Geopolitics is once again calling the shots in global markets, and this time, it’s hitting at the heart of the world’s energy lifeline. Rising tensions of the war between the United States and Iran have effectively choked activity through the Strait of Hormuz, the world's most vital artery for global oil and gas flows. With shipments disrupted, investors are bracing for tighter supply, elevated prices, and a fresh wave of volatility rippling across markets. At times like these, history becomes a valuable guide. And analysis from investment firm Schroders highlights an interesting pattern.

In the aftermath of major oil supply disruptions, certain sectors have consistently outperformed. Specifically, energy, consumer staples, healthcare, and utilities have each delivered gains of more than 5% in the 12 months following such shocks. These trends have played out across several major geopolitical events, including the Yom Kippur War in 1973, the Iranian Revolution in 1978, the Iran–Iraq War in 1980, the Gulf War in 1990, and Russia’s War on Ukraine in 2021. The trend underscores a simple dynamic.

When energy supply is constrained and uncertainty rises, investors gravitate toward sectors tied to essential demand and stronger pricing power, areas that tend to remain resilient even as broader economic conditions weaken. With that perspective in mind, the current backdrop is beginning to look familiar. And with history pointing toward a potential rotation into energy-linked names, it may be the right time to take a closer look at these two energy stocks that could benefit from the current setup.

Energy Stock #1: Targa Resources

Texas-based Targa Resources (TRGP) operates at the center of the midstream energy network, making it one of the largest independent infrastructure players in North America. The company’s portfolio spans gathering, processing, and transportation assets that help move natural gas and natural gas liquids (NGLs) from production sites to end markets. This network supports the steady and efficient flow of energy across the U.S. while also linking supply to rising global demand.

As cleaner fuels and related feedstocks gain traction, Targa’s infrastructure continues to serve as a key conduit between upstream production and downstream consumption. With a market capitalization of around $51.8 billion, Targa has been a clear beneficiary of the current geopolitical backdrop, as rising oil prices lift sentiment across the energy space.

