Nio (NIO) stock has gained over 21% over the last five days and is up 13.5% for the year. The price action might not look astonishing in a silo, but it comes at a time when U.S. stocks, including electric vehicle (EV) names, have slumped amid the broader-market meltdown. In my previous article, I noted that NIO’s risk-reward was looking attractive for 2026. With the stock up significantly from those levels, let’s explore whether it can continue its uptrend this year.

Why Is NIO Stock Going Up?

The recent uptrend in NIO has been driven by its strong Q4 2025 performance. While startup EV companies are not exactly known for keeping promises, NIO delivered its first-ever adjusted profit in Q4, as management had guided. And, the company generated positive free cash flows in the quarter and ended the year with cash and cash equivalents of $6.67 billion. It wasn’t a mean achievement given the bloodbath in the startup EV space, where price wars have taken a toll on margins, and many companies continue to burn cash.

NIO's guidance was also quite upbeat, and the top end of its Q1 guidance implies deliveries nearly doubling on an annual basis. NIO tasted success with its new models and is set to launch more models this year, which will help spur sales. While the company expects overall vehicle sales in China to dip this year, it expects battery electric vehicle (BEV) penetration levels to rise.

Notably, while sales of plug-in hybrids have sagged in China, which has particularly taken a toll on BYD’s (BYDDY) fortunes, BEV sales are still strong, which bodes well for companies like NIO, as it only sells BEVs. The management reaffirmed its guidance of volume growth of between 40% and 50% this year, which looks encouraging considering the otherwise sorry state of the country’s automotive industry.

Further, NIO is expanding globally, which would help it increase its volumes. Notably, while multiple countries clamped down on EV imports from China, some are warming up to the world’s second biggest economy. For instance, Canada has lowered tariffs on EV imports from China, albeit with a quota, and the E.U. is considering replacing tariffs with a minimum floor price for Chinese cars. Other countries might also take a more favorable view of EV imports from China, as the spike in oil prices could lead to a renewed push for electric cars.

On the margin front, NIO expects to mitigate the impact of higher input costs, including memory prices, through supply chain optimization. Its margins would also be supported by the launch of new SUV models this year, which typically have a higher margin.

