Since March 2021, the S&P 500 has delivered a total return of 66.7%. But one standout stock has more than doubled the market - over the past five years, Laureate Education has surged 139% to $33.96 per share. Its momentum hasn’t stopped as it’s also gained 14.3% in the last six months thanks to its solid quarterly results, beating the S&P by 13.8%.

Is now the time to buy Laureate Education, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Laureate Education Will Underperform?

Despite the momentum, we're sitting this one out for now. Here are three reasons we avoid LAUR and a stock we'd rather own.

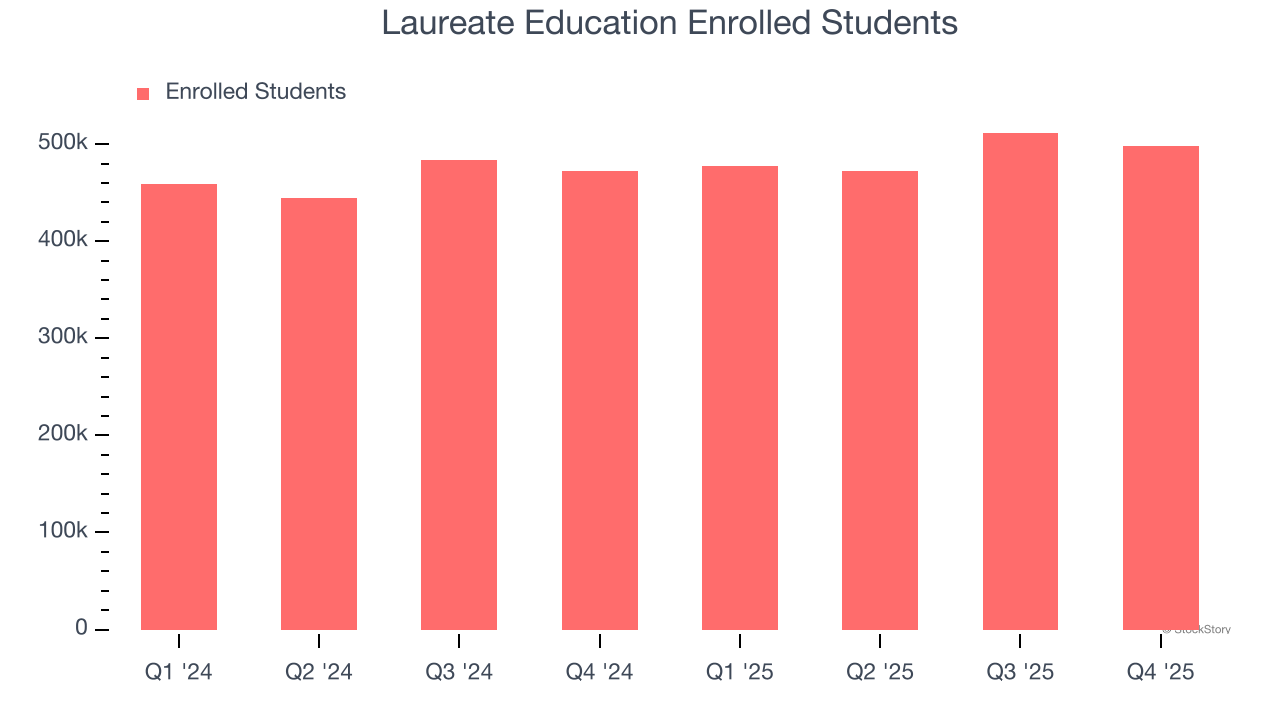

1. Weak Growth in Enrolled Students Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Laureate Education, our preferred volume metric is enrolled students). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Laureate Education’s enrolled students came in at 497,700 in the latest quarter, and over the last two years, averaged 5.3% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

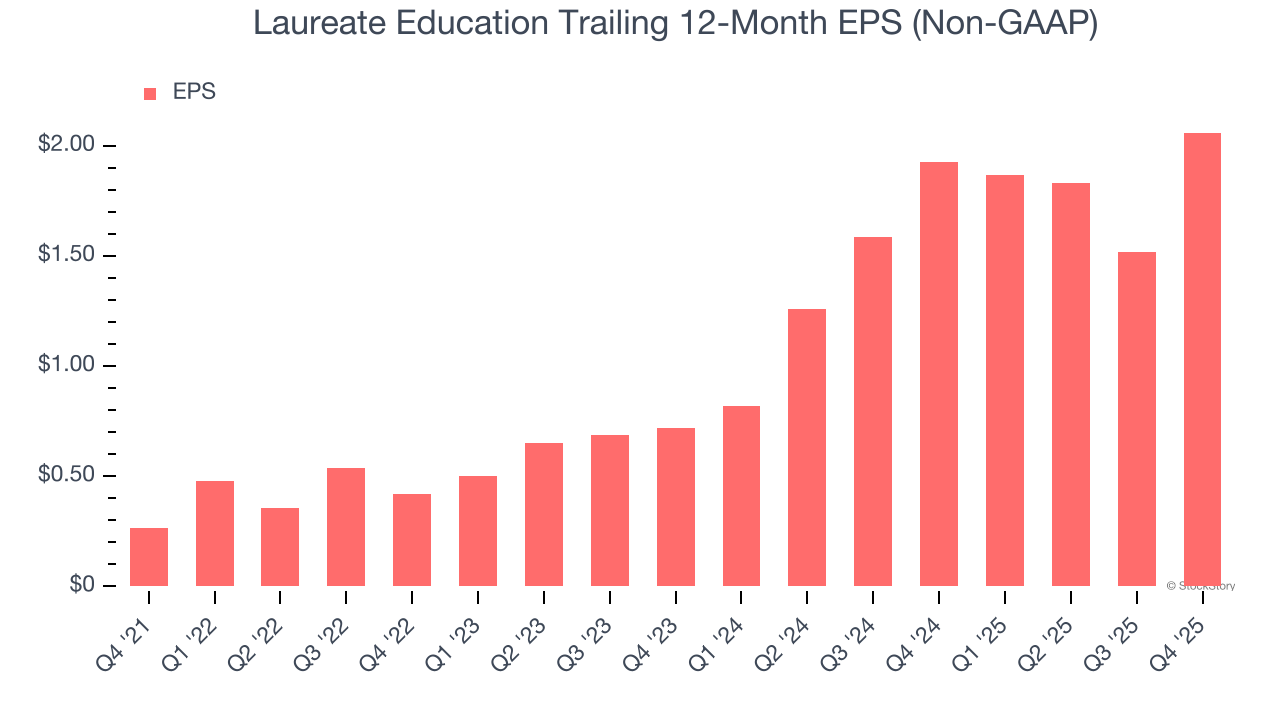

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Laureate Education, its EPS declined by 14% annually over the last five years while its revenue grew by 10.7%. This tells us the company became less profitable on a per-share basis as it expanded.

3. Free Cash Flow Projections Disappoint

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts’ consensus estimates show they’re expecting Laureate Education’s free cash flow margin of 15.5% for the last 12 months to remain the same.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Laureate Education, we’ll be cheering from the sidelines. With its shares topping the market in recent months, the stock trades at 16.2× forward P/E (or $33.96 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are more exciting stocks to buy at the moment. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Laureate Education

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.