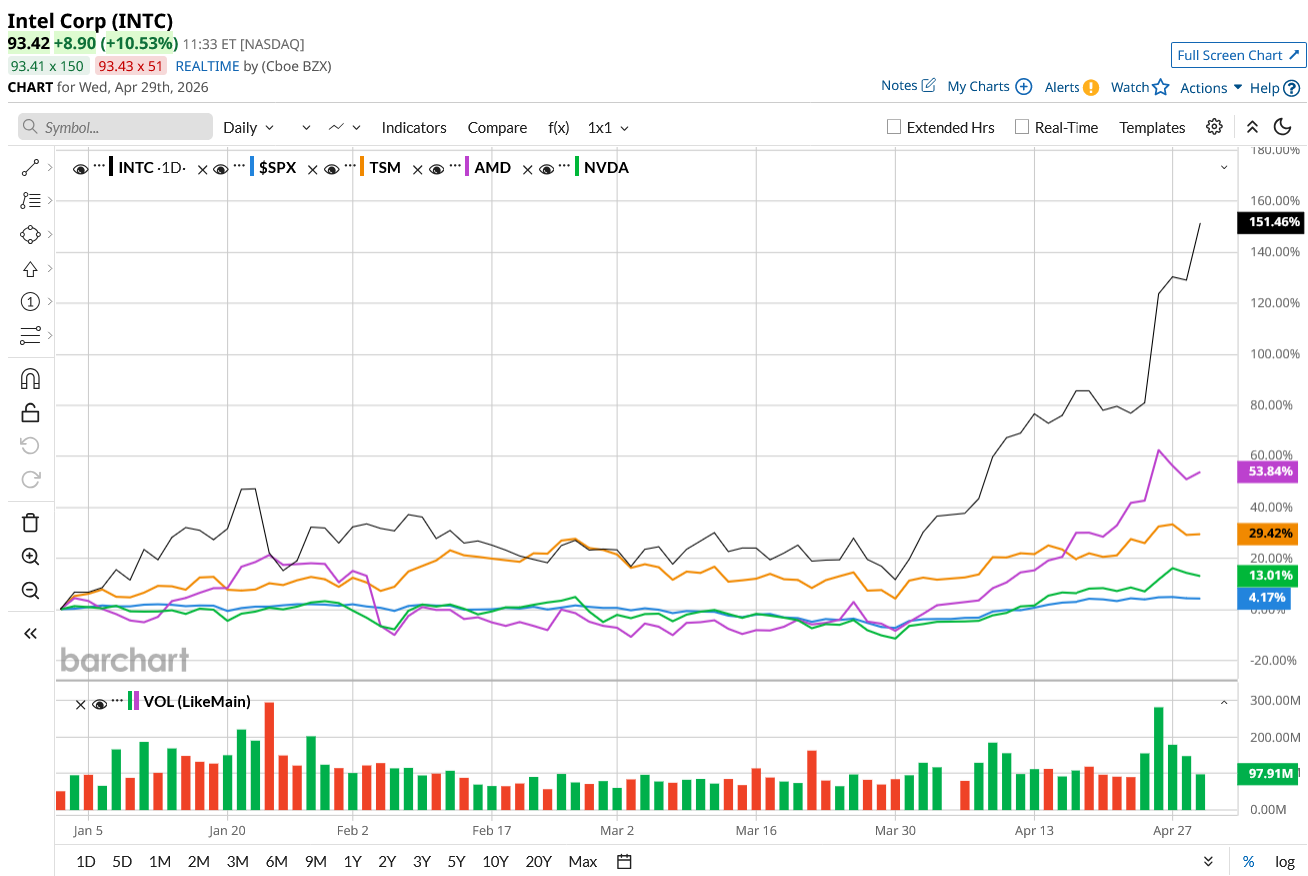

For years, Intel (INTC) lagged the artificial intelligence (AI) boom while competitors like Nvidia (NVDA), AMD (AMD), and TSMC (TSM) stormed ahead, raising doubts about its ability to keep pace in the most critical growth markets. But Intel's stock is suddenly back in the spotlight after testing investors patience for years with its turnaround story. Intel shares have surged 42% in just five days following its Q1 report and are now up an eye-catching 152% year-to-date (YTD), handily outperforming both the broader market and key semiconductor rivals.

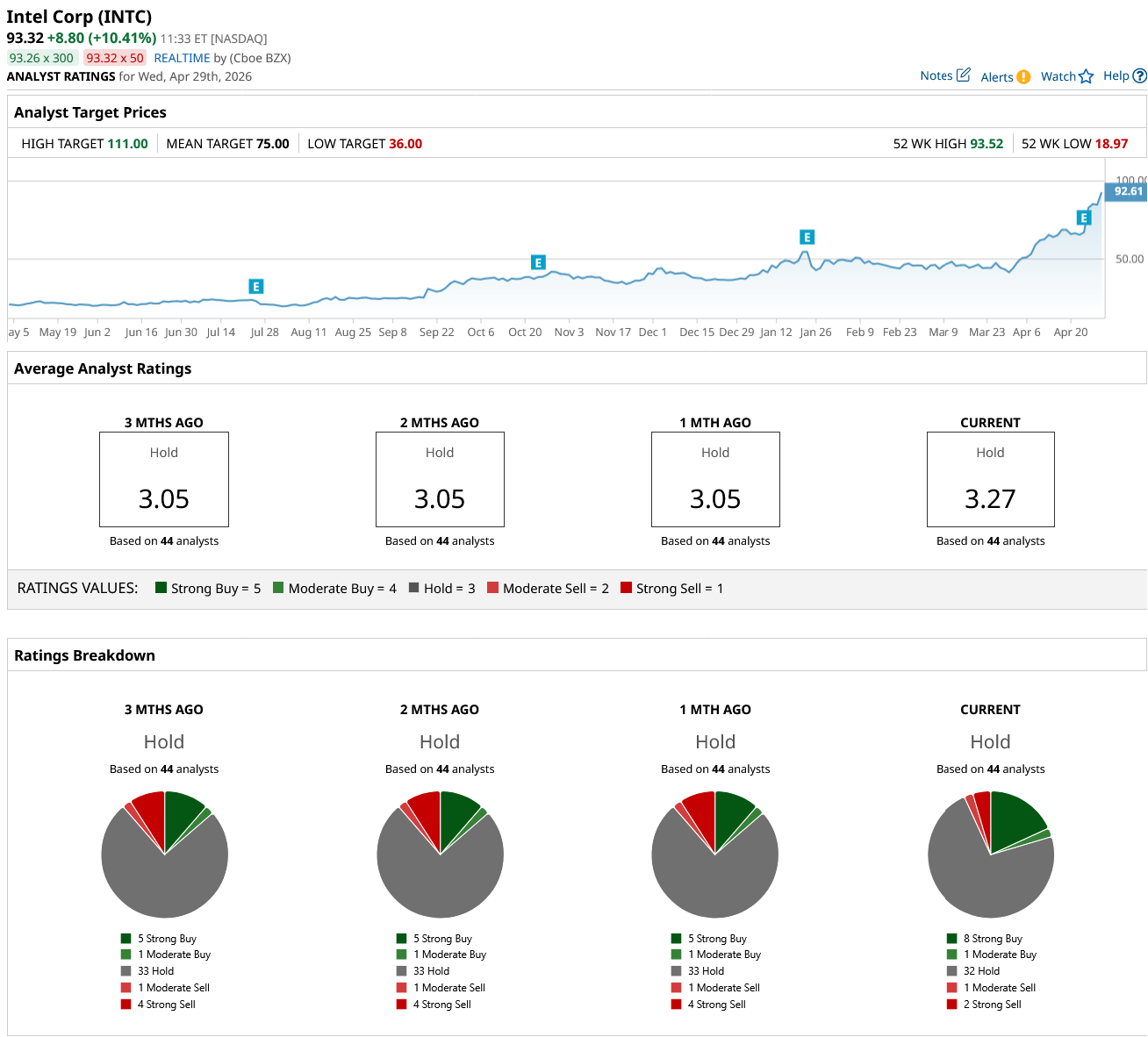

And Evercore ISI analyst Mark Lipacis has raised the target price for Intel sharply to $111 from $45. This high price target suggests the stock has the potential to climb another 19% from current levels. The analyst believes under the leadership of CEO Lip-Bu Tan, Intel is back in a competitive position after years of missteps.

Is it time to grab INTC stock now?

Early Signs of Progress Have Turned Wall Street in Its Favor

Mark Lipacis upgraded INTC stock to “Outperform,” highlighting the possibility that the next wave of AI demand may rely far more on CPUs than previously expected. The analyst also noticed that under the new leadership, Intel has stabilized its balance sheet and is executing a clearer, more disciplined strategy. At the same time, geopolitical tensions and supply chain concerns are elevating Intel’s strategic value, as it remains the only U.S.-based company capable of creating leading-edge chips at scale.

