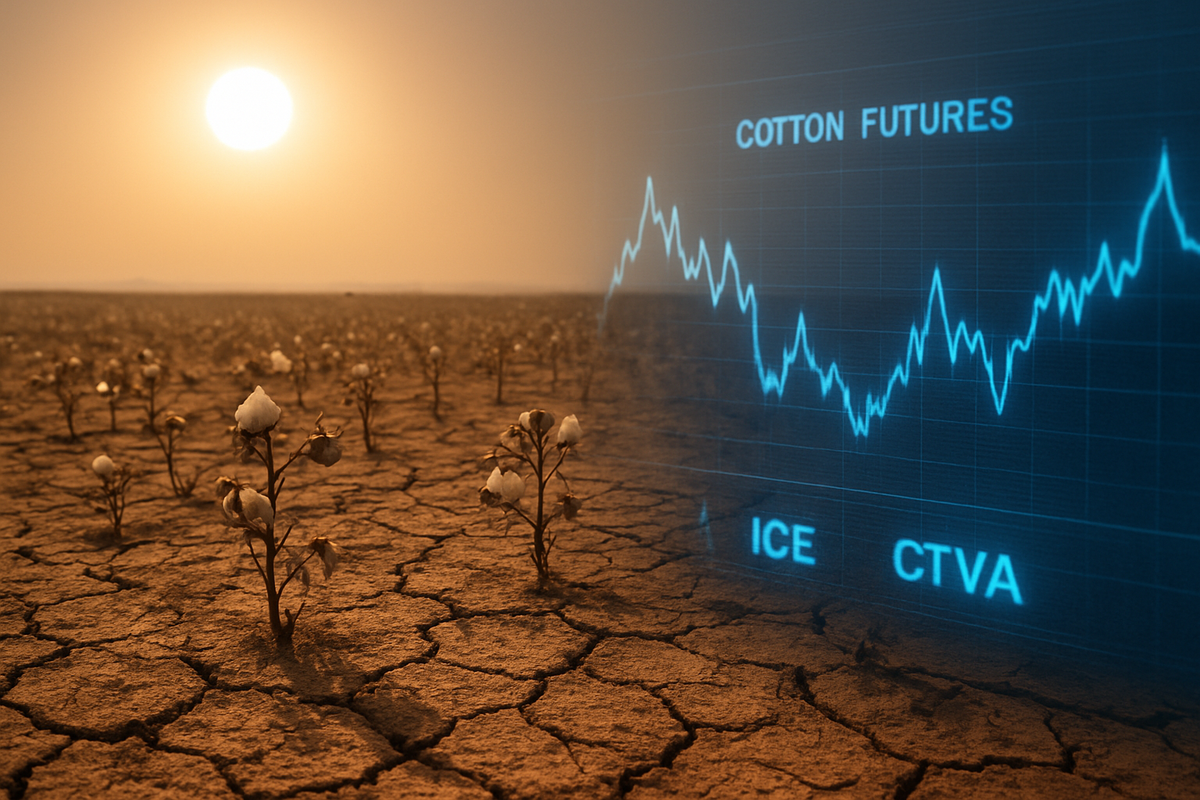

As of March 25, 2026, the United States cotton industry is staring down a generational crisis that threatens to destabilize global textile supply chains. A staggering 88% of U.S. cotton production areas are currently experiencing drought conditions, according to the latest U.S. Drought Monitor report. This represents a massive spike from the 33% coverage recorded just one year ago, marking one of the most rapid environmental deteriorations in the history of American fiber production.

The immediate implications are already rippling through the Intercontinental Exchange, Inc. (NYSE: ICE), where cotton futures have entered a period of extreme volatility. While the drought signals a severe supply crunch for the 2026 harvest, the market is simultaneously grappling with a massive "short squeeze" as institutional investors scramble to cover bearish bets. For farmers, the crisis is twofold: a lack of soil moisture to start the 2026 planting season and a pricing environment that, despite recent rallies, remains dangerously close to or below the cost of production.

The Arid Reality: A Timeline of the 2026 Cotton Crisis

The path to this looming disaster began in late 2025, driven by a persistent La Niña weather pattern that denied critical winter moisture to the "Cotton Belt." By February 2026, the situation in the Southwest—the heart of U.S. cotton production—had turned dire. Texas, which accounts for nearly half of all U.S. cotton acreage, saw 98% of its territory fall into drought categories ranging from "Severe" to "Exceptional." This environmental pressure has led to a projected 2026 crop of just 13.6 million bales, a significant downgrade from historical averages.

Stakeholders, including the U.S. Department of Agriculture (USDA) and economists at Texas A&M University, have expressed growing alarm over "abandonment" rates. Abandonment occurs when growers determine that a crop is too damaged to harvest and instead plow it under to claim insurance. With 88% of the crop land parched, industry experts warn that abandonment in 2026 could rival the record-shattering levels seen during the 2011 drought. This threat has forced a sudden reversal in market sentiment; as supply fears materialized in mid-March, cotton futures staged a dramatic recovery from 62 cents per pound toward the 68-cent mark.

The technical catalyst for this price action was the "unwinding" of massive net short positions held by managed money—essentially hedge funds and large institutional speculators. Entering 2026, these traders held near-record bearish positions, betting that weak global demand would keep prices low. However, the sheer scale of the drought forced these "managed money" players to buy back over 6,100 contracts in a single week this March, reducing their net short to approximately 66,754 contracts. This forced buying provided an artificial floor for prices, even as the fundamental outlook for the 2026 crop remained bleak.

Winners and Losers: Navigating the Fiber Fallout

The impact of this crisis is deeply bifurcated across the retail and agricultural sectors. Large-scale apparel retailers like The Gap, Inc. (NYSE: GPS) and American Eagle Outfitters, Inc. (NYSE: AEO) are facing a period of high uncertainty. These companies, which rely heavily on stable cotton prices for margin planning, are now navigating a landscape where raw material costs are highly volatile. While they may have some inventory hedged, a sustained supply shock in late 2026 could force price increases on basic goods like denim and t-shirts, potentially cooling consumer demand.

On the losing side of the ledger are the agricultural infrastructure providers. In the Southeast, companies like Corteva, Inc. (NYSE: CTVA) and local cotton gins are seeing a contraction in business as growers in states like Georgia pivot away from cotton in favor of more resilient or profitable crops like peanuts. For these firms, fewer cotton acres planted means lower sales of specialized seeds and chemicals, as well as reduced processing volume for ginning facilities. Conversely, V.F. Corporation (NYSE: VFC), the parent company of brands like The North Face, is attempting to mitigate these risks by aggressively investing in regenerative agriculture. By partnering with farmers who use water-retention techniques, they aim to "future-proof" their supply chain against the very drought conditions currently plaguing the market.

Retail giants like Walmart Inc. (NYSE: WMT) and Amazon.com, Inc. (NASDAQ: AMZN) may also see a shift in consumer behavior. As the unit price of cotton apparel imports rises—recent data suggests a 2–6% increase in the cost of basic cotton necessities—these "big box" retailers may see consumers prioritize essential purchases over discretionary fashion. This shift could squeeze the margins of mid-tier fashion brands while favoring value-oriented private labels owned by the retail behemoths.

A Broader Trend: Climate Volatility and Market Resilience

The 2026 cotton crisis is not an isolated event but rather a stark example of how climate volatility is becoming a primary driver of financial market behavior. Historically, cotton prices were dictated by global demand and stocks-to-use ratios. However, the current situation mirrors the "climate-driven" market cycles seen in the early 2010s, where environmental shocks overrode traditional demand metrics. This event fits into a broader industry trend where "managed money" is increasingly reactive to satellite-based drought monitoring rather than just quarterly economic reports.

The ripple effects of the U.S. drought will likely be felt globally. As the U.S. is the world’s leading cotton exporter, a 13.6-million-bale crop could tighten the global balance sheet, potentially benefiting international competitors in Brazil and Australia. Furthermore, this crisis may accelerate regulatory discussions regarding crop insurance and climate subsidies. If 88% of the production area remains in drought, the federal government may face mounting pressure to reform the Federal Crop Insurance Corporation's policies to address the "permanent" nature of drought in the Southwest.

Comparisons to the 2011-2012 "Cotton Cliff" are inevitable. During that period, prices spiked to nearly $2.00 per pound before crashing. While the current 68-cent range is far from those heights, the underlying soil moisture deficit is arguably worse today. The industry is watching to see if this drought will serve as the final catalyst for a mass migration of cotton production out of traditional "dryland" areas and into regions with more reliable irrigation or higher rainfall, a move that would fundamentally reshape the American agricultural map.

What Comes Next: The Sowing Window and Strategic Pivots

The next 60 days are critical for the U.S. cotton market. As the spring sowing window opens, farmers will have to make a "gamble" on whether to plant into dry dust in hopes of late-spring rains or to abandon their 2026 plans entirely. If widespread, "slow-soaking" precipitation does not arrive by May, the market should expect a secondary wave of short covering from hedge funds, which could propel prices toward the 80-cent break-even mark for the first time in years.

In the long term, strategic pivots are already underway. Expect to see apparel companies accelerate their transition to synthetic blends or recycled fibers to reduce their dependence on virgin cotton. For investors, the "managed money" positions will remain the most important indicator to watch. If institutional traders shift from a "net short" to a "net long" position, it will signal that the financial world has officially priced in a catastrophic harvest for 2026.

Market opportunities may emerge in "Ag-Tech" firms that specialize in drought-resistant seed traits and precision irrigation. As water becomes the most valuable commodity in the Cotton Belt, any technology that can produce a bale of cotton with 20% less water will see a massive surge in adoption. The coming months will determine if the 2026 season is a temporary setback or the beginning of a structural decline for U.S. cotton dominance.

Final Assessment: A Market in Flux

The looming crisis in the US cotton market is a sobering reminder of the fragility of global commodity chains. With 88% of production areas under environmental duress, the "White Gold" of the American South is under unprecedented pressure. While the recent price rally has provided a glimmer of hope for some traders, it is largely the result of speculative positioning rather than a genuine improvement in the agricultural outlook.

Moving forward, the market will be defined by its ability to adapt to a "low-moisture" reality. Investors should keep a close eye on weekly USDA crop progress reports and the Commitments of Traders (COT) data to gauge how quickly the "managed money" crowd is exiting its bearish bets. For the public companies involved, the test will be how well they can manage margins in a high-volatility environment where the weather, more than the consumer, is in the driver’s seat.

As we move toward the summer of 2026, the resilience of the U.S. farmer and the adaptability of the global textile industry will be put to the ultimate test. The "crisis of 88%" may well be remembered as the moment the cotton market was forced to reckon with the true cost of climate volatility.

This content is intended for informational purposes only and is not financial advice.