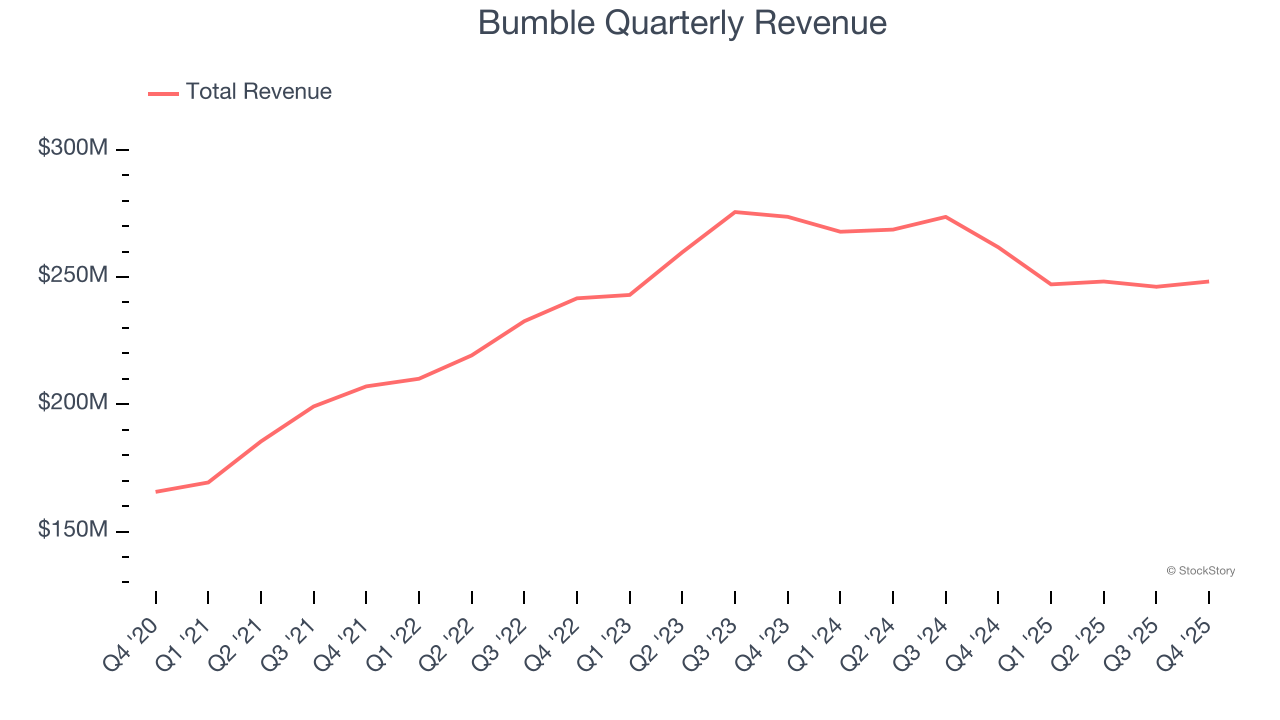

Online dating app Bumble (NASDAQ: BMBL) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 5.1% year on year to $248.2 million. On top of that, next quarter’s revenue guidance ($244 million at the midpoint) was surprisingly good and 15.9% above what analysts were expecting. Its GAAP loss of $2.45 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Bumble? Find out by accessing our full research report, it’s free.

Bumble (BMBL) Q4 CY2025 Highlights:

- Revenue: $248.2 million vs analyst estimates of $221.5 million (5.1% year-on-year decline, 12% beat)

- EPS (GAAP): -$2.45 vs analyst estimates of $0.22 (significant miss)

- Adjusted EBITDA: $94.59 million vs analyst estimates of $63.77 million (38.1% margin, 48.3% beat)

- Revenue Guidance for Q1 CY2026 is $244 million at the midpoint, above analyst estimates of $210.6 million

- EBITDA guidance for Q1 CY2026 is $81.5 million at the midpoint, above analyst estimates of $56.76 million

- Operating Margin: -136%, down from 14.1% in the same quarter last year

- Free Cash Flow Margin: 27.3%, down from 30% in the previous quarter

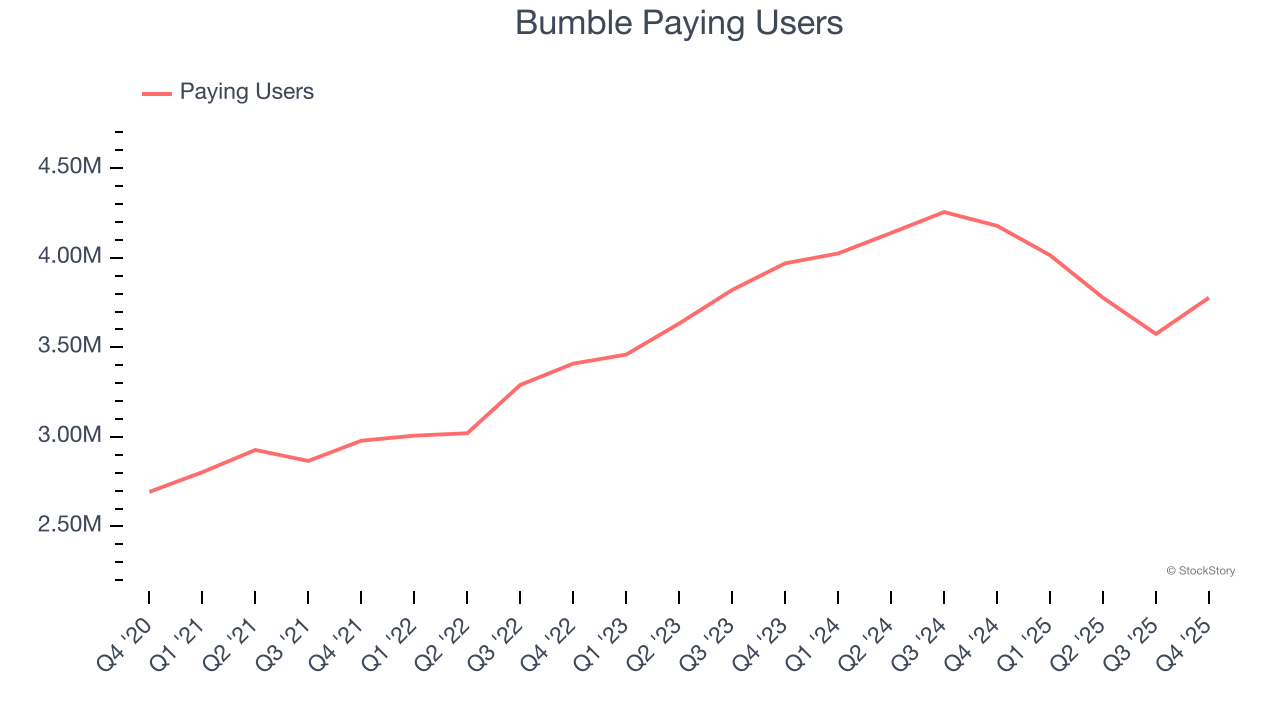

- Paying Users: 3.78 million, down 401,600 year on year

- Market Capitalization: $316.8 million

“Our second quarter results demonstrate how we are moving decisively and with conviction to build a durable foundation for Bumble’s future,” said Whitney Wolfe Herd, Founder & CEO of Bumble Inc.

Company Overview

Started by the co-founder of Tinder, Whitney Wolfe Herd, Bumble (NASDAQ: BMBL) is a leading dating app built with women at the center.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Bumble’s 3.1% annualized revenue growth over the last three years was sluggish. This fell short of our benchmark for the consumer internet sector and is a poor baseline for our analysis.

This quarter, Bumble’s revenue fell by 5.1% year on year to $248.2 million but beat Wall Street’s estimates by 12%. Company management is currently guiding for a 1.3% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 13.8% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Paying Users

Buyer Growth

As a subscription-based app, Bumble generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Bumble’s paying users, a key performance metric for the company, increased by 1.5% annually to 3.78 million in the latest quarter. This growth rate is one of the lowest in the consumer internet sector. If Bumble wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

Unfortunately, Bumble’s paying users decreased by 401,600 in Q4, a 9.6% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for buyers yet.

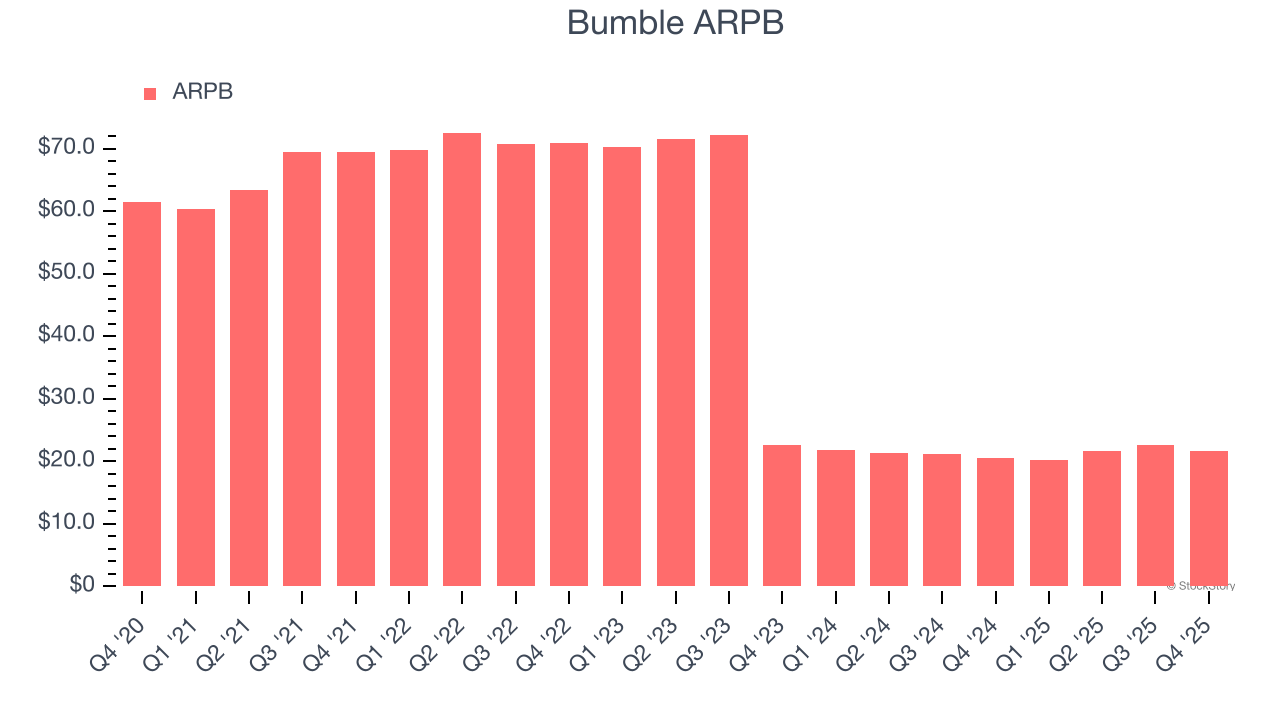

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the average buyer spends. ARPB is also a key indicator of how valuable its buyers are (and can be over time).

Bumble’s ARPB fell over the last two years, averaging 26.5% annual declines. This isn’t great when combined with its weaker paying users performance. If Bumble tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyer growth would be sustainable.

This quarter, Bumble’s ARPB clocked in at $21.69. It grew by 5.4% year on year, faster than its paying users.

Key Takeaways from Bumble’s Q4 Results

We were impressed by Bumble’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its number of buyers declined. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 21.7% to $3.51 immediately after reporting.

Bumble may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).