profitable pre-tax profit margin and effectively manages its investment portfolio.

Over the next 12 months, Consensus estimates call for W. R. Berkley’s BVPS to grow by 22.1% to $27.79, elite growth rate.

Final Judgment

W. R. Berkley is an interesting business with potential. With the recent decline, the stock trades at 2.4× forward P/B (or $66.20 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than W. R. Berkley

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.