The race to power artificial intelligence (AI) is rapidly becoming the defining constraint of the next phase of the digital economy, and Meta Platforms (META) is signaling just how far the industry may need to go. In a recent move that underscores the scale, Meta has partnered with private startup Overview Energy to secure up to 1 gigawatt of space-based solar power, an emerging technology that collects energy in orbit and beams it back to Earth for continuous, 24/7 use.

This is a direct response to the explosive growth in energy demand driven by AI data centers, where power availability is increasingly becoming a bottleneck to scaling compute infrastructure. By tapping solar energy beyond the constraints of terrestrial grids, where intermittency, land use, and permitting challenges persist, Meta is effectively placing a long-duration bet on orbital energy as a baseload solution for AI workloads.

For investors, however, the more actionable angle may lie not with Meta, but with the defense and aerospace company that has quietly been developing similar capabilities for years. Northrop Grumman Corporation (NOC) has a long history of investing in space-based solar power concepts.

The well-known defense firm has been one of the earliest and most consistent players in space-based solar power, primarily through its Space Solar Power Incremental Demonstrations and Research (SSPIDR) program and related partnerships.

At a high level, the company’s efforts focus on solving three core technical challenges: collecting solar energy in orbit, converting it into transmittable energy (radio frequency/microwave), and accurately beaming it back to Earth.

In recent years, Northrop has made tangible progress. It has successfully demonstrated beam-steering technology, a critical capability that allows energy to be directed precisely to ground receivers, validating a key component of its planned orbital system. The next milestone is a prototype satellite demonstration (Arachne) intended to show end-to-end power transmission from space.

Northrop Grumman’s efforts position it as a first-mover in the engineering backbone of space-based solar power, with proven components, defense-backed funding, and a near-term demonstration roadmap, potentially giving it an edge.

About Northrop Grumman Stock

Northrop Grumman is a leading American aerospace and defense contractor specializing in advanced systems across aeronautics, space, mission systems, and defense technologies. The company is headquartered in Falls Church, Virginia and plays a critical role in U.S. national security through programs spanning stealth aircraft, missile systems, and space infrastructure. Northrop Grumman has a market cap of $82.1 billion.

Over the past 52 weeks, the stock has delivered 17.86% returns, supported by robust defense demand, strong backlog growth, and exposure to high-priority programs such as the B-21 bomber and missile systems. This places it solidly during a period of elevated geopolitical tensions.

However, year-to-date (YTD) performance has been more muted, with the stock up down marginally. This was fueled by recent earnings, which, despite beating expectations, triggered a pullback as investors reacted to higher capital expenditures and concerns around peak defense spending, contributing to near-term pressure on the stock. It plunged almost 7% on April 21 following the release and 3.5% on April 22.

The stock is currently trading at a slight premium compared to industry peers at 20.65 times forward earnings.

Q1 Results Beat Expectations

Northrop Grumman reported its first quarter 2026 results on April 21, delivering a solid operational performance that modestly exceeded market expectations but failed to drive a positive stock reaction due to already elevated investor expectations.

Revenue came in at $9.88 billion, representing 4% year-over-year (YOY) growth. Earnings performance was notably stronger, with EPS rising to $6.14 from $3.32 a year earlier (85% YOY increase) and exceeding expectations, reflecting improved program execution. Net earnings increased 82% YOY to $875 million from $481 million, while operating margin expanded to 10% from 6.1%, indicating significant margin recovery.

Segment-wise, growth was led by Aeronautics Systems, with 17% YOY growth driven by the B-21 bomber program, alongside 5% growth in Defense Systems and modest growth in Mission Systems, partially offset by a decline in Space Systems. Also, the company reported a backlog of $95.6 billion, underscoring strong demand visibility.

Further, the report highlighted continued momentum in key strategic programs, including the B-21 Raider, Sentinel program, and missile systems, supported by elevated global defense spending. However, management flagged supply chain constraints and longer international sales cycles as ongoing headwinds.

On the other hand, the company reaffirmed its FY2026 revenue outlook at $43.5 billion to $44 billion and adjusted EPS guidance at $27.40 to $27.90.

Analysts remain upbeat, projecting EPS of $27.86 for fiscal 2026, up 5.8% YOY, and anticipating a further 8.4% annual increase to $30.19 in fiscal 2027.

