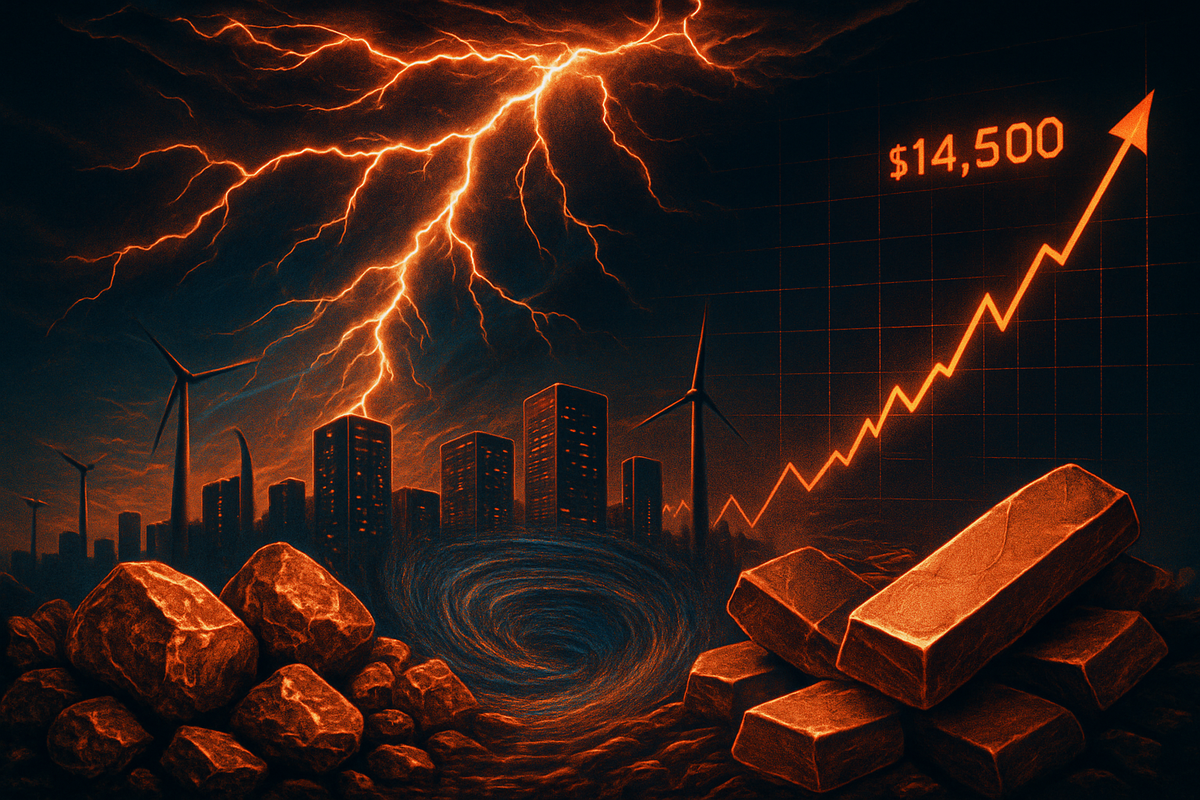

As of March 23, 2026, the global copper market has officially entered what analysts are calling a "Perfect Storm," with prices on the London Metal Exchange (LME) shattering all previous records to trade above $14,500 per tonne. This historic surge is the culmination of a massive 330,000 metric tonne (kmt) global supply deficit that has left industrial consumers scrambling for physical metal and pushed warehouse inventories to their lowest levels in over three decades.

The immediate implications of this price explosion are being felt across the global economy. From the automotive sector to renewable energy infrastructure, the rising cost of the "red metal" is threatening to derail decarbonization timelines and significantly inflate the cost of the next generation of artificial intelligence (AI) infrastructure. For the first time in history, copper has transitioned from a cyclical industrial commodity into a strategic national security asset, as world powers compete to secure the dwindling supplies required for the twin pillars of the 2020s economy: the green energy transition and the AI revolution.

The Road to $14,500: A Timeline of Scarcity

The journey to the current $14,500 per tonne milestone began in earnest during the second half of 2025, following a series of "Black Swan" events that decimated the global supply cushion. The most significant of these was the catastrophic mudslide at the Grasberg mine in Indonesia—operated by Freeport-McMoRan (NYSE: FCX)—in September 2025. The disaster flooded several levels of the Grasberg Block Cave, forcing a declaration of force majeure and wiping approximately 300,000 tonnes of production off the 2026 forecast. This event effectively erased the world's remaining supply surplus at a time when demand was beginning to accelerate exponentially.

Leading up to this moment, financial institutions like J.P. Morgan and Citigroup had been warning of a structural "supply cliff." Throughout 2024 and 2025, a lack of investment in new "greenfield" mining projects meant that as older mines in Chile and Peru saw declining ore grades, there were no new major projects ready to fill the gap. When the Grasberg disruption hit, it acted as a catalyst for a massive short squeeze in the futures markets. Initial market reactions were characterized by panic buying from Chinese smelters and Western industrial giants, who realized that the long-warned "structural scarcity" had finally arrived.

Winners and Losers in a High-Copper World

In this environment, the major mining houses hold unprecedented leverage. Rio Tinto (NYSE: RIO) has emerged as one of the primary beneficiaries of the current crisis. While other miners struggled with disruptions, Rio Tinto’s massive Oyu Tolgoi mine in Mongolia successfully completed its ramp-up to full production in late 2025, positioning the company to capture the full upside of the $14,500 price point. Similarly, BHP Group (NYSE: BHP), the world's largest miner, continues to reap massive profits from its Escondida operation in Chile, despite rising labor costs and social pressures in the region. BHP’s strategic $18 billion investment in the Vicuna project in Argentina is now seen as a masterstroke of foresight, though the project is still years away from adding significant supply.

Conversely, the "losers" in this scenario include heavy industrial consumers and electronics manufacturers. Public companies heavily dependent on copper wiring and components, such as electric vehicle pioneer Tesla (NASDAQ: TSLA) and power equipment giant ABB Ltd (NYSE: ABB), are facing severe margin compression. While these companies have attempted to pivot toward aluminum substitution where possible, the technical requirements for high-efficiency motors and power grids often make copper irreplaceable. Furthermore, the massive "hyperscalers" like Microsoft (NASDAQ: MSFT) and Alphabet (NASDAQ: GOOGL) are seeing the capital expenditure for their AI data centers skyrocket, as copper intensity in these facilities is three to four times higher than in traditional data centers.

The AI Boom and the Narrative of Structural Scarcity

The current crisis fits into a broader shift in how the world views industrial metals. For decades, copper demand was driven by Chinese urbanization; today, it is driven by the global "electrification of everything." The rise of generative AI has added a massive, unexpected layer of demand. AI data centers require sophisticated cooling systems and massive amounts of power distribution hardware, all of which are copper-heavy. A single 1-gigawatt AI campus, like those currently being proposed by major tech firms, can consume upwards of 50,000 tons of copper.

This shift has profound regulatory and policy implications. Governments in the United States, the European Union, and China are increasingly treating copper mines as critical infrastructure. This has led to a flurry of new mining-friendly policies aimed at fast-tracking permits, yet the physical reality of mining—where a new project can take 10 to 15 years from discovery to production—means that policy changes cannot solve the immediate deficit. Historically, this level of price pressure often leads to "demand destruction," but in 2026, the demand is largely inelastic because it is tied to non-negotiable climate goals and the competitive necessity of AI development.

What Comes Next: Substitution or Sustained Scarcity?

Looking ahead, the market faces two potential paths. In the short term, the extreme price of $14,500 per tonne will likely trigger a massive wave of copper recycling and urban mining. We can expect to see companies like Glencore (OTC:GLNCY) ramp up their recycling divisions to recover copper from old electronics and discarded infrastructure. However, secondary supply is rarely enough to bridge a 330 kmt deficit. If prices remain at these levels or climb toward the $15,000 "incentive price" target, we may see a more aggressive shift toward aluminum in the automotive and utility sectors, despite the loss in conductivity and efficiency.

The long-term challenge remains the "supply gap." Even if the Grasberg mine returns to full capacity by 2027, the underlying trend of 3% to 4% annual demand growth driven by the green transition and AI is expected to persist. This suggests that the "Perfect Storm" of 2026 is not a temporary spike, but the beginning of a new high-plateau for copper prices. Strategic pivots will be required; mining companies may seek more aggressive M&A to consolidate existing assets, while tech giants may look to take direct equity stakes in mining projects to ensure their "Stargate" AI projects aren't stalled by a lack of wiring.

Wrapping Up: The Red Metal's New Reality

The copper market of 2026 has provided a stark lesson in the limits of resource availability in a high-tech world. The combination of the Grasberg disruption and the insatiable appetite of AI data centers has created a 330 kmt deficit that cannot be quickly closed. With prices firmly above $14,500, the "Red Metal" has redefined itself as the essential backbone of the modern digital and green economy.

Moving forward, the market is likely to remain in a state of high volatility. Investors should keep a close eye on the restart progress at Freeport-McMoRan's Grasberg site and the pace of "hyperscaler" data center builds. If the deficit persists into 2027, the $15,000 price target may quickly become the new floor rather than the ceiling. In the coming months, the ability of companies to manage their supply chains and adapt to these historic costs will separate the winners from the losers in this new era of structural scarcity.

This content is intended for informational purposes only and is not financial advice