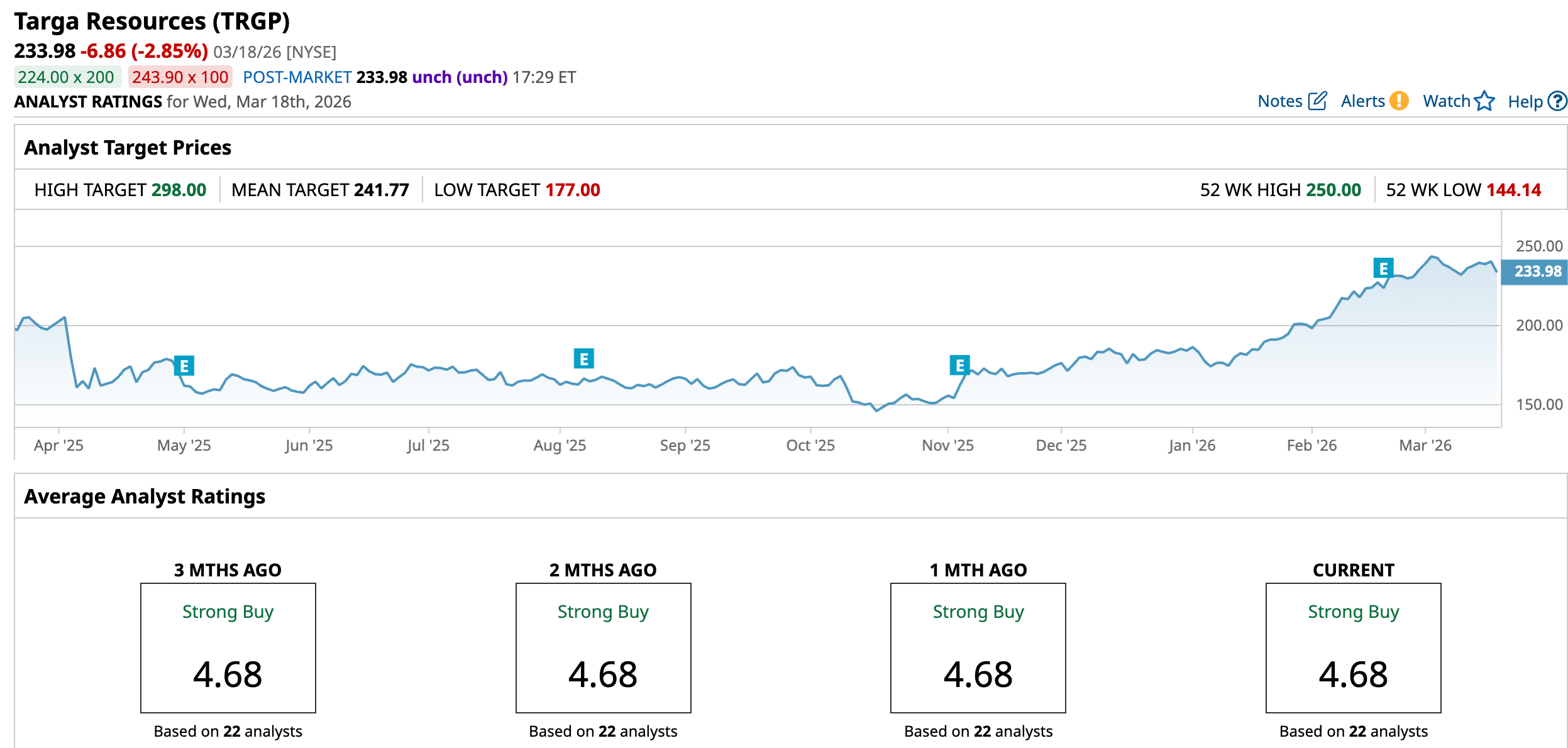

The stock has surged an impressive 26.8% in 2026 so far, sharply outperforming the broader S&P 500 Index ($SPX), which has slipped 3.23% year-to-date (YTD), highlighting just how strongly investors are rotating into energy names amid the ongoing turmoil.

Targa’s fiscal 2025 fourth-quarter results, published on Feb. 19, painted a somewhat mixed picture, but with several standout positives beneath the surface. Total revenue came in at $4.06 billion, marking an 8% year-over-year (YOY) decline, yet still topping Wall Street’s expectations of $3.90 billion. Profitability, however, told a stronger story.

Net income attributable to Targa jumped to $545 million from $351 million a year ago, while the company delivered record adjusted EBITDA of $1.34 billion, up 20% annually and 5% sequentially from Q3 2025. The real highlight was the surge in volumes across Targa’s integrated network, particularly in the Permian Basin. Natural gas inlet volumes in the region hit a record 6.65 billion cubic feet per day, reflecting 10% YOY growth.

This momentum was supported by the successful launch of the Bull Moose II processing plant in October 2025. At the same time, the Logistics and Transportation (L&T) segment posted record NGL pipeline transportation and fractionation volumes. This helped to offset softer margins in the Gathering and Processing (G&P) segment, which were pressured by weak natural gas prices at the Waha hub.

Also, Targa used its fourth-quarter update to signal a notable shift in its capital return strategy heading into 2026. After repurchasing $642 million worth of shares in 2025, the company declared a $1.25 per share dividend for Q4 and unveiled plans to boost its annual dividend by 25% to $5.00 per share starting May 2026. This move is underpinned by a business mix that is now over 90% fee-based, providing greater stability to cash flows regardless of swings in oil and gas prices.

Looking ahead, management struck an optimistic tone. Targa expects adjusted EBITDA to land between $5.4 billion and $5.6 billion in 2026, implying an 11% increase at the midpoint. To support this growth, the company is gearing up for a heavy investment cycle, with approximately $4.5 billion earmarked for capital expenditures aimed at expanding its infrastructure footprint.