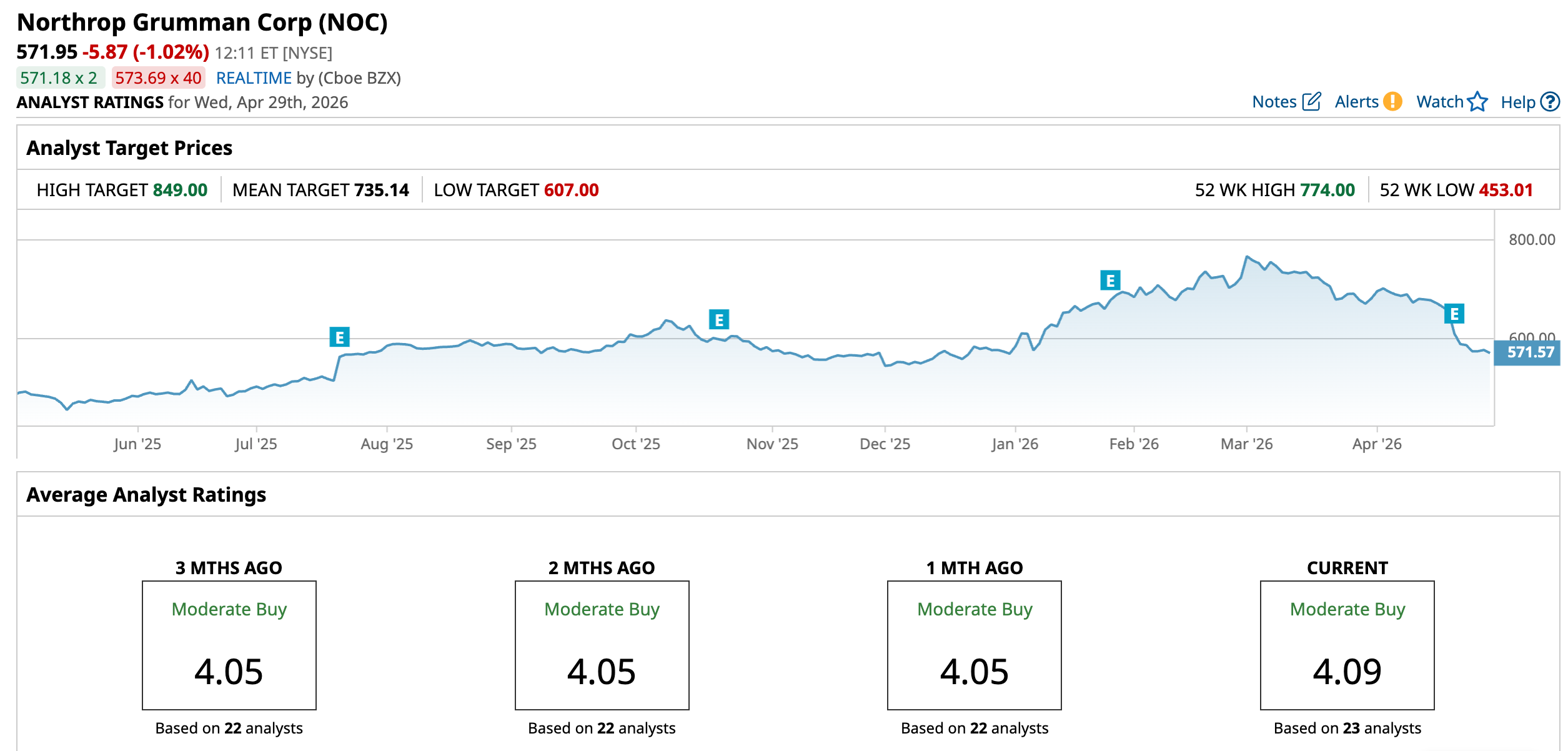

What Do Analysts Expect for Northrop Grumman Stock?

Bernstein SocGen reiterated a “Market Perform” rating on Northrop Grumman with a $765 price target, earlier this month.

On the other hand, Jefferies raised its price target on Northrop Grumman to $710 (from $690) amid anticipated margin expansion, but maintained a “Hold” rating.