NIO Stock Forecast

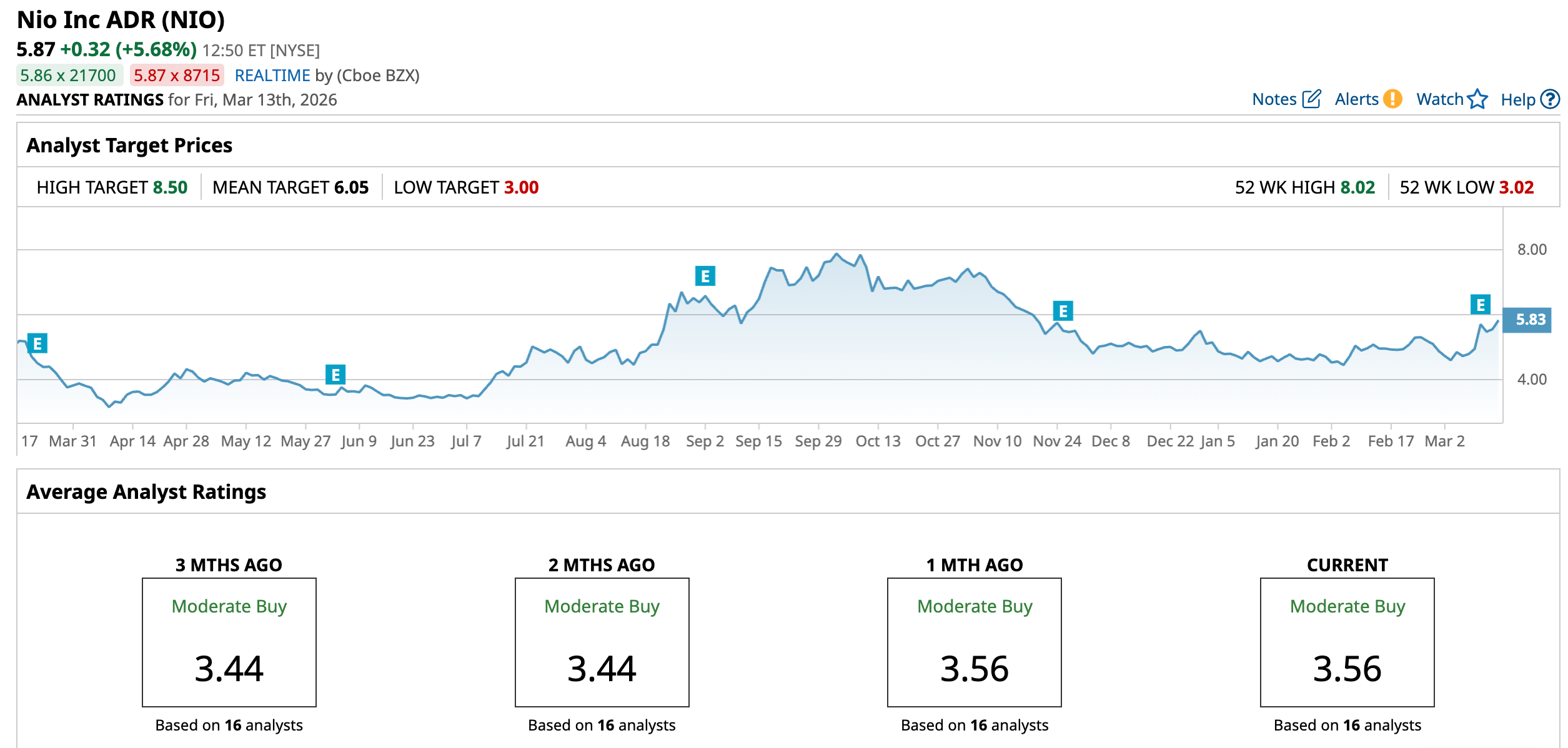

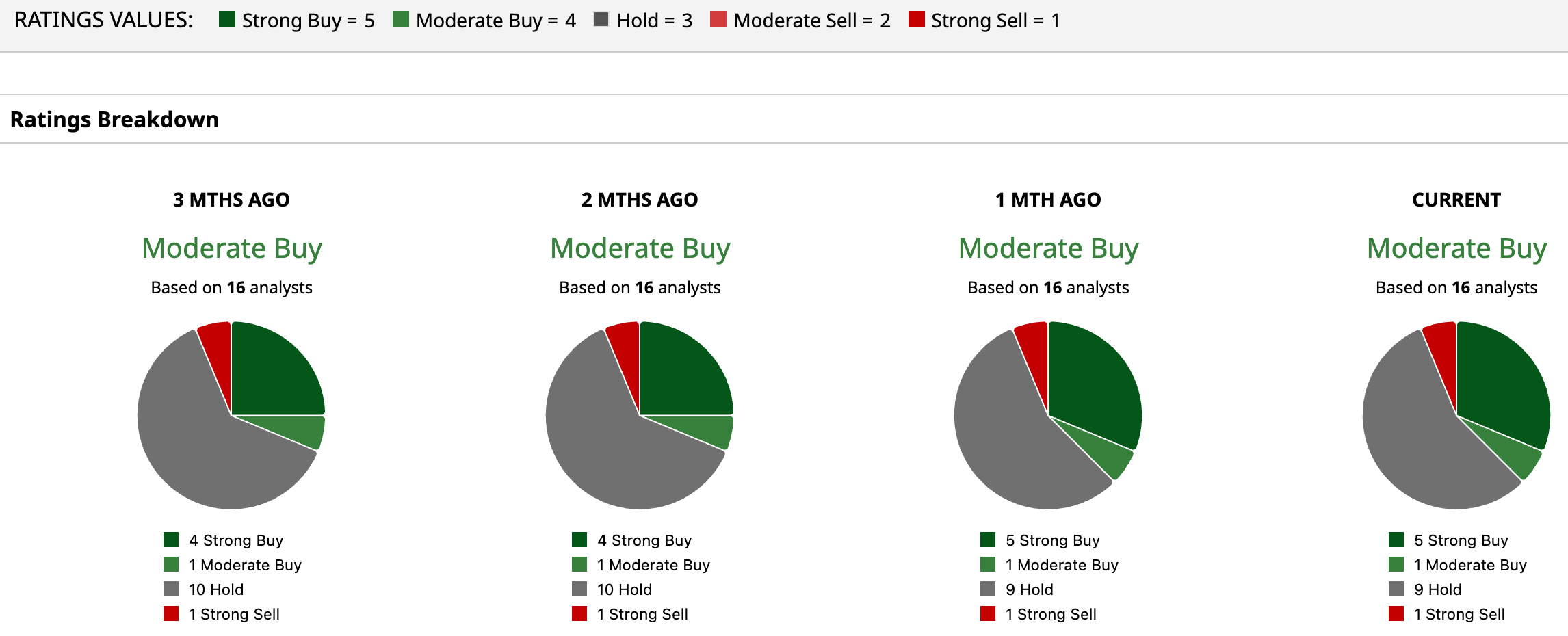

NIO’s strong Q4 performance got a vote of confidence from the sell-side analyst community, and Nomura upgraded the stock to a “Buy” for the first time since 2023, even as it lowered its target price to $6.60. Previously, Macquarie had upgraded the stock to an “outperform” in January. Overall, NIO is rated a “Moderate Buy” with a mean target price of $6.05, which is 3% higher than current price levels.

Can NIO Continue to Outperform in 2026?

China has tweaked the subsidy for EV cars and now offers a 12% subsidy, which is capped at 20,000 yuan. The tweak has dampened sales of budget models as they were previously eligible for the full 20,000-yuan subsidy. Given its higher price point, NIO's premium eponymous brand would still get the full 20,000-yuan subsidy, as under the previous regime. There would be an impact on the budget brand Firefly, but since the bulk of the company’s sales came from the premium NIO brand, it wouldn’t be as impacted as budget EV makers, particularly BYD.

NIO’s chip subsidiary Shenji is developing its second chip and exploring third-party customers, including those in the automotive industry. The company’s chip manufacturing strategy fits well into the Chinese government’s policy of promoting domestic semiconductors and reducing reliance on imported chips. These chips would also help NIO lower input costs as it transitions from Nvidia (NVDA) chips to in-house silicon.

From a valuation perspective, NIO trades at just about 0.76x its expected sales for the current year, which looks quite reasonable to me. With the company delivering on the Q4 adjusted profit guidance and reaffirming up to 50% delivery growth in 2026 despite industry headwinds, I remain constructive on NIO stock and expect it to rise further from these levels this year.

On the date of publication, Mohit Oberoi had a position in: NIO , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart