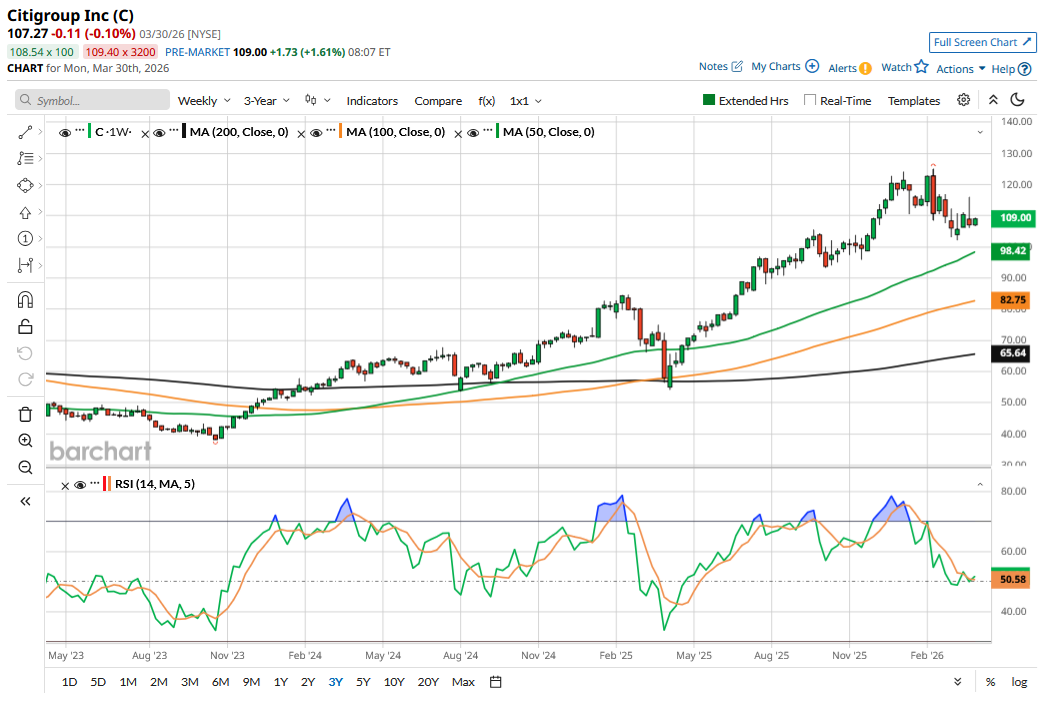

While the escalation in the Iran war has rattled broader markets and the S&P 500 Index ($SPX) is on the verge of correction territory, which by definition is a fall of 10% from the peak, Citigroup (C) shares have fared relatively well and are up about 2% over the last month. Citi has among the highest dividend yields in the banking space, currently yielding over 2.2%. Let's explore whether the stock is a “buy,” particularly for dividend investors.

Why Has Citigroup Outperformed Over the Last Month?

To begin with, let’s analyze why Citi outperformed markets over the last month. Firstly, the tensions in the Middle East are not having much of an impact on Citi’s business. Speaking at the RBC Capital Markets Global Financial Institutions Conference earlier this month, CEO Jane Fraser said that Citi expects mid-teens percentage growth in both investment banking fees and markets revenue for the first quarter of 2026 despite the war in Iran.

On the regulatory front, the Federal Reserve has announced proposals to “modernize the regulatory capital framework” and is currently seeking comments on these. In a nutshell, once adopted, these proposals will lower the regulatory capital requirements for the banking sector.

Additionally, Citi expects its Stress Capital Buffer (SCB) to come down as the bank has lowered its risk profile by exiting some international markets. Notably, as part of the turnaround under Fraser, Citi has flattened its organizational structure, reduced bureaucracy, and is working to address the underlying issues that have put it in the crosshairs with regulators in the past. Lower capital requirements would help Citi increase its share buybacks and perhaps even its dividend.

Citi’s Turnaround Has Largely Played Out

Citi has been a play on the transformation. However, the bank is now in the final leg of its transformation, and during the Q4 2025 earnings call, management noted that 80% of the “programs are now at or nearly at our target state.”

Citi’s turnaround story has largely run its course, which means that the returns over the coming years might not be as stellar as we saw in the previous three years, where the stock rose over 133%, outperforming most of its large-cap banking peers.

Citi trades at a discount to other large U.S. banks as its return and profitability metrics are lower than those of its peers. For instance, Citi’s return on average tangible common equity (RoTCE) was 7.7% last year, and the management reiterated its optimism over achieving an RoTCE of between 10% and 11% this year, which it expects to further increase in the coming years. For context, Bank of America (BAC) reported an RoTCE of 14.2% last year, while the corresponding number for J.P. Morgan Chase (JPM) was 20%.

As Citi continues to deliver on the financial metrics that it has outlined, the stock should be able to bridge its valuation gap with peers even further.

C Stock Forecast

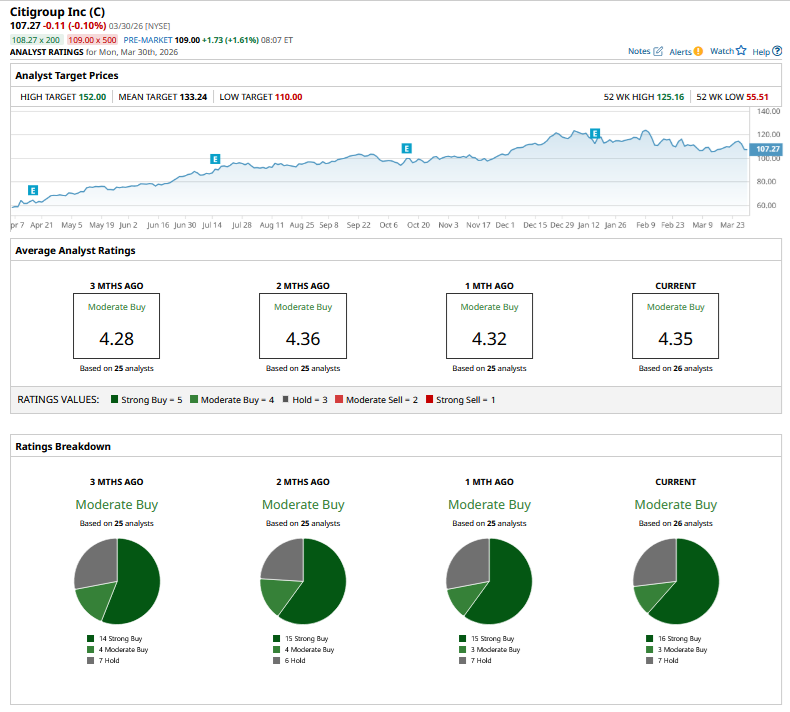

The sell-side analyst community is reasonably bullish on C stock, and it is rated as a “Strong Buy” by 16 of the 26 analysts polled by Barchart. Three analysts rate it as a “Moderate Buy” and the remaining seven as a “Hold.” The stock trades below its Street-low target price of $110, while the mean target price of $133.24 is over 24% higher than current price levels.

Should You Buy C Stock?

In my previous article, I had listed C stock as a decent buy, noting that the risk-reward had become relatively favorable after the crash from the peak. Notably, Citi had a tangible book value of $97.06 at the end of 2025, while the total book value per share was $110.01, which is slightly above where the stock is currently trading.

While the stock's valuation is not as mouthwatering as a couple of years back, when it was trading below the tangible book value, there is a good enough margin of safety at these levels. The stock would particularly fit into portfolios of investors who are looking for high-dividend yielding names that can deliver decent capital returns over the next couple of years.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart