Over the past six months, Hartford’s shares (currently trading at $127.05) have posted a disappointing 6.2% loss, well below the S&P 500’s 10.9% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Hartford, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Hartford Not Exciting?

Even though the stock has become cheaper, we don’t have much confidence in Hartford. Here are three reasons you should be careful with HIG, plus one stock we’d rather own.

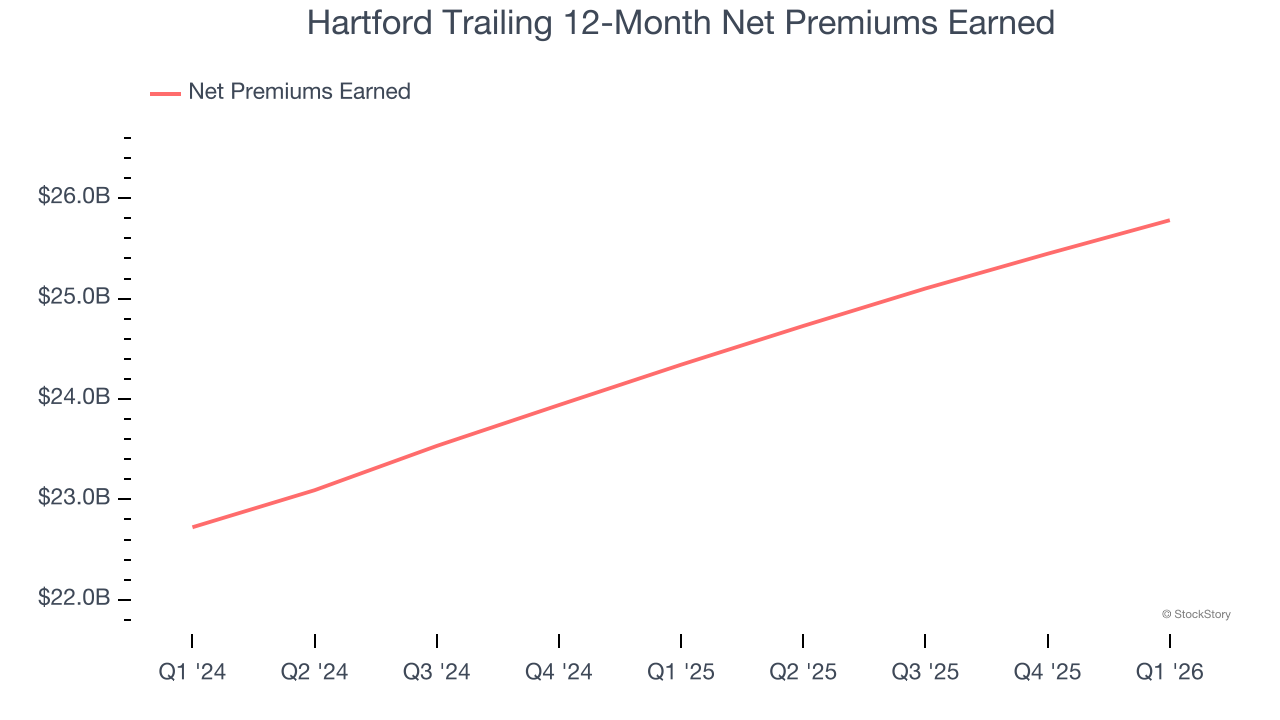

1. Net Premiums Earned Point to Soft Demand

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Hartford’s net premiums earned has grown at a 6.5% annualized rate over the last two years, slightly worse than the broader insurance industry and in line with its total revenue.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Hartford’s revenue to drop by 27.1%, a decrease from its 7.2% annualized growth for the past two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

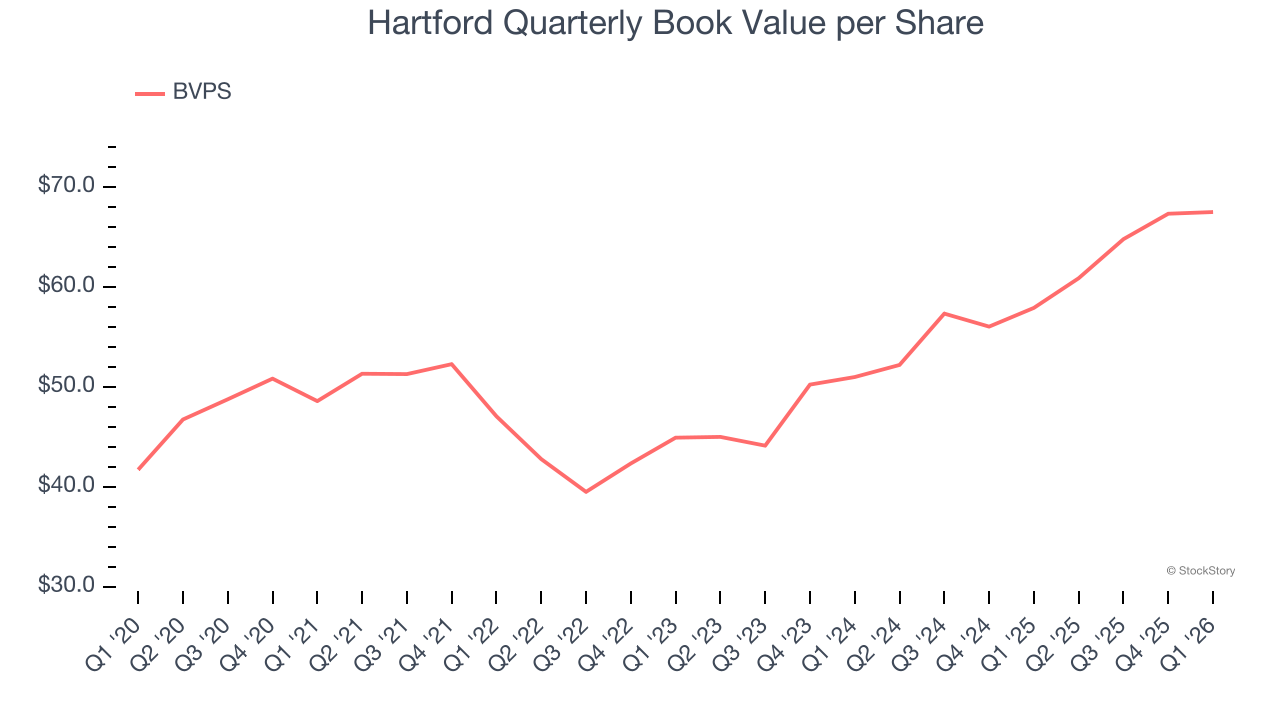

3. Steady Increase in BVPS Highlights Solid Asset Growth

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

Although Hartford’s BVPS increased by a meager 6.8% annually over the last five years, the good news is that its growth has recently accelerated as BVPS grew at a solid 15.1% annual clip over the past two years (from $50.99 to $67.50 per share).

Final Judgment

Hartford isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 1.8× forward P/B (or $127.05 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.