Dollar Tree has had an impressive run over the past six months. While the S&P 500 has been flat, the stock has returned 33.9% and now trades at $85.99. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Dollar Tree, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Dollar Tree Not Exciting?

Despite the momentum, we don't have much confidence in Dollar Tree. Here are three reasons why DLTR doesn't excite us and a stock we'd rather own.

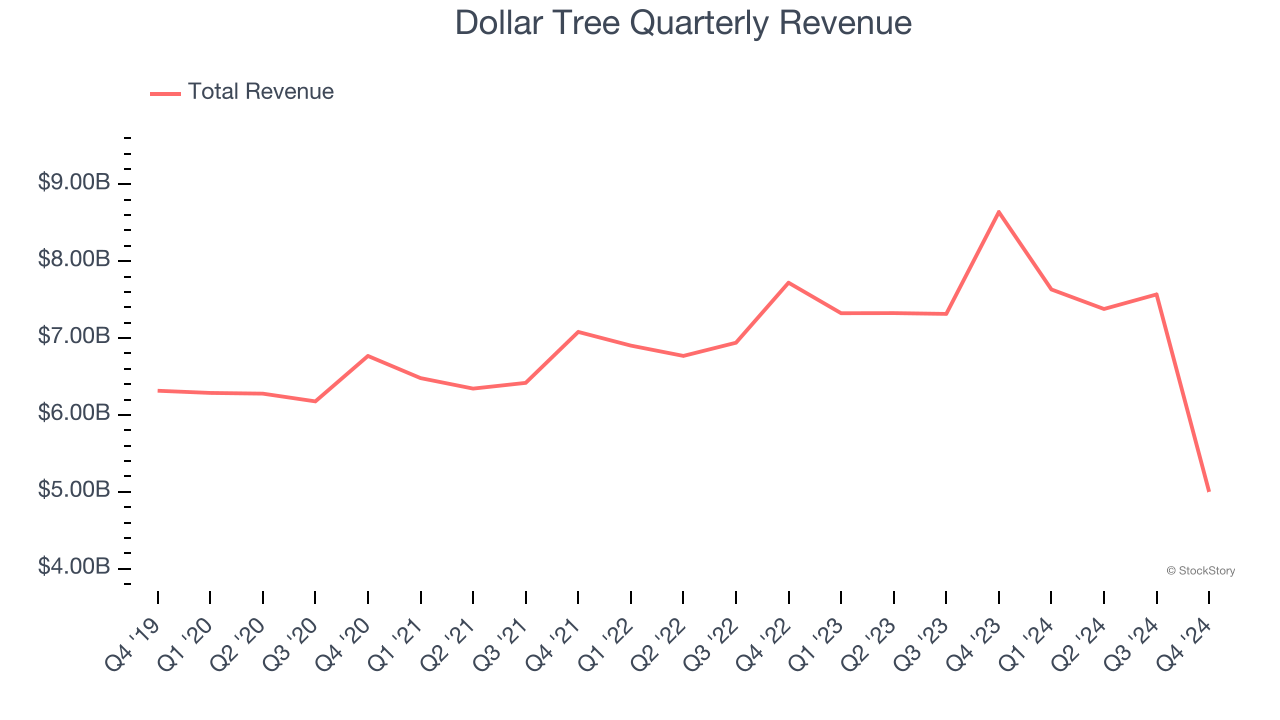

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Dollar Tree’s 3.2% annualized revenue growth over the last five years was sluggish. This was below our standard for the consumer retail sector.

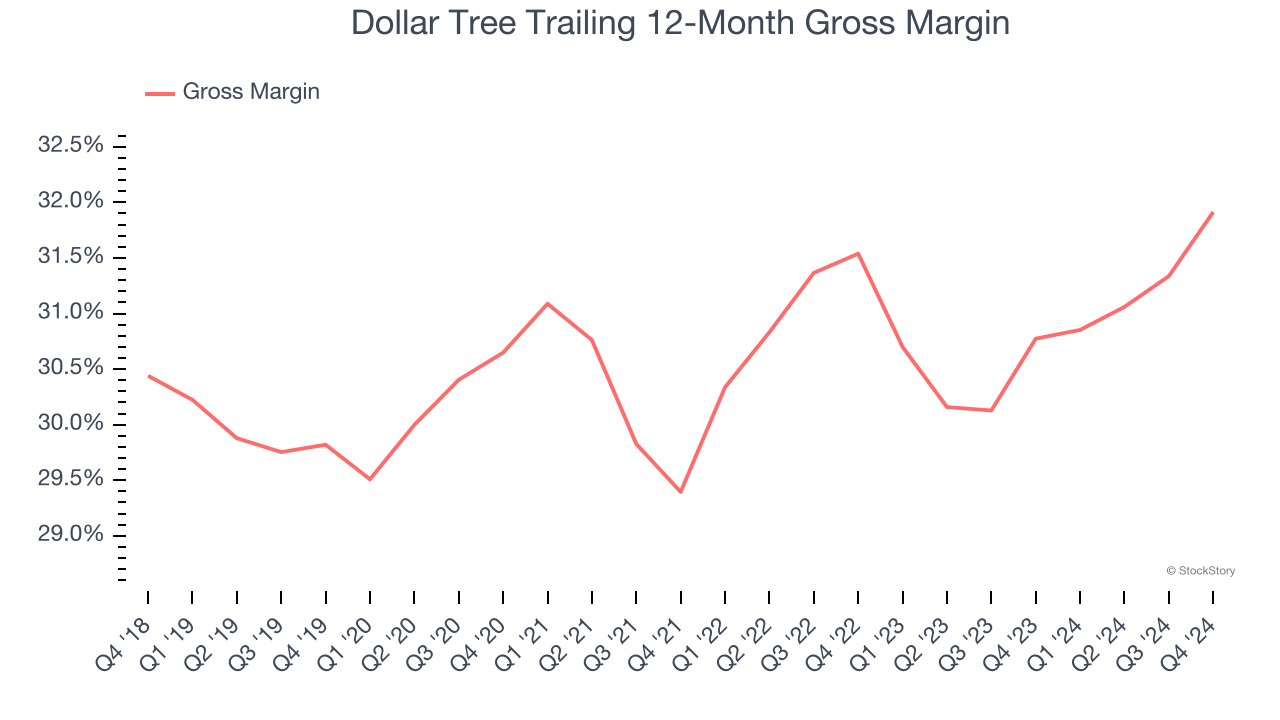

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Dollar Tree has bad unit economics for a retailer, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 31.3% gross margin over the last two years. Said differently, Dollar Tree had to pay a chunky $68.69 to its suppliers for every $100 in revenue.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Dollar Tree historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 9.8%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

Final Judgment

Dollar Tree isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 14.6× forward P/E (or $85.99 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

Stocks We Like More Than Dollar Tree

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.