In addition to Evercore, analysts at DBS, Barclays, D.A. Davidson, Morgan Stanley, and Robert W. Baird, among others, also boosted the price target for INTC. Roth Capital increased the price target to $100 from $50 and upgraded the stock to a “Buy” from “Neutral.” The firm is impressed with Intel’s recovery under Lip-Bu Tan.

Overall, the price upgrades reflect Wall Street’s opinion that Intel could be entering a multi-year recovery fueled by AI demand, improved execution, and its unique geopolitical positioning.

A CEO-Driven Turnaround Story

When Intel brought in Lip-Bu Tan as CEO in March 2025, the story was about survival. Tan, on the other hand, has a solid reputation of being a turnaround specialist with deep industry credibility. One year later, the survival story has shifted to a strategic reset.

In the first quarter of fiscal 2026 released on April 23, Intel reported revenue of $13.6 billion, exceeding guidance by $1.4 billion and increasing 7% year-over-year (YoY). Earnings per share landed at $0.29, far above the company’s breakeven guidance. Meanwhile, analysts had expected just $0.01 per share in earnings in the quarter. This marks the sixth consecutive quarter the company has surpassed expectations, a streak that signals improving execution discipline. Yet, Tan pointed out that performance could have been stronger if there wasn’t a demand-supply imbalance across all segments.

For the past few years, GPUs have dominated the AI story. However, Tan highlighted that instead of GPUs doing most of the heavy lifting, future AI workloads may require many more CPUs, potentially reversing the traditional ratio in favor of CPUs. This could dramatically increase the importance of Intel’s core business. Management also noted that Xeon processors, in particular, are seeing strong and sustained demand. Notably, Intel’s Xeon 6 chips built on Intel 3 and its Core Series 3 processors using the 18A node have entered large-scale production, representing the company’s quickest product ramp in the past five years. Evercore called Intel a “CPU renaissance play,” implying that the company’s legacy business could become essential to the next wave of AI infrastructure.

Another intriguing fact is that under Tan's leadership, Intel has placed a greater emphasis on partnerships. Intel has struck many long-term agreements, including collaborations with Google (GOOG) (GOOGL), Nvidia, and SambaNova Systems, to strengthen its position in AI infrastructure. It has also taken a more unconventional path, teaming with SpaceX, Tesla (TSLA), and xAI to study next-generation semiconductor fabrication through the TeraFab program.

But Not Everyone Is Convinced

Despite the growing optimism, there were a few mixed signals. While Bank of America Securities analyst Vivek Arya increased the target price for INTC to $56, he reiterated his “Sell” rating on the stock. The analyst believes that most of Intel’s recovery story already appears reflected in the stock price. Currently, INTC stock trades at a premium of 57x forward 2027 earnings, which are expected to increase by 36.4% over fiscal 2026.

At the same time, Arya states the company continues to face financial pressure, with weak gross margins and ongoing cash burn as it invests heavily in expanding manufacturing capacity, particularly around its advanced 18A node. For context, gross margin stood at 41% in the quarter. Intel’s foundry business is still operating at a loss of $2.4 billion in Q1. It remains one of the most ambitious and risky components of its turnaround story. Furthermore, heavy investments resulted in negative free cash flow of $2 billion in the quarter.

Overall, Wall Street maintains a cautious stance with a consensus “Hold” rating for INTC stock. Of the 44 analysts covering the stock, eight rate it a “Strong Buy,” one recommends a “Moderate Buy,” 32 rate it a “Hold,” one rates it a “Moderate Sell,” and two suggest a “Strong Sell.” The stock has surpassed its average target price of $74.54.

The Bottom Line on INTC Stock

Intel’s rally is driven by a powerful mix of AI optimism, improving execution, and renewed confidence in leadership. Analysts’ price target upgrades show that the company is entering a multi-year recovery, with CPUs potentially playing a bigger role in AI than previously expected.

Intel is far from fully recovered. But Q1 proved the company is moving in the right direction with clarity, purpose, and momentum. Investors with patience and a decade-long investment horizon might want to scoop up INTC stock at a better entry point.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Down Nearly 50% from All-Time Highs, Should You Buy the dip in POET Technologies Stock?

- ‘I’d Love to Be Able to Save an Airline,’ Says Trump About Spirit. But Is There Any Saving FLYYQ Stock?

- Semiconductor Stocks Are the New Elephant in the Room at 14% of the S&P 500. How to Play This Tech Super-Sector.

- As Alibaba Rolls Out the Happy Horse AI Model, Should You Buy, Sell, or Hold BABA Stock?