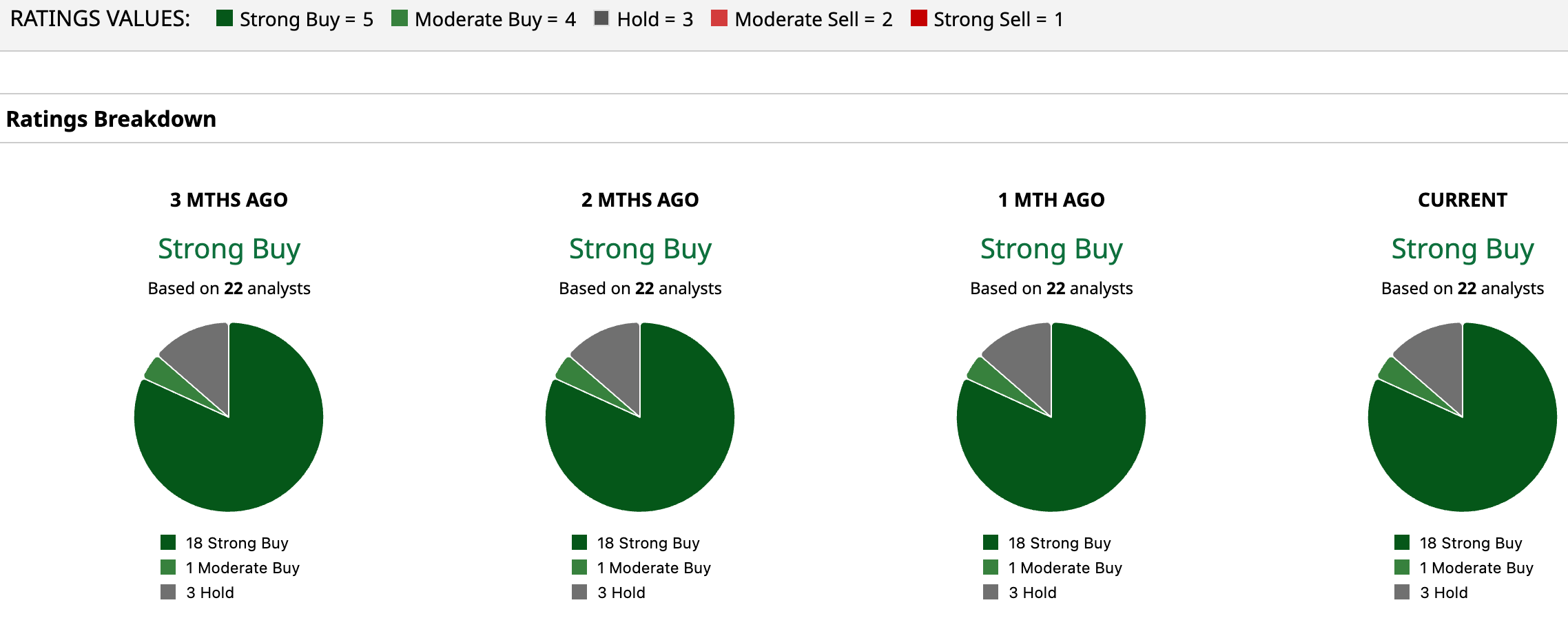

Overall, Wall Street remains highly optimistic about Targa, with the stock carrying a consensus “Strong Buy” rating. Of the 22 analysts covering the stock, 18 recommend “Strong Buy,” one suggests “Moderate Buy,” while three maintain a “Hold.” The average price target of $241.77 points to 3.3% upside from current levels, but the Street-high target of $298 implies the stock could still rally by as much as 27.4%, highlighting lingering bullish conviction.

Energy Stock #2: Expand Energy

Valued at roughly $25.6 billion by market capitalization, Expand Energy Corporation (EXE) is the largest natural gas producer in North America, with operations built around supplying gas to both domestic and international markets. The company focuses on linking its large-scale production base with areas of growing demand, reflecting the increasing role of natural gas in the global energy mix.

Its strategy is centered on generating consistent returns by utilizing a diversified asset portfolio, maintaining financial discipline, and driving operational efficiency. As natural gas continues to be viewed as a relatively lower-carbon and reliable energy source, Expand Energy remains positioned within a segment of the market that is seeing steady long-term demand.

