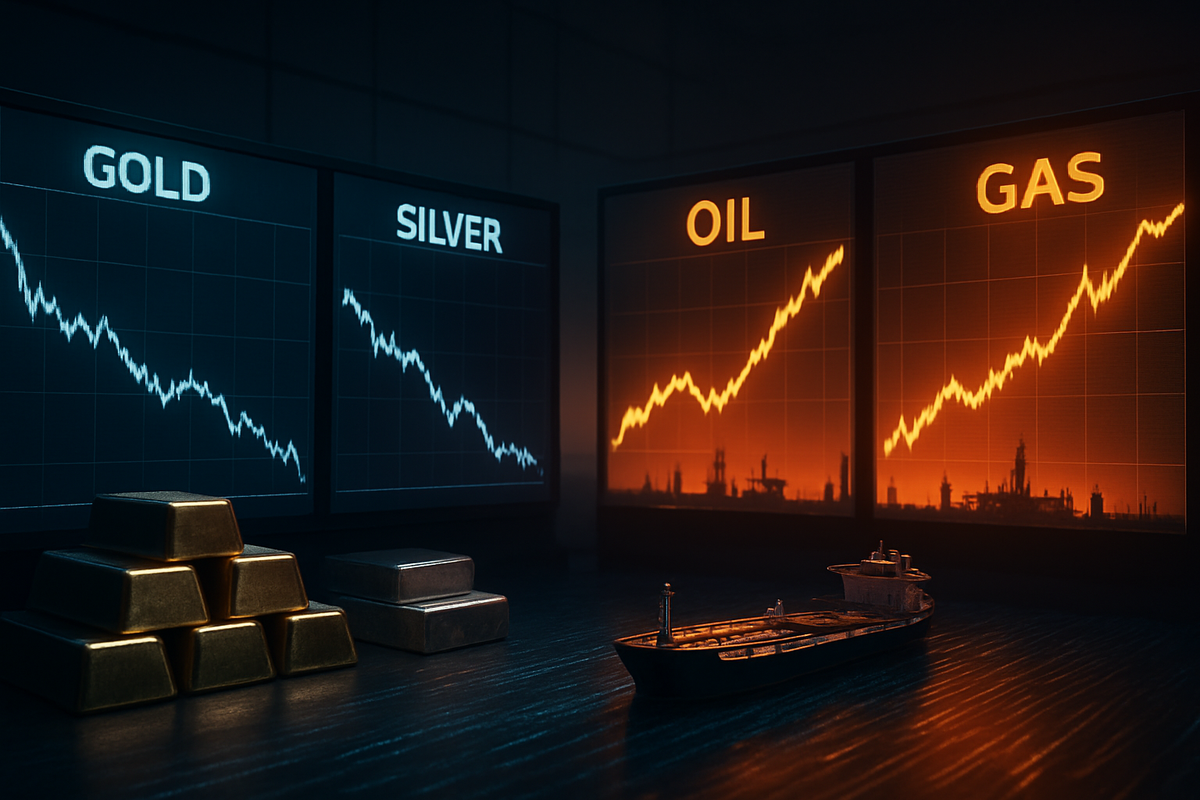

As of April 1, 2026, the financial world is grappling with a radical "regime change" that has shattered the long-held expectations of a 2026 monetary easing cycle. In a dramatic series of moves during the final week of March, the U.S. Federal Reserve and the Bank of Japan (TYO:8301) have doubled down on their hawkish stances, maintaining high interest rates and signaling a readiness to hike further if necessary. This policy pivot, fueled by an explosive energy crisis in the Middle East, has effectively quashed the "rate-cut trade," triggering a violent rotation of capital out of precious metals and into the hydrocarbon sector.

The immediate implications are profound: the era of cheap money remains a distant memory, and the "soft landing" narrative has been replaced by fears of a stagflationary shock. With the Strait of Hormuz effectively closed and global oil prices surging past $120 per barrel, central banks are prioritizing the fight against energy-driven inflation over economic growth. This shift has removed the primary tailwind for non-yielding assets like gold and silver, which are now being abandoned in favor of "real-economy" assets that benefit directly from supply-side disruptions.

The 'Warsh Shock' and the Hormuz Blockade: A Timeline of Volatility

The market turmoil reached a fever pitch in mid-March 2026, following the escalation of what analysts are now calling the "2026 Iran War." On March 4, the effective closure of the Strait of Hormuz—a chokepoint responsible for nearly 30% of global oil transit—sent shockwaves through energy markets. This was followed by targeted missile strikes on key LNG infrastructure in Qatar, forcing a global scramble for energy security. By late March, Brent crude prices had ascended nearly 40% year-to-date, putting central banks in a defensive crouch.

In Washington, the Federal Reserve, led by Jerome Powell but heavily influenced by the hawkish nomination of Kevin Warsh as his successor, opted to keep the federal funds rate at a restrictive 3.75% to 4.00% range. The Fed’s revised "dot plot" shocked investors by removing two previously anticipated rate cuts for the second half of 2026. Simultaneously, the Bank of Japan surprised the world by holding its short-term rate at 0.75%, its highest level in three decades, while Governor Kazuo Ueda warned that "inflationary risks from imported energy costs" necessitate a continued tightening path.

Initial market reactions were swift and brutal. The "higher for longer" mantra, which many thought would fade by 2026, was reinforced by a strengthening U.S. Dollar. This "Warsh Shock" pushed Treasury yields higher, creating an environment where holding gold and silver became increasingly expensive in terms of opportunity cost. By the end of March, the market had decisively rotated, treating precious metals as sources of liquidity to fund bets on the soaring energy and shipping sectors.

Winners and Losers: The Decoupling of Real Assets

The primary winners of this transition have been the global oil and gas supermajors, which have successfully repositioned themselves as the new "defensive" trade. ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have seen their shares hit all-time highs as investors flock to their insulated production bases in the Permian Basin and Guyana. These companies are viewed as the ultimate hedge against a Middle East supply vacuum. Furthermore, the shipping industry has seen a massive windfall; Frontline (NYSE: FRO) and other tanker operators have watched spot rates for Very Large Crude Carriers (VLCCs) skyrocket to over $400,000 per day as global trade routes are diverted around the Cape of Good Hope.

Conversely, the losers are found in the precious metals and Japanese growth sectors. Despite the geopolitical instability—traditionally a boon for bullion—gold and silver have suffered a "liquidity washout." Newmont (NYSE: NEM) and Barrick Mining Corp (NYSE: B) have seen their margins squeezed between falling metal prices and skyrocketing "All-In Sustaining Costs" (AISC) driven by high diesel and electricity prices. Newmont, in particular, saw its stock plunge over 20% in March as the rising cost of energy-intensive extraction erased the benefits of historically high (but now declining) gold spot prices.

In Asia, the Bank of Japan's hawkishness has hit high-growth tech and manufacturing firms particularly hard. SoftBank Group (TYO:9984) and Toyota (TYO:7203) have faced heavy selling pressure as the double whammy of rising interest rates and surging fuel costs threatens their profitability. Even the heavyweights like Mitsubishi Corp (TYO:8058), which initially benefited from its energy holdings, saw a sharp reversal in late March as fears of a domestic Japanese recession began to outweigh the gains from commodity exports.

A Fundamental Shift in Defensive Strategy

This event signifies a broader industry trend where hydrocarbons are replacing gold as the ultimate safe-haven asset. For decades, investors turned to gold to protect against inflation and geopolitical risk. However, the unique nature of the 2026 energy shock—where the geopolitical risk is the driver of inflation and higher interest rates—has created a scenario where gold's non-yielding nature makes it an inferior hedge compared to "black gold." The rise in real interest rates (nominal rates minus inflation expectations) has historically been the "gold killer," and the current central bank resolve is proving that rule once again.

The ripple effects are extending to the regulatory and policy spheres. Governments in Europe and Asia are reportedly considering emergency subsidies for energy-intensive industries, which could further strain national budgets and lead to a new wave of sovereign debt issuance. This historical precedent is reminiscent of the 1970s oil shocks, but with a modern twist: the transition to green energy has left the global economy with less spare capacity in traditional hydrocarbons, making the current supply squeeze even more volatile.

Furthermore, the Bank of Japan's departure from its long-standing ultra-loose policy is a watershed moment for global carry trades. As the Japanese Yen strengthens and domestic rates rise, the flow of Japanese capital into foreign bond markets is drying up, adding even more upward pressure on global yields and further punishing assets like gold and silver that thrive in low-rate environments.

Looking Ahead: The Risks of a Hawkish Overstep

In the short term, the market will remain laser-focused on the Strait of Hormuz and the potential for any further disruption to LNG flows from Qatar. If the blockade persists through Q2 2026, analysts warn that $150 oil is not out of the question. This would force the Federal Reserve into a corner where they may have to consider rate increases rather than just a "hawkish hold," a scenario that was considered unthinkable only six months ago.

Strategic pivots will be required for investors who have been overweight in "safe-haven" metals or "long-duration" tech stocks. The immediate opportunity lies in energy infrastructure and "brown-to-green" transition plays that can provide immediate energy security. However, the long-term challenge will be navigating a period of persistent inflation. If central banks over-tighten in an attempt to quash supply-side inflation, they risk a deep global recession that could eventually force a chaotic return to rate cuts, though most experts believe that pivot is at least a year away.

Potential scenarios range from a "Stagflationary Grind," where rates and oil stay high for years, to a "Supply Breakthrough," where de-escalation in the Middle East leads to a rapid crash in energy prices. For now, the latter seems unlikely, and the market is pricing in a prolonged period of high-cost energy and restrictive monetary policy.

Conclusion: The New Market Reality

The events of late March 2026 have redefined the relationship between central banks, energy, and safe-haven assets. The "Hawkish Hold" by the Federal Reserve and the Bank of Japan has sent a clear message: the era of prioritizing growth over price stability is over. By quashing rate-cut expectations, central banks have effectively removed the oxygen from the precious metals rally, forcing a mass migration of capital into the hydrocarbon sector.

Investors must now adjust to a market where crude oil (and its producers) is the primary hedge against global instability. Moving forward, the key indicators to watch will be the weekly energy inventory reports and the rhetoric from the "Warsh-led" Fed. If energy prices remain elevated, the rotation out of gold and into the likes of ExxonMobil and Chevron is likely to accelerate. The final takeaway for the months ahead is one of caution; with the tailwinds for gold and silver gone and energy costs acting as a tax on the global economy, the path to a "soft landing" has never looked more treacherous.

This content is intended for informational purposes only and is not financial advice.