PFAS Concentration and Destruction Systems Market Accelerates Amid Global Water Safety Regulations