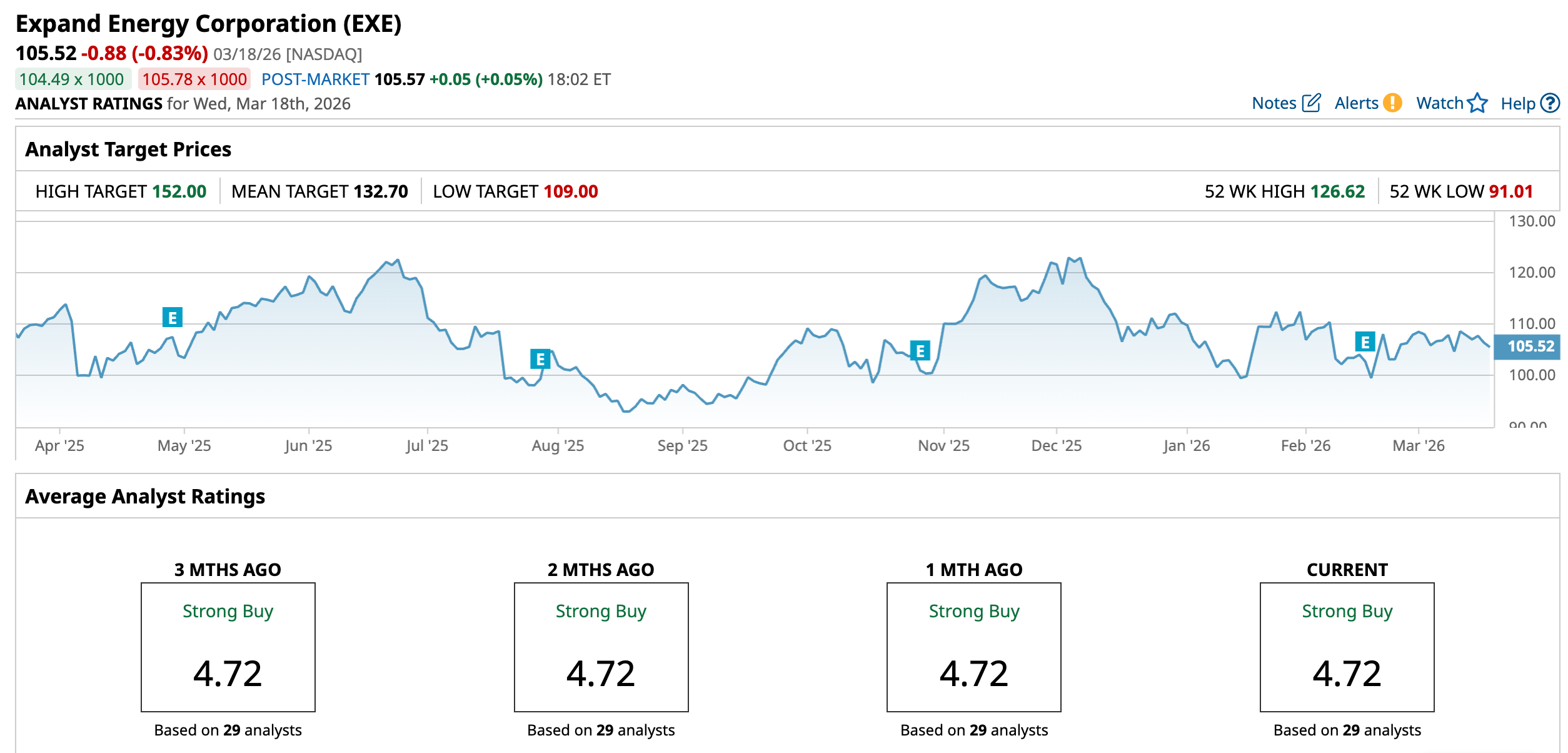

Unlike Targa’s strong run to new highs in 2026, Expand Energy has faced a more challenging start to the year. The company’s heavy exposure to natural gas has weighed on performance, especially as oversupply concerns for 2027 continue to pressure sentiment. As a result, the stock is down about 4.39% so far this year, underperforming the broader S&P 500 Index, which has seen a comparatively milder decline of 3.23% over the same period.

Despite a volatile start to the year, Expand Energy’s latest results suggest the underlying business remains on a solid footing. The company’s fiscal 2025 fourth-quarter results, released on Feb. 17, delivered a notable earnings beat despite a challenging natural gas pricing environment. Quarterly revenue came in at $3.27 billion, marking a sharp 63.5% YOY increase and comfortably topping the $2.25 billion forecast. On an adjusted basis, EPS surged to $2.00, up a stunning 263.6% from the prior year and ahead of estimates of $1.89 per share.

Profitability remained a key highlight. Adjusted EBITDAX reached $1.425 billion for the quarter, underscoring the company’s strong cash-generating capacity as the largest natural gas producer in the U.S. Operationally, Expand Energy delivered record production of 7.40 billion cubic feet equivalent per day (Bcfe/d), up 15% YOY, with output still heavily weighted toward natural gas at 92%.

Another standout was the company’s progress on merger synergies. Management highlighted a 15% reduction in breakeven costs in the Haynesville Basin while still achieving double-digit production growth. As Interim President and CEO Mike Wichterich noted, the improvement reflects the company’s scale, financial strength, and capital efficiency, positioning it well to capture demand across power, industrial, and LNG markets.

At the same time, the fourth-quarter update signaled a shift in strategy heading into 2026, one that drew mixed reactions, particularly from growth-focused investors. Expand Energy declared a quarterly base dividend of $0.575 per share, payable in March 2026, but emphasized a more disciplined, balance sheet-focused approach.

The company plans to reduce gross debt by at least $1 billion in 2026, building on the $1.25 billion already paid down since the merger. This balance sheet first strategy is aimed at maintaining resilience, especially if natural gas prices remain under pressure. Looking ahead, management offered a steady outlook for 2026, projecting average production of 7.5 Bcfe/d alongside a capital budget of approximately $2.85 billion.

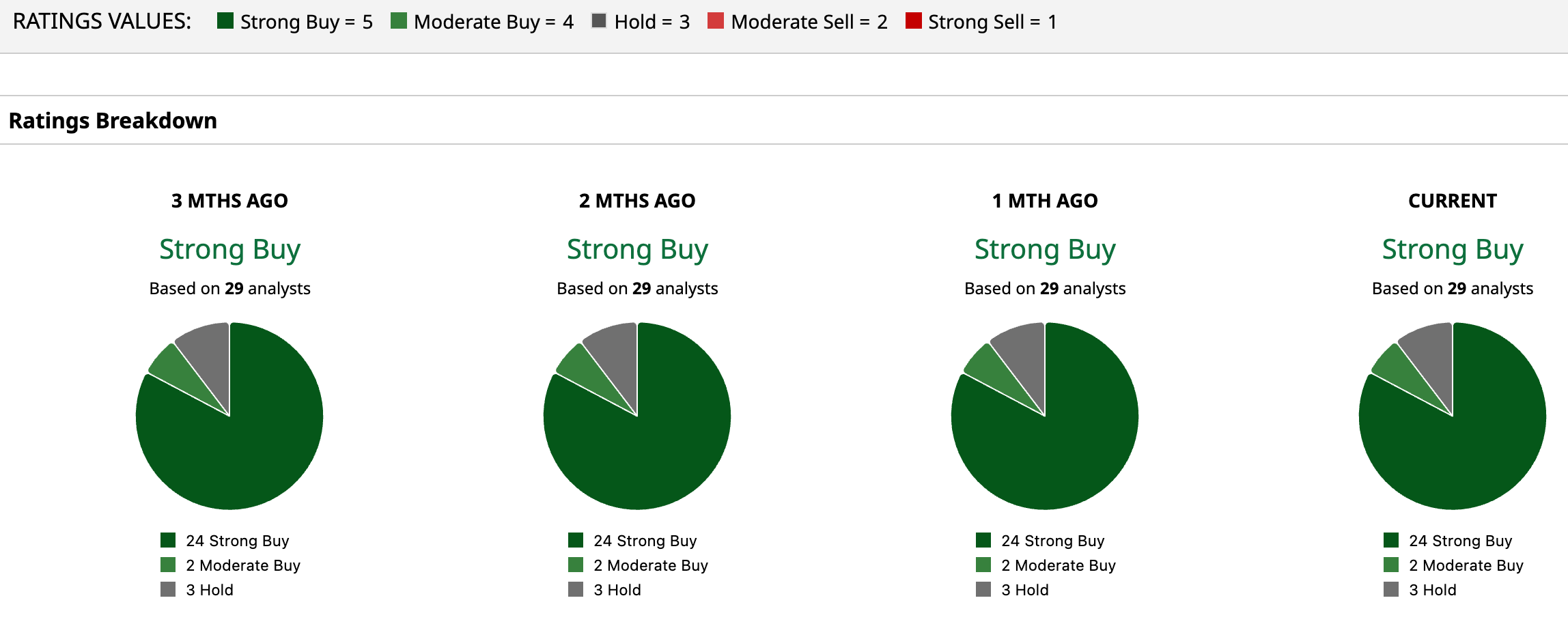

Overall, Wall Street continues to show strong confidence in Expand Energy, with the stock holding a consensus “Strong Buy” rating. Among the 29 analysts covering it, 24 have issued a “Strong Buy,” two recommend a “Moderate Buy,” and three remain on a “Hold.” The average price target of $132.70 suggests a 25.76% upside from current levels, while the Street-high target of $152 implies the stock could rally up to 44% from here.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart