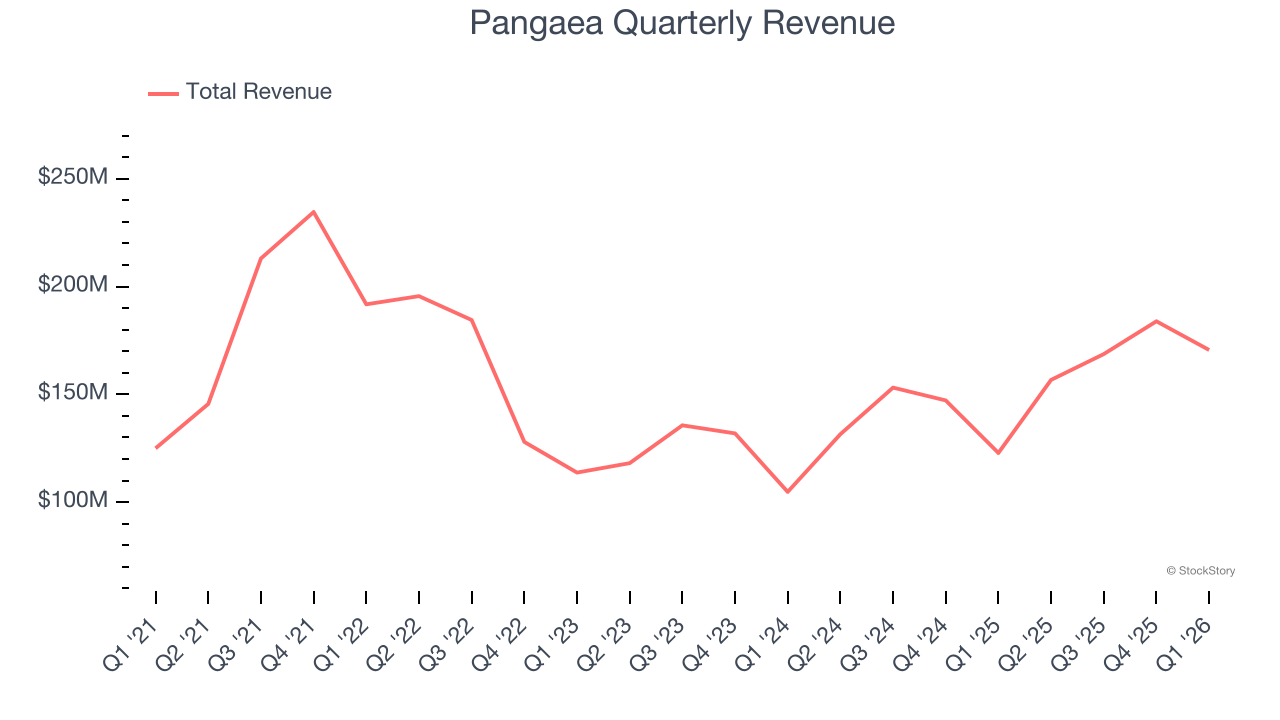

Pangaea Logistics (NASDAQ: PANL) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 38.9% year on year to $170.6 million. Its non-GAAP profit of $0.11 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Pangaea? Find out by accessing our full research report, it’s free.

Pangaea (PANL) Q1 CY2026 Highlights:

- Revenue: $170.6 million vs analyst estimates of $165.8 million (38.9% year-on-year growth, 2.9% beat)

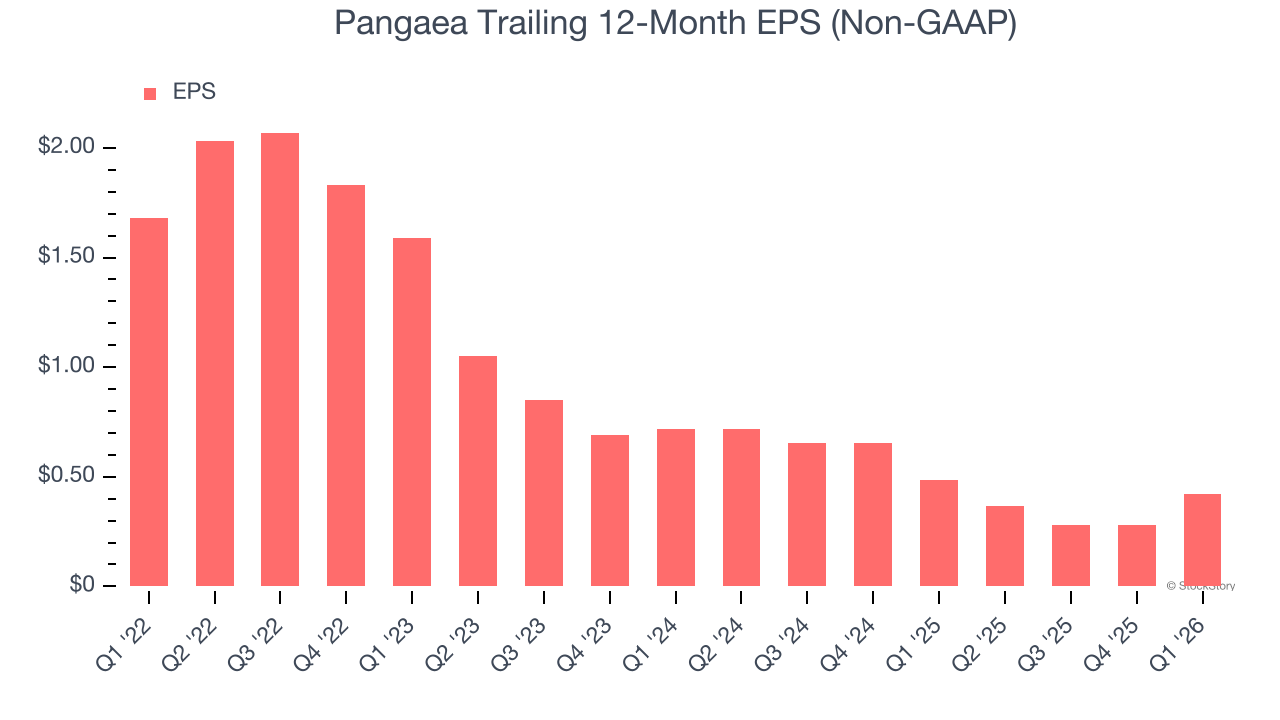

- Adjusted EPS: $0.11 vs analyst estimates of $0.05 (significant beat)

- Adjusted EBITDA: $25.2 million vs analyst estimates of $19.86 million (14.8% margin, 26.9% beat)

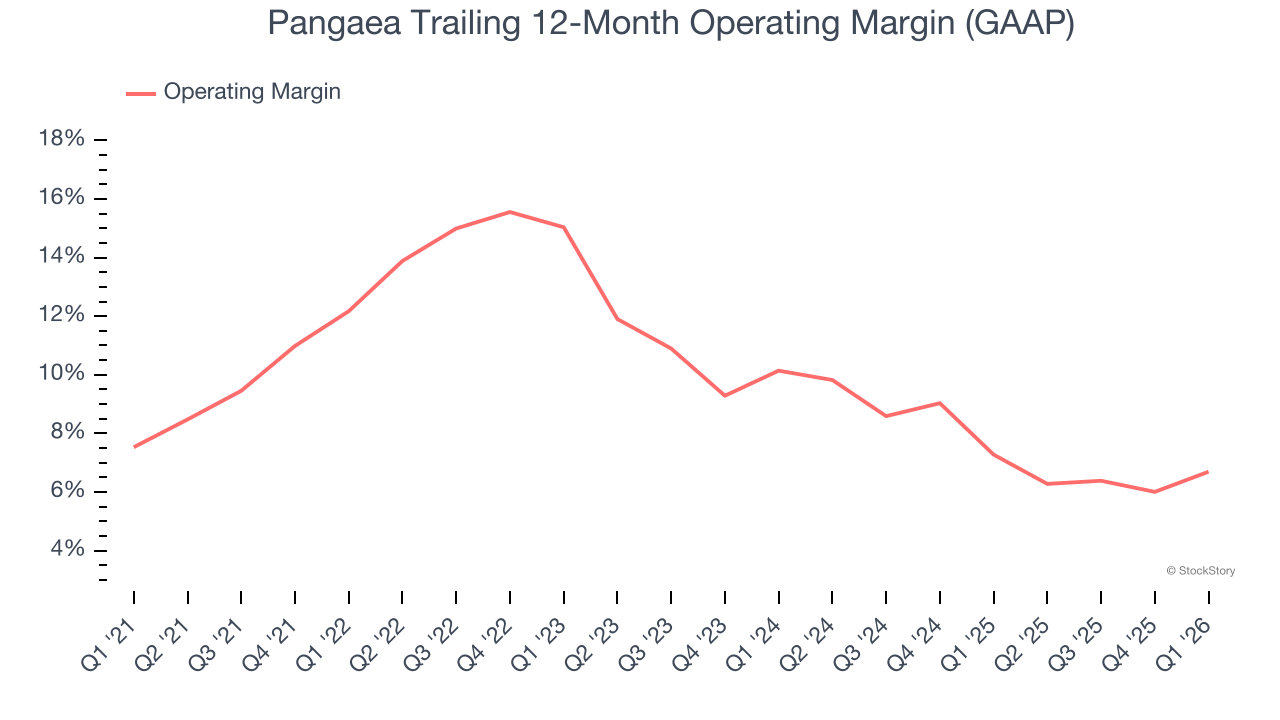

- Operating Margin: 6.1%, up from 2.4% in the same quarter last year

- Free Cash Flow was $2,683, up from -$4.82 million in the same quarter last year

- Market Capitalization: $512.1 million

"Our first quarter results represent a solid start to 2026, reflecting continued strong operating execution, and supportive market conditions" said Mads Boye Petersen, President and Chief Executive Officer of Pangaea Logistics Solutions.

Company Overview

Established in 1996, Pangaea Logistics (NASDAQ: PANL) specializes in global logistics and transportation services, focusing on the shipment of dry bulk cargoes.

Revenue Growth

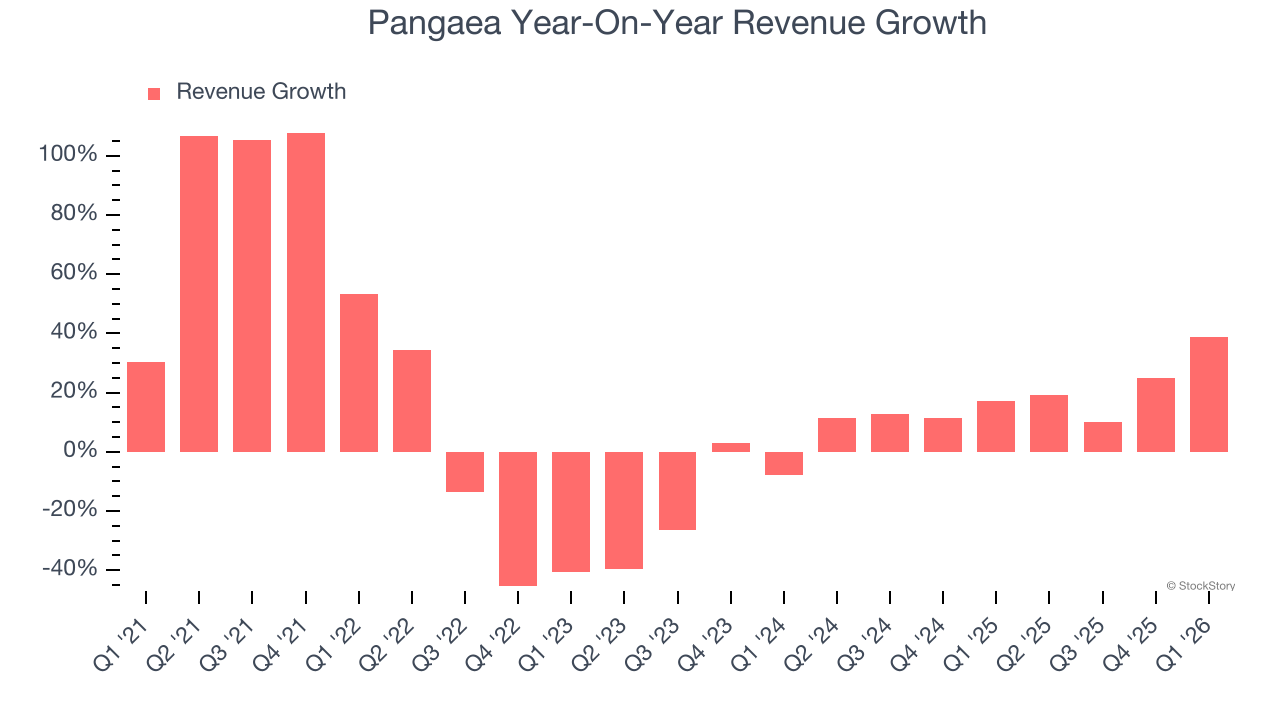

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Pangaea’s 10.5% annualized revenue growth over the last five years was impressive. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Pangaea’s annualized revenue growth of 17.7% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Pangaea reported wonderful year-on-year revenue growth of 38.9%, and its $170.6 million of revenue exceeded Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 15.8% over the next 12 months, a slight deceleration versus the last two years. Still, this projection is admirable and indicates the market is baking in success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Pangaea has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.4%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Pangaea’s operating margin decreased by 5.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Pangaea generated an operating margin profit margin of 6.1%, up 3.8 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Pangaea’s full-year EPS dropped 179%, or 29.3% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Pangaea’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Pangaea, its EPS declined by 23.6% annually over the last two years while its revenue grew by 17.7%. This tells us the company became less profitable on a per-share basis as it expanded.

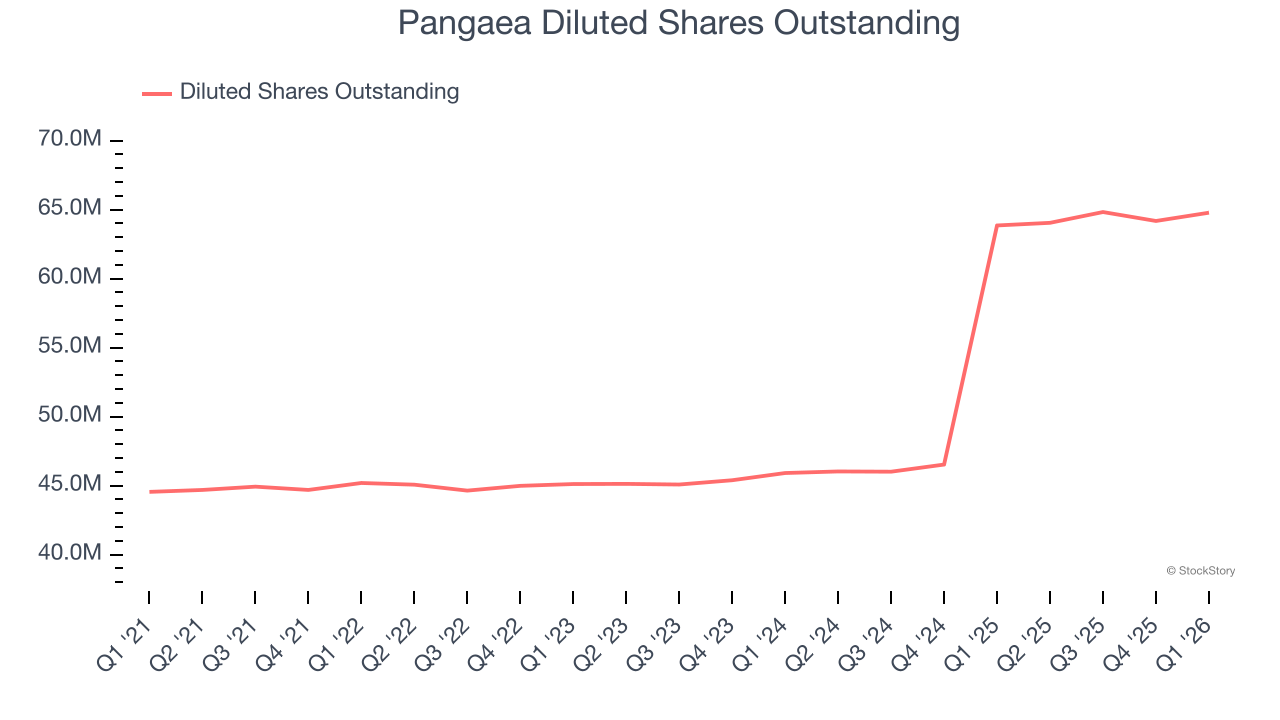

We can take a deeper look into Pangaea’s earnings to better understand the drivers of its performance. We mentioned earlier that Pangaea’s operating margin expanded this quarter, but a two-year view shows its margin has declinedwhile its share count has grown 41.1%. This means the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Pangaea reported adjusted EPS of $0.11, up from negative $0.03 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Pangaea’s Q1 Results

It was good to see Pangaea beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 3.4% to $7.93 immediately following the results.

Indeed, Pangaea had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).