Although the S&P 500 is down 4.7% over the past six months, EnerSys’s stock price has fallen further to $90.71, losing shareholders 11% of their capital. This may have investors wondering how to approach the situation.

Is there a buying opportunity in EnerSys, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is EnerSys Not Exciting?

Despite the more favorable entry price, we're cautious about EnerSys. Here are three reasons why there are better opportunities than ENS and a stock we'd rather own.

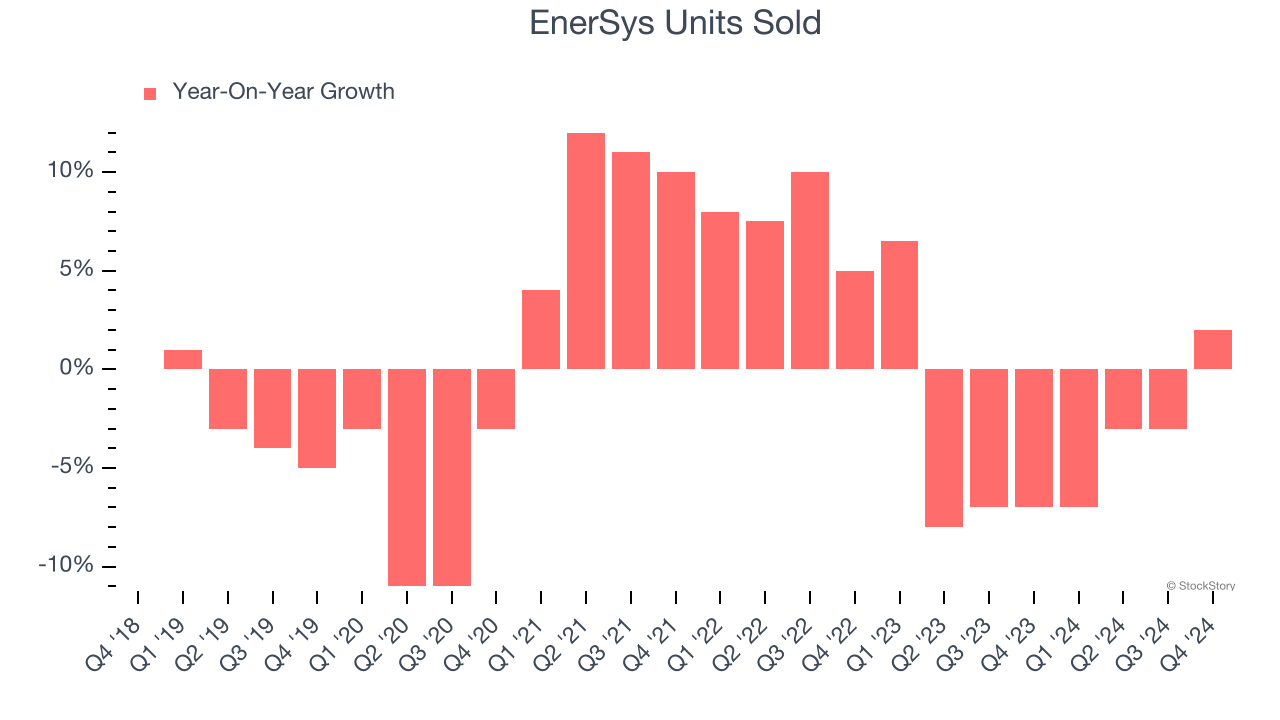

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Renewable Energy company because there’s a ceiling to what customers will pay.

Over the last two years, EnerSys’s units sold averaged 3.3% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests EnerSys might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