Meanwhile, Wells Fargo initiated coverage on Northrop Grumman with an “Overweight” rating and an $800 price target, citing strong long-term growth driven by major programs like the B-21 bomber and GBSD.

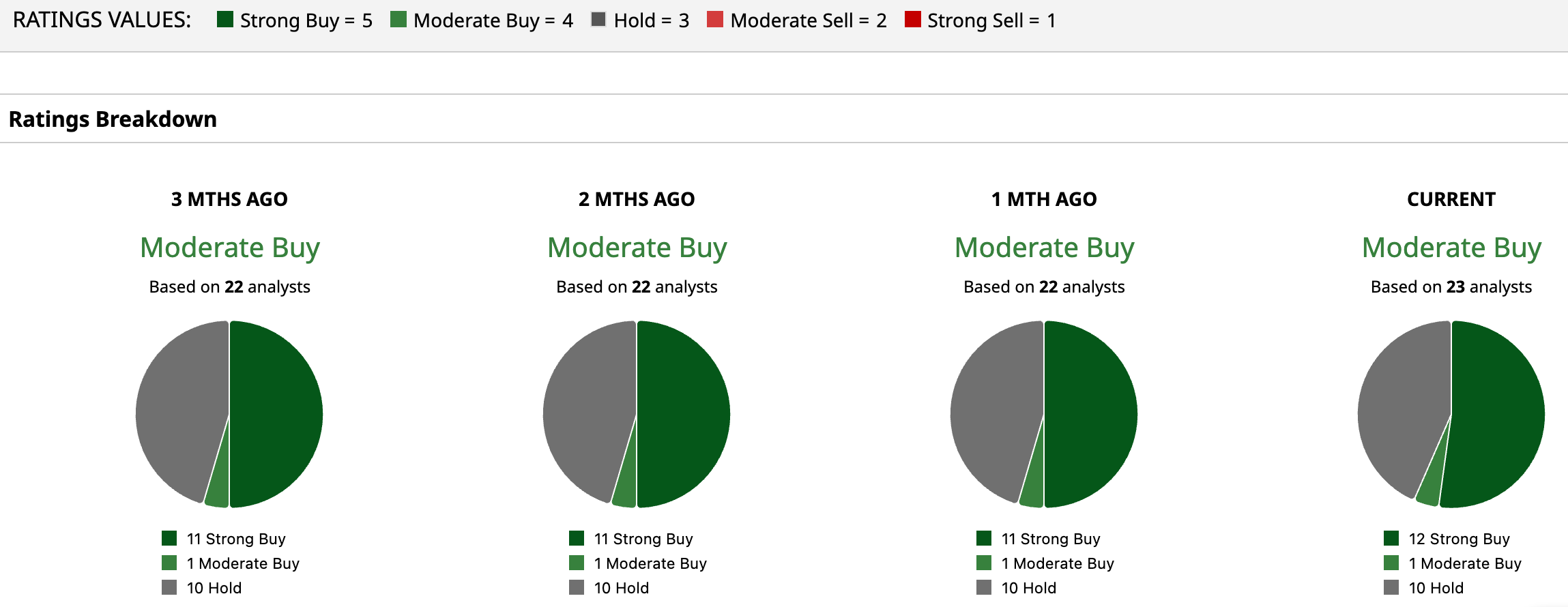

Overall, NOC has a consensus “Moderate Buy” rating. Of the 23 analysts covering the stock, 12 advise a “Strong Buy,” one suggests a “Moderate Buy,” and 10 analysts recommend a “Hold” rating.

The average analyst price target for NOC is $735.14, indicating a potential upside of 28.5%. The Street-high target price of $849 suggests that the stock could rally as much as 48.4%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Down Nearly 50% from All-Time Highs, Should You Buy the dip in POET Technologies Stock?

- ‘I’d Love to Be Able to Save an Airline,’ Says Trump About Spirit. But Is There Any Saving FLYYQ Stock?

- Semiconductor Stocks Are the New Elephant in the Room at 14% of the S&P 500. How to Play This Tech Super-Sector.

- As Alibaba Rolls Out the Happy Horse AI Model, Should You Buy, Sell, or Hold BABA Stock?