Last week, Tesla (TSLA) posted one of its weakest quarterly delivery reports in recent memory. The numbers came in below Wall Street's expectations, dragging TSLA stock lower by 5% in a single trading session.

The electric vehicle maker delivered 358,023 vehicles in the first quarter of 2026, according to a company statement. That was a meaningful miss.

The analyst consensus, compiled by Tesla itself from 23 sell-side firms including Daiwa, Morgan Stanley, Barclays, and JPMorgan, had called for 365,645 deliveries. The median estimate was 363,371.

Tesla missed by about 7,600 vehicles, which is much more than a rounding error.

Tesla Deliveries Continue to Disappoint

Tesla had already posted a rough 2025. The brand took significant reputational hits tied to CEO Elon Musk's political visibility. Competition from Chinese EV makers, particularly BYD (BYDDY), intensified. And U.S. consumer sentiment toward the brand weakened, as evidenced by the sales data.

Coming into Q1, the bar for a recovery was set relatively low. Analysts were looking for signs that consumer demand had stabilized.

Instead, Model 3/Y deliveries came in at 341,893, well below the consensus of 351,179. Other models delivered 16,130 vehicles, which beat the estimate of 13,946. But the Model 3/Y is the key volume driver for Tesla.

For context, Tesla delivered 418,227 vehicles in the fourth quarter of 2025. That means Q1 deliveries fell roughly 14% from just one quarter earlier. Sequential declines in Q1 aren't unusual due to seasonality, but a drop of that size still stings.

What's Next for TSLA Stock?

Tesla will post its full financial results after market close on Wednesday, April 22, 2026. That's when investors will get the revenue and earnings numbers that put the delivery miss in proper context.

According to analyst estimates:

- Q1 revenue is expected to average $22.82 billion, an 18% increase year-over-year (YoY) from $19.34 billion in the year-ago period.

- The earnings per share (EPS) consensus is $0.39 for the quarter, up from $0.27 per share last year.

Both numbers carry wide ranges. Revenue estimates span from $20.28 billion to $24.86 billion. EPS estimates run from $0.22 to $0.54. That kind of dispersion reflects just how uncertain Wall Street is about where Tesla's margins land after another difficult quarter. The full-year 2026 revenue consensus is $103 billion, up from $94.83 billion in 2025, implying roughly 8.6% growth.

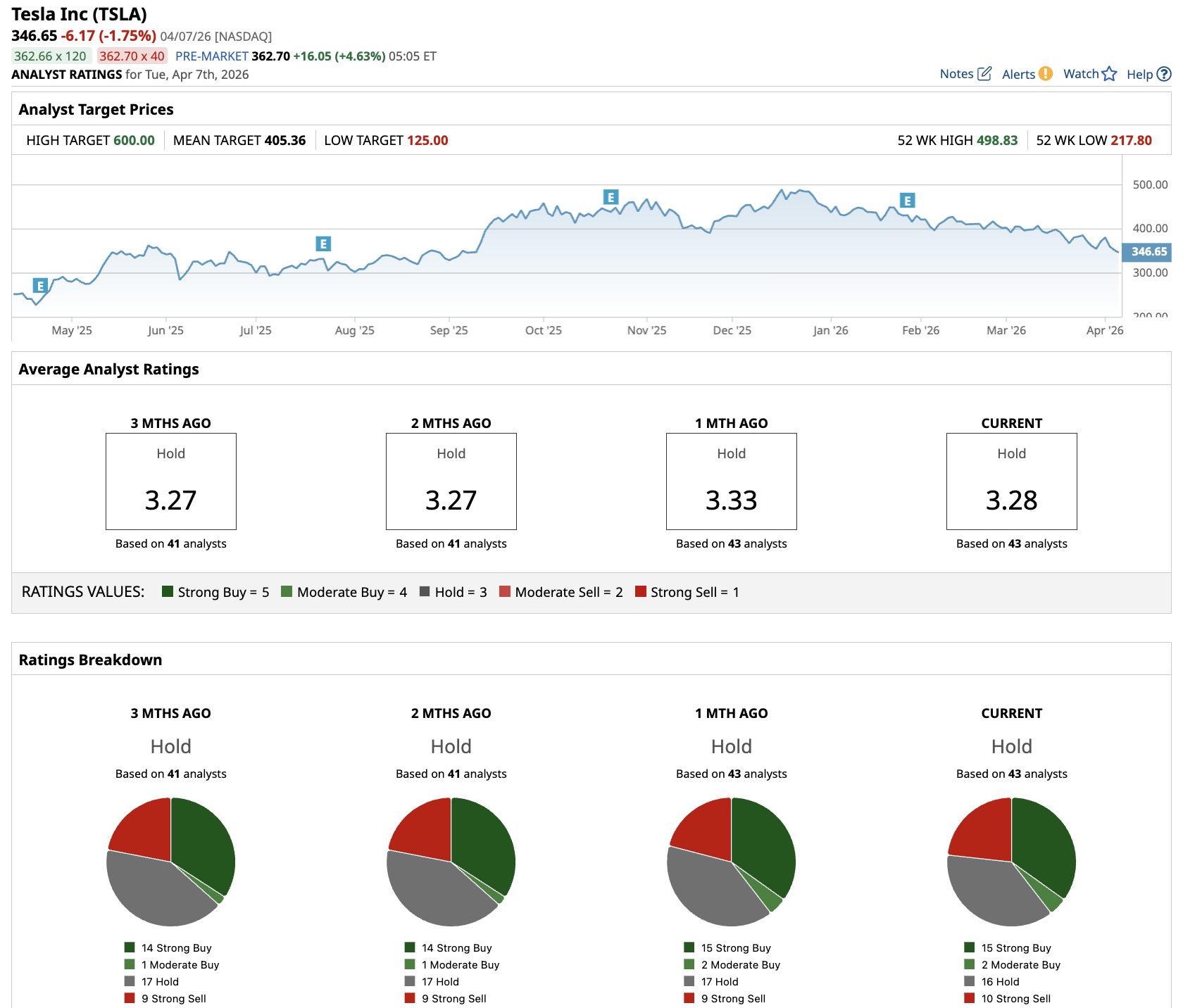

Out of the 43 analysts covering TSLA stock, 15 recommend “Strong Buy,” two recommend “Moderate Buy,” 16 recommend “Hold,” and 10 recommend “Strong Sell.” The average TSLA price target is $405.36, above the current price of about $347.

Robotaxi, Cybercab, and Optimus Could Drive Future Growth

However, Tesla is no longer just a car company, and that's important for investors to keep in mind.

According to a company statement:

- Tesla began removing safety monitors from Robotaxi rides in Austin on a limited basis in January.

- The Robotaxi iOS app no longer has a waitlist in its service areas.

- The Bay Area service expanded to San Jose Airport in October 2025.

These are small steps and come with no guarantees of success, but they mark real commercial progress for what Tesla calls its "physical AI" strategy.

On the manufacturing side, Cybercab and Tesla Semi production ramps are on schedule for the first half of 2026.

The first-generation Optimus humanoid robot production line is being installed, with volume production targeted before the end of the year and an eventual planned capacity of one million robots per year.

Tesla's energy business is also quietly growing. The company deployed 8.8 gigawatt-hours (GWh) of energy storage in Q1 2026.

The full-year 2025 consensus for energy storage is 65.2 GWh. That business hit a record gross profit of $1.1 billion in Q4 2025, its fifth consecutive record quarter.

None of that erases the Q1 delivery miss. But it does explain why some investors are holding on.

The question is whether the autonomous-vehicle and energy stories develop quickly enough to offset the continued pressure on core auto sales. Earnings on April 22 will give a clearer picture of whether Tesla's margins held or slipped further.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart