The stock market can be quite turbulent. Growth stocks, while having tremendous potential, can also be risky, as we have seen this month. The once-hyped AI growth stocks plummeted as investors failed to see adequate growth in comparison to their enormous capital expenditures. In such volatile scenarios, dividend stocks turn out to be a reliable source of income. When it comes to dependable income, few names carry the weight of Pfizer (PFE). After a rocky few years highlighted by post-pandemic revenue stabilization and pipeline shifts, PFE stock now offers something income investors rarely ignore: a dividend yield above 6%.

But yield isn’t the only factor to consider when choosing a dividend stock. Let’s find out if Pfizer is a high-quality dividend opportunity.

A 6%+ Yield That Demands Attention, But There’s More to It

Valued at $154.3 billion, Pfizer is a global pharmaceutical company that develops, manufactures, and sells prescription drugs for cancer, heart disease, inflammation, and rare diseases. It also makes vaccines for infectious diseases. So far this year, Pfizer’s stock has surged 7.7%, beating the overall market.

Currently, Pfizer pays a forward dividend yield of 6.45%, significantly higher than the S&P 500 ($SPX) average and the healthcare average of 1.6%. This high yield can boost total returns, especially when reinvested. However, yield is not everything you consider when you are choosing dividend stocks. A reliable dividend stock should be able to pay and increase dividends consistently. Pfizer has been paying and hiking dividends for the past 15 years.

The second factor to consider is the dividend payout ratio, which measures how much of a company’s earnings is distributed as dividends. A higher ratio makes you question whether the dividends are sustainable unless earnings grow at a consistent rate. It also suggests the company is not retaining enough to invest in growth opportunities. However, Pfizer’s forward payout ratio of 53.2% suggests dividends are sustainable, with room for growth.

A Deep Drug Pipeline to Sustain the Dividends

While Pfizer became widely recognized for its Covid-19 vaccine, its core business is long-term drug development across multiple areas. In 2025, Pfizer reported total revenue of $62.6 billion, a 2% operational decrease year-over-year (YoY), owing primarily to declining Covid product sales. However, excluding Covid-related items, operational revenue increased 6%, indicating that the company’s core business has stabilized and returned to growth. Adjusted diluted earnings per share reached $3.22 for the full year, up from $3.11 in the prior year.

Adjusted gross margin stood at 76% for the year. The most notable contributions were from recently launched and acquired portfolio products. These products, which included ABRYSVO (vaccine for RSV), ELIQUIS (blood thinner), Prevnar (a pneumococcal vaccine), and the Vyndaqel family that treats transthyretin amyloidosis (ATTR), generated $10.2 billion in revenue, increasing 14% YoY. This growth is essential to mitigate the upcoming loss-of-exclusivity (LOE) headwinds between 2026 and 2028. Pfizer's push into obesity, a market that management believes could reach $150 billion, could be another huge long-term opportunity. The company is evaluating its ultra-long-acting GLP-1 receptor agonist candidate, known as PF'3944, in Phase 2 trials. Pfizer is planning 10 Phase 3 studies of PF'3944, targeting potential approvals by 2028. If successful, this franchise could materially reshape Pfizer’s revenue base in the next decade.

While investing heavily in R&D and acquisitions, Pfizer is maintaining aggressive cost discipline and is on track to deliver the majority of $7.2 billion in total net cost savings by the end of 2026. In 2025, Pfizer paid out $9.8 billion in dividends while investing $10.4 billion in internal R&D. The company also spent $8.8 billion on business development. Furthermore, management emphasized the company's commitment to maintaining and growing dividends over time, even while it reinvests strategically.

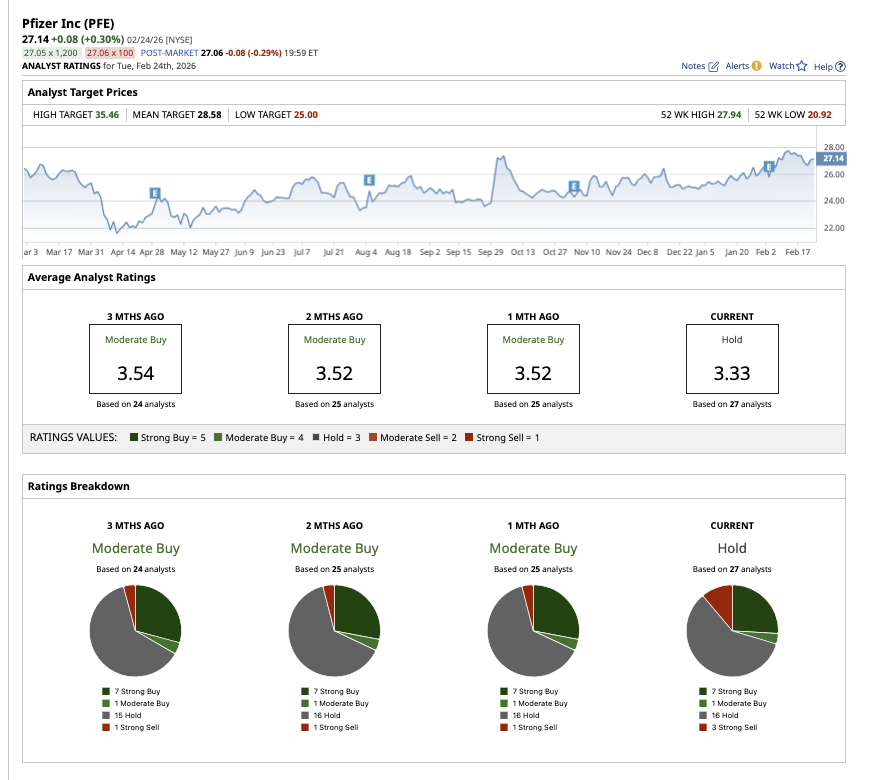

What Does Wall Street Say About PFE Stock?

Wall Street believes PFE stock is a “Moderate Buy.” Out of the 27 analysts who cover PFE, seven rate it a “Strong Buy,” one rates it a “Moderate Buy,” 16 rate it a “Hold,” and three suggest a “Strong Sell.” PFE stock is trading close to its average price target of $28.58. However, its high target price of $35.46 implies upside potential of 31% over the next 12 months.

While in transition, Pfizer has maintained core growth, increased margins through extreme cost discipline, has a strong late-stage pipeline, and has committed to a $9.8 billion annual dividend. Management expects growth to accelerate near the end of the decade, owing to obesity and oncology products, along with recently acquired businesses. Growth investors may find their patience rewarded in the coming years. Income investors will continue to benefit from the high yield and the reliable payouts.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart