Over the last six months, MetLife’s shares have sunk to $70.02, producing a disappointing 12.8% loss while the S&P 500 was flat. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in MetLife, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think MetLife Will Underperform?

Despite the more favorable entry price, we don't have much confidence in MetLife. Here are three reasons why MET doesn't excite us and a stock we'd rather own.

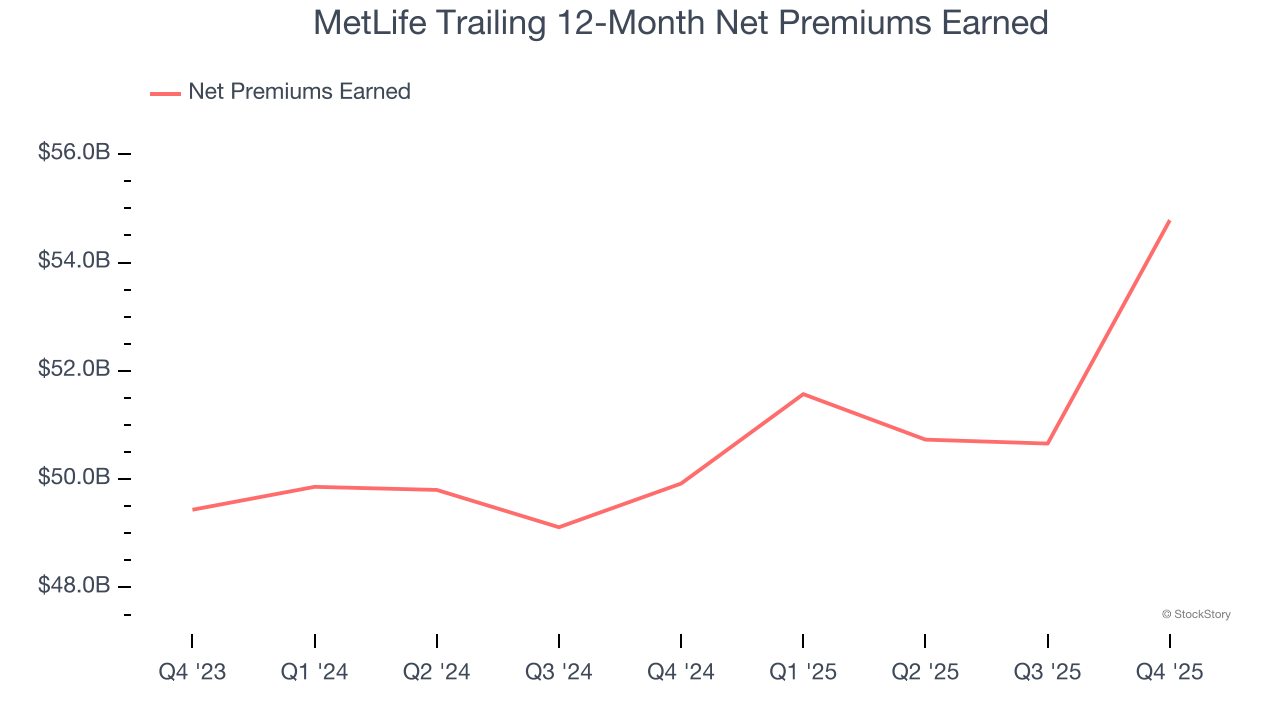

1. Net Premiums Earned Point to Soft Demand

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

MetLife’s net premiums earned has grown at a 2.8% annualized rate over the last five years, much worse than the broader insurance industry and in line with its total revenue.

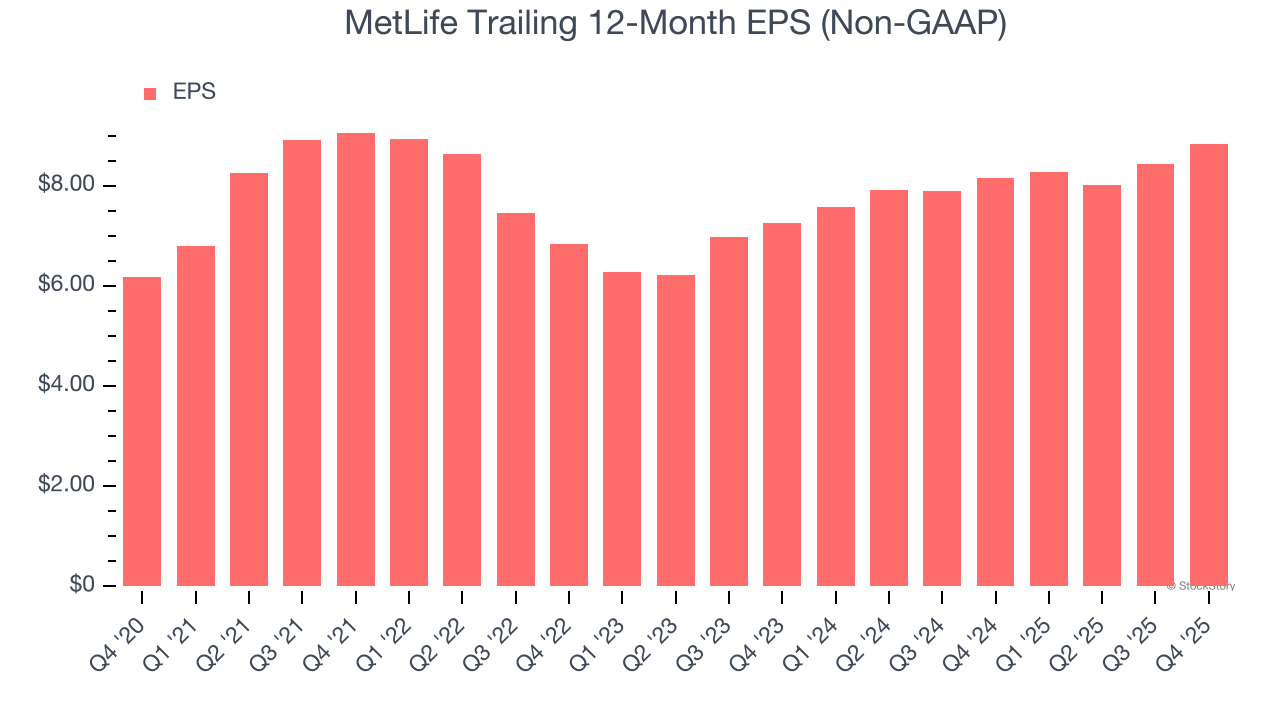

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

MetLife’s EPS grew at 7.5% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 3.5% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

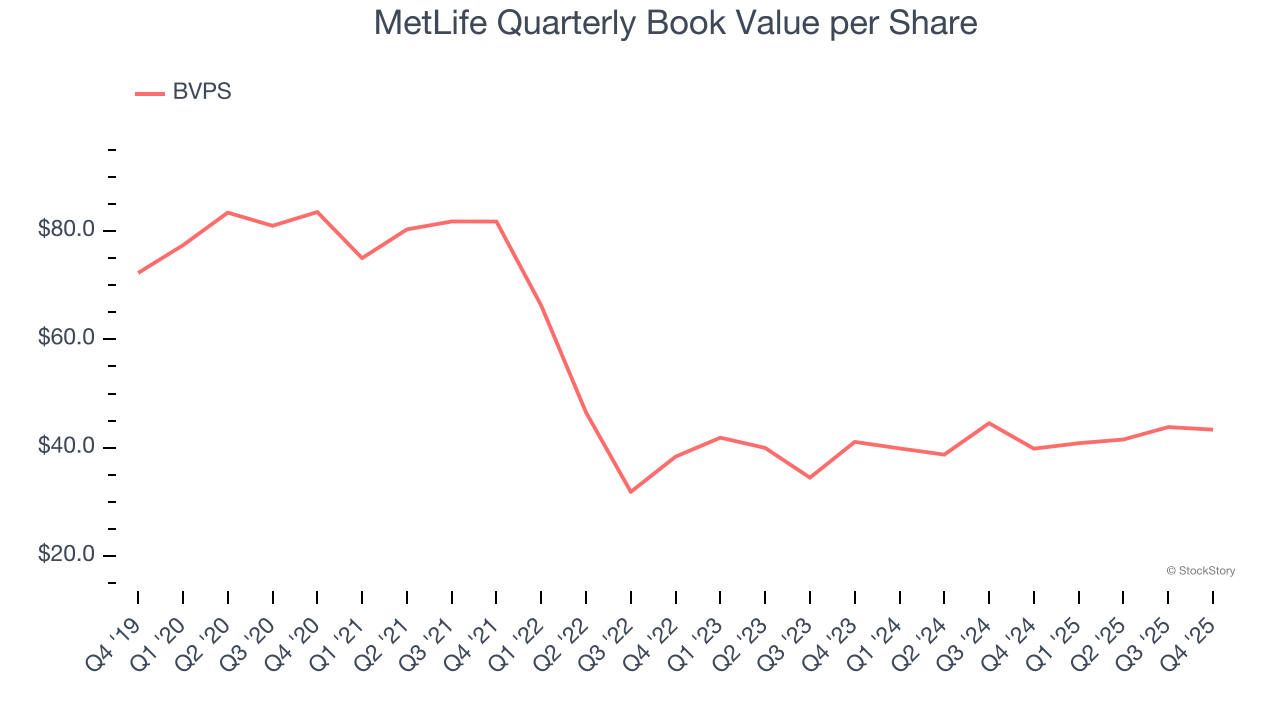

3. Substandard BVPS Growth Indicates Limited Asset Expansion

Book value per share (BVPS) serves as a key indicator of an insurer’s financial stability, reflecting a company’s ability to maintain adequate capital levels and meet its long-term obligations to policyholders.

Disappointingly for investors, MetLife’s BVPS grew at a sluggish 2.7% annual clip over the last two years.

Final Judgment

MetLife doesn’t pass our quality test. Following the recent decline, the stock trades at 1.5× forward P/B (or $70.02 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward the most dominant software business in the world.

Stocks We Would Buy Instead of MetLife

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.