Seagate Technology (STX) delivered a fiscal third-quarter 2026 performance that has fundamentally reset Wall Street’s expectations for the company, transforming what was previously considered an optimistic scenario into the new consensus outlook. Revenue of $3.11 billion exceeded estimates by 5.4%, representing 44% year-over-year growth, while non-GAAP earnings per share of $4.10 surpassed the $3.48 consensus by more than 17%. Perhaps most critically, management guided fiscal fourth-quarter revenue to $3.45 billion and EPS to $5.00, both dramatically above Street expectations of $3.16 billion and $3.97, respectively.

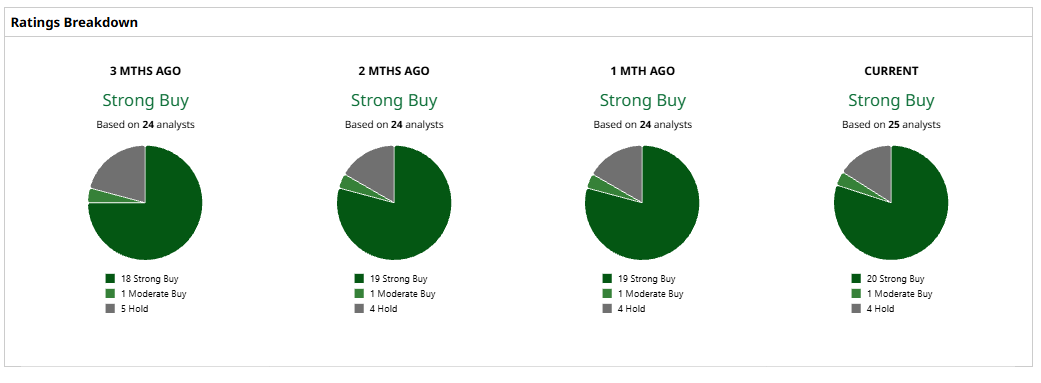

The magnitude of the earnings surprise triggered an immediate and sweeping reassessment across Wall Street. Rosenblatt doubled its price target to $1,000 from $500, representing the most aggressive HDD call of 2026. Bank of America lifted its target to $840, Barclays to $750, Citi to $740, and Goldman Sachs nearly doubled its target to $700 from $385. Morgan Stanley reaffirmed Seagate as a top pick, characterizing the company as “stronger for longer.” Only UBS maintained a cautious stance, raising its target modestly to $545 while keeping a “Neutral” rating and warning that structural improvements may already be priced in.

The structural underpinnings of the bull case rest on three pillars that now appear increasingly durable. First, nearline HDD capacity is fully allocated through calendar 2027, with hyperscale customers already engaging in supply discussions for 2028, a dramatic acceleration from just three months ago when 2027 conversations were only beginning. Second, Seagate’s HAMR-based Mozaic platform has been qualified with five of the world’s largest cloud customers, delivering meaningful cost-per-bit advantages that underwrite margin expansion. Third, the HDD industry operates as a functional oligopoly with only Seagate and Western Digital (WDC) controlling the vast majority of supply, creating sustained pricing power.

The margin profile transformation has been extraordinary. Non-GAAP gross margins expanded from 36.2% to 47.0% in a single year, while operating margins surged to 37.5%, up 1,400 basis points year-over-year. Free cash flow reached $953 million in the quarter, approaching $1 billion and representing a 30.6% free cash flow margin. Management raised its longer-term annual revenue growth target to a minimum of 20%, up from previous guidance in the low-to-mid teens.

The AI-driven data storage demand cycle is the fundamental catalyst. Data center revenue reached $2.5 billion, up 55% year-over-year and now representing 80% of total company revenue. CEO Dave Mosley characterized the current environment as “a new era of structural growth,” emphasizing that AI applications are amplifying data creation across video, cloud platforms, and agentic AI workloads.

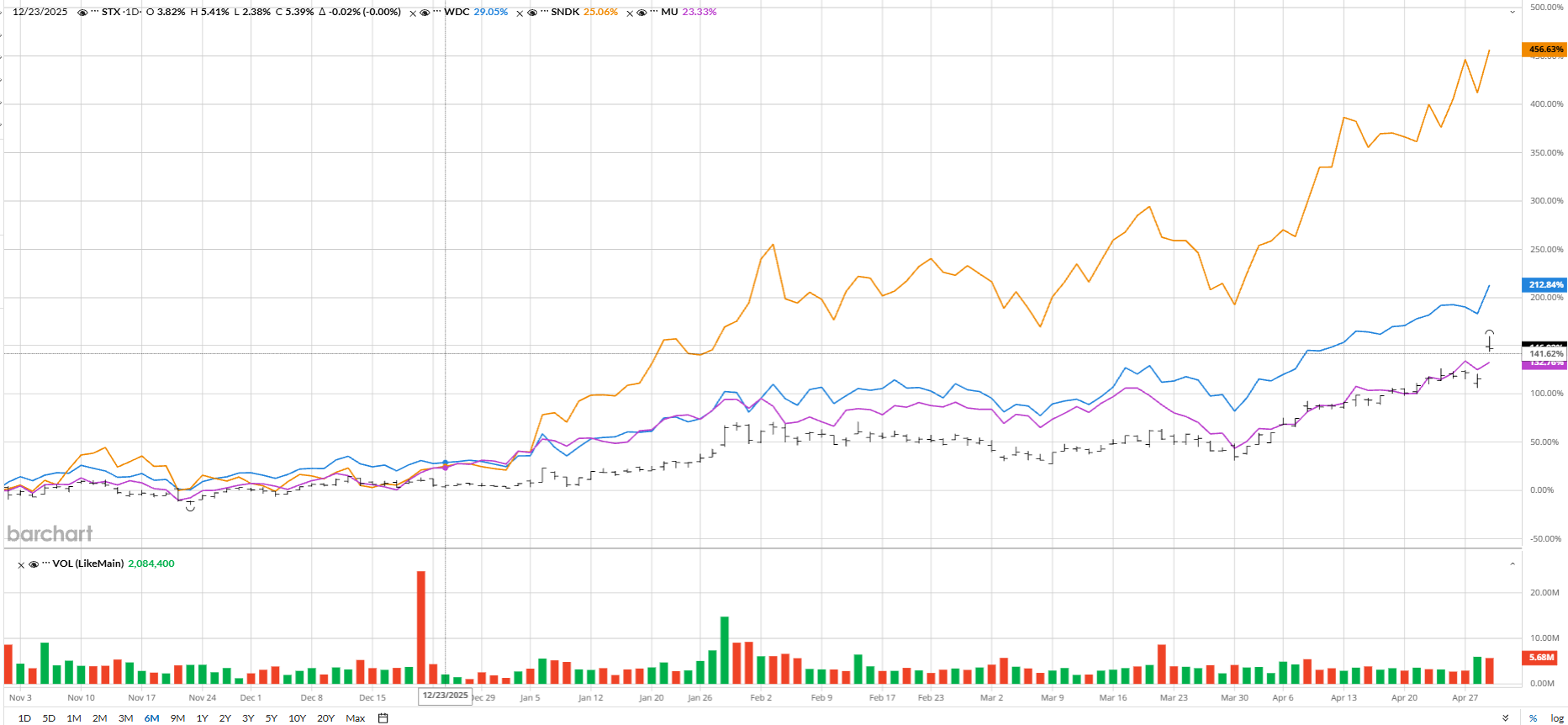

The broader storage ecosystem responded emphatically, with Seagate shares surging approximately 14% on the day, pulling Western Digital (WDC) up nearly 10%, SanDisk (SNDK) up 8%, and Micron (MU) up approximately 4%. The four storage companies were on track to add over $60 billion in combined market value, underscoring institutional conviction that the storage demand narrative extends well beyond a single company.

Risks remain material despite the overwhelming bullish sentiment. Seagate shares have rallied 141% year-to-date and approximately 714% over the trailing 12 months.

The bear case centers on cyclicality. If hyperscaler capital expenditure normalizes, solid-state drives encroach on nearline workloads, or the macro environment deteriorates amid elevated oil prices and geopolitical tensions surrounding the Iran conflict, today’s pricing power could erode. The stock’s extraordinary run means significant good news is already embedded in the price, and prudent investors should consider position sizing accordingly even as the fundamental trajectory remains compelling.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Sarah Holzmann did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Down Nearly 50% from All-Time Highs, Should You Buy the dip in POET Technologies Stock?

- ‘I’d Love to Be Able to Save an Airline,’ Says Trump About Spirit. But Is There Any Saving FLYYQ Stock?

- Semiconductor Stocks Are the New Elephant in the Room at 14% of the S&P 500. How to Play This Tech Super-Sector.

- As Alibaba Rolls Out the Happy Horse AI Model, Should You Buy, Sell, or Hold BABA Stock?