As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the thrifts & mortgage finance industry, including Annaly Capital Management (NYSE: NLY) and its peers.

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

The 22 thrifts & mortgage finance stocks we track reported a slower Q1. As a group, revenues missed analysts’ consensus estimates by 18.5%.

In light of this news, share prices of the companies have held steady as they are up 4.1% on average since the latest earnings results.

Annaly Capital Management (NYSE: NLY)

Operating as a real estate investment trust since 1996 with a focus on generating income from interest rate spreads, Annaly Capital Management (NYSE: NLY) is a diversified capital manager that invests in agency mortgage-backed securities, residential mortgage loans, and mortgage servicing rights.

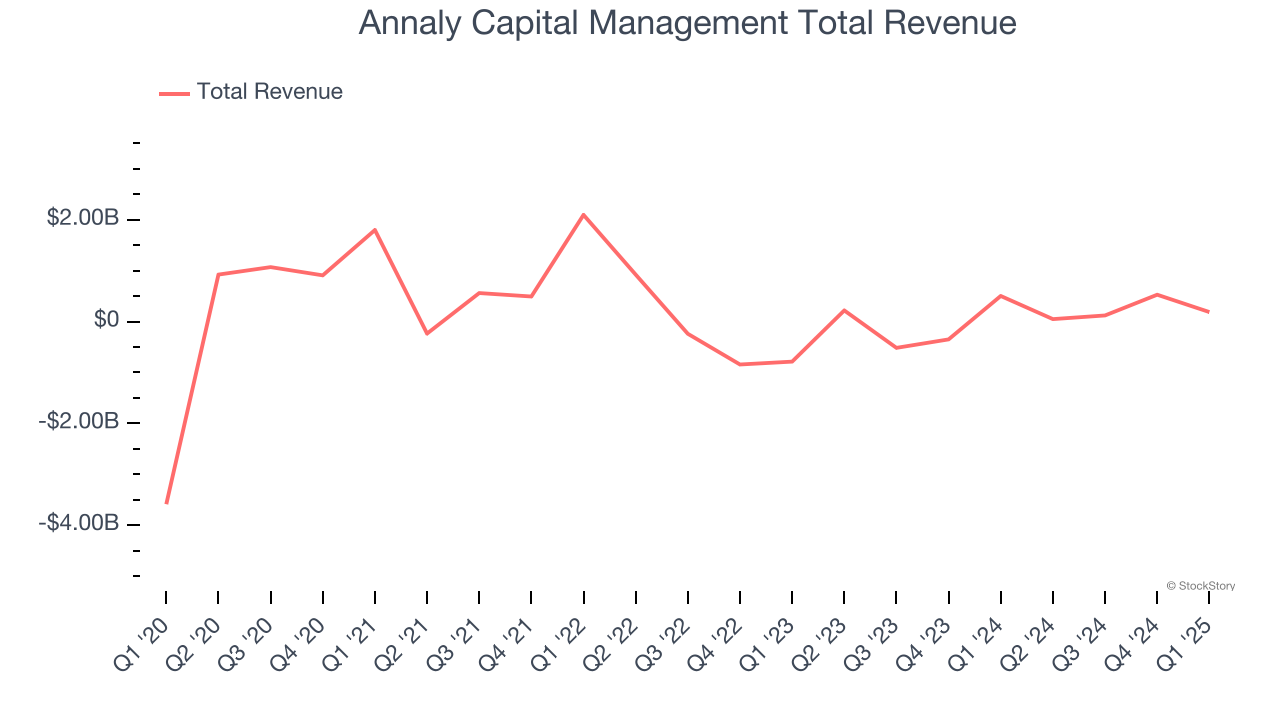

Annaly Capital Management reported revenues of $186.6 million, down 62.9% year on year. This print fell short of analysts’ expectations by 61.1%. Overall, it was a softer quarter for the company with a slight miss of analysts’ tangible book value per share estimates and EPS in line with analysts’ estimates.

Unsurprisingly, the stock is down 1.9% since reporting and currently trades at $19.49.

Read our full report on Annaly Capital Management here, it’s free.

Best Q1: Northwest Bancshares (NASDAQ: NWBI)

Founded in 1896 and operating across Pennsylvania, New York, Ohio, and Indiana, Northwest Bancshares (NASDAQ: NWBI) is a bank holding company that operates Northwest Bank, providing personal and business banking, investment management, and trust services.

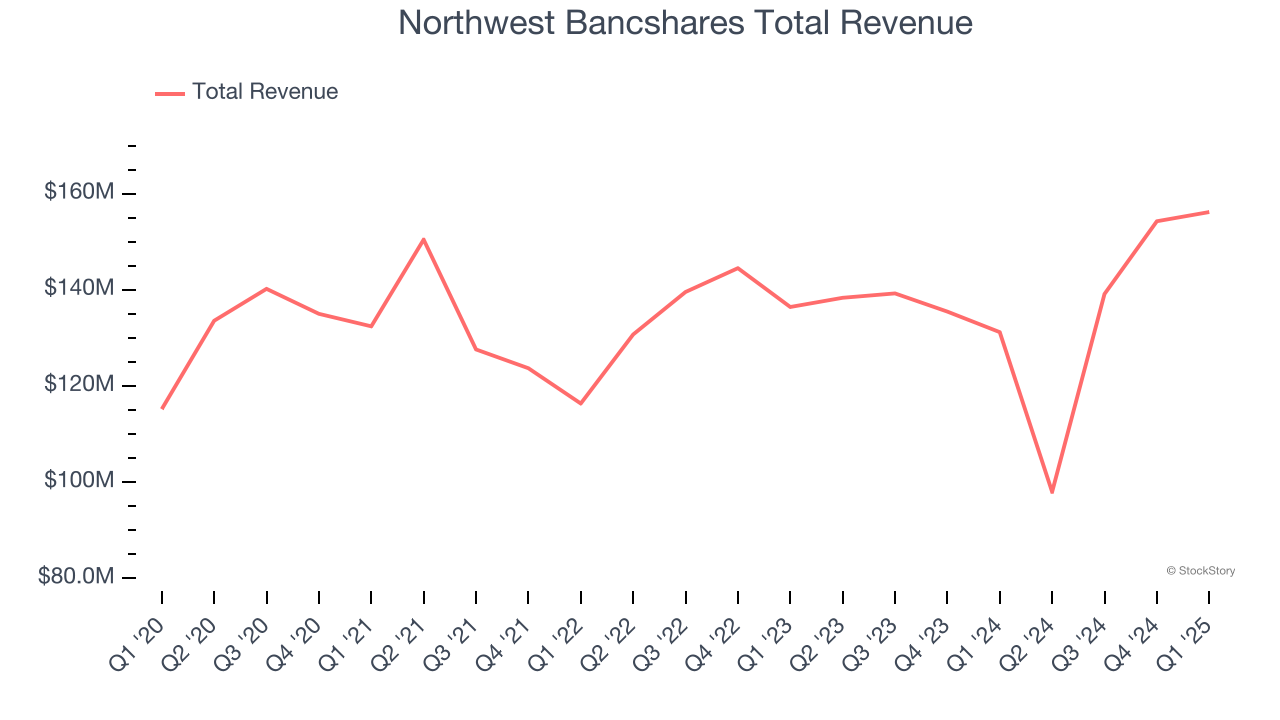

Northwest Bancshares reported revenues of $156.2 million, up 19% year on year, outperforming analysts’ expectations by 9.9%. The business had a stunning quarter with an impressive beat of analysts’ EPS and net interest income estimates.

The market seems happy with the results as the stock is up 8.1% since reporting. It currently trades at $12.77.

Is now the time to buy Northwest Bancshares? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Ladder Capital (NYSE: LADR)

Founded during the 2008 financial crisis when traditional lenders retreated from commercial real estate, Ladder Capital (NYSE: LADR) is a real estate investment trust that originates commercial real estate loans, owns commercial properties, and invests in real estate securities.

Ladder Capital reported revenues of $51.28 million, down 18.9% year on year, falling short of analysts’ expectations by 7.1%. It was a disappointing quarter as it posted a significant miss of analysts’ tangible book value per share and EPS estimates.

Interestingly, the stock is up 3.5% since the results and currently trades at $11.03.

Read our full analysis of Ladder Capital’s results here.

Mr. Cooper Group (NASDAQ: COOP)

Born from the 2018 merger of Nationstar Mortgage and WMIH Corp, Mr. Cooper Group (NASDAQ: COOP) is a non-bank servicer of residential mortgage loans that collects payments, manages escrow funds, and performs loss mitigation activities for 4.6 million customers.

Mr. Cooper Group reported revenues of $560 million, flat year on year. This number came in 9.1% below analysts' expectations. Overall, it was a disappointing quarter as it also produced a significant miss of analysts’ tangible book value per share estimates and EPS in line with analysts’ estimates.

The stock is up 14.7% since reporting and currently trades at $151.31.

Read our full, actionable report on Mr. Cooper Group here, it’s free.

Franklin BSP Realty Trust (NYSE: FBRT)

Operating as a specialized real estate investment trust (REIT) with roots dating back to 2012, Franklin BSP Realty Trust (NYSE: FBRT) originates and manages a diversified portfolio of commercial real estate debt investments secured by properties in the United States and abroad.

Franklin BSP Realty Trust reported revenues of $52.01 million, up 1.8% year on year. This print lagged analysts' expectations by 6%. Overall, it was a disappointing quarter as it also recorded a significant miss of analysts’ EPS estimates.

The stock is down 5.2% since reporting and currently trades at $10.93.

Read our full, actionable report on Franklin BSP Realty Trust here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.