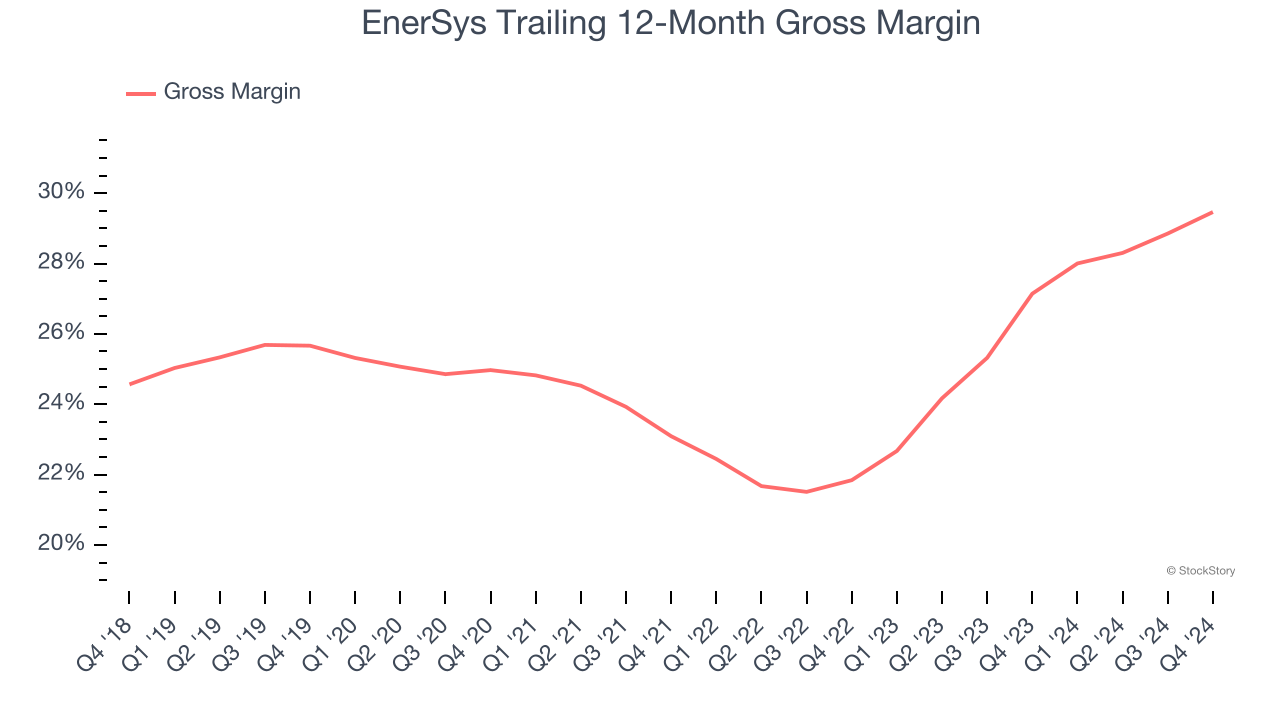

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

EnerSys has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 25.3% gross margin over the last five years. That means EnerSys paid its suppliers a lot of money ($74.65 for every $100 in revenue) to run its business.

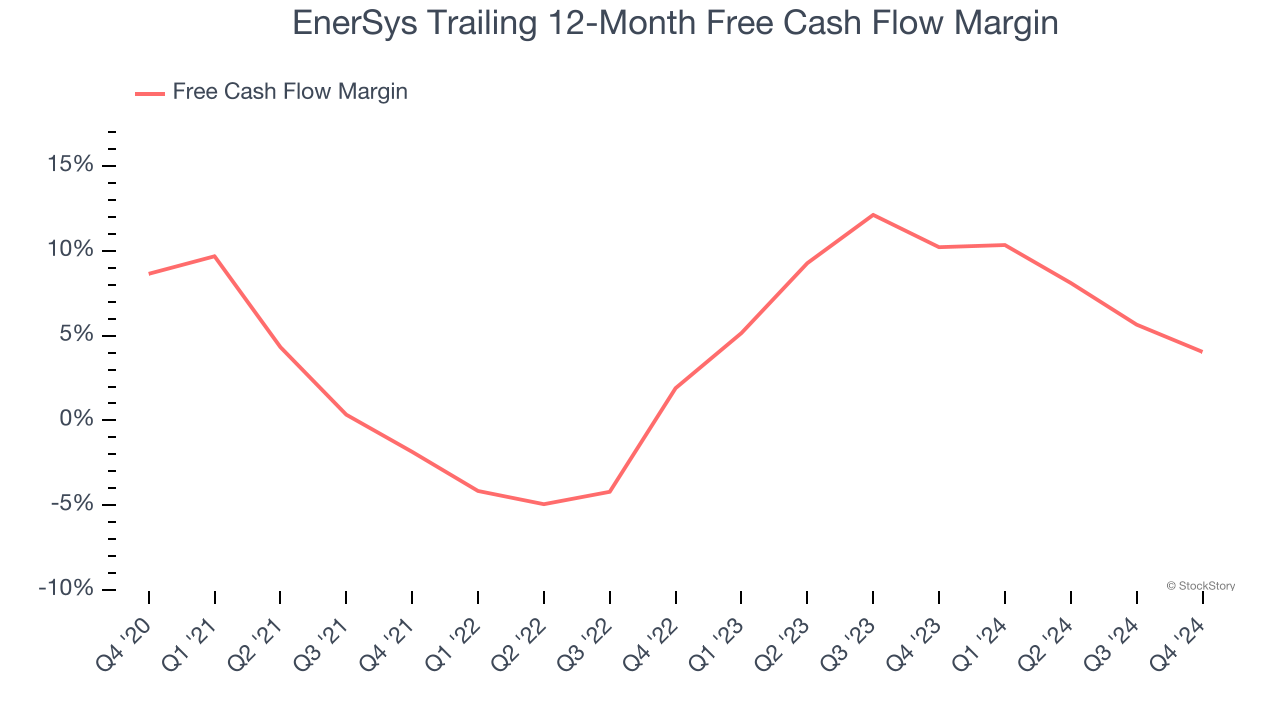

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, EnerSys’s margin dropped by 4.6 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business. EnerSys’s free cash flow margin for the trailing 12 months was 4%.

Final Judgment

EnerSys isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 9.5× forward P/E (or $90.71 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than EnerSys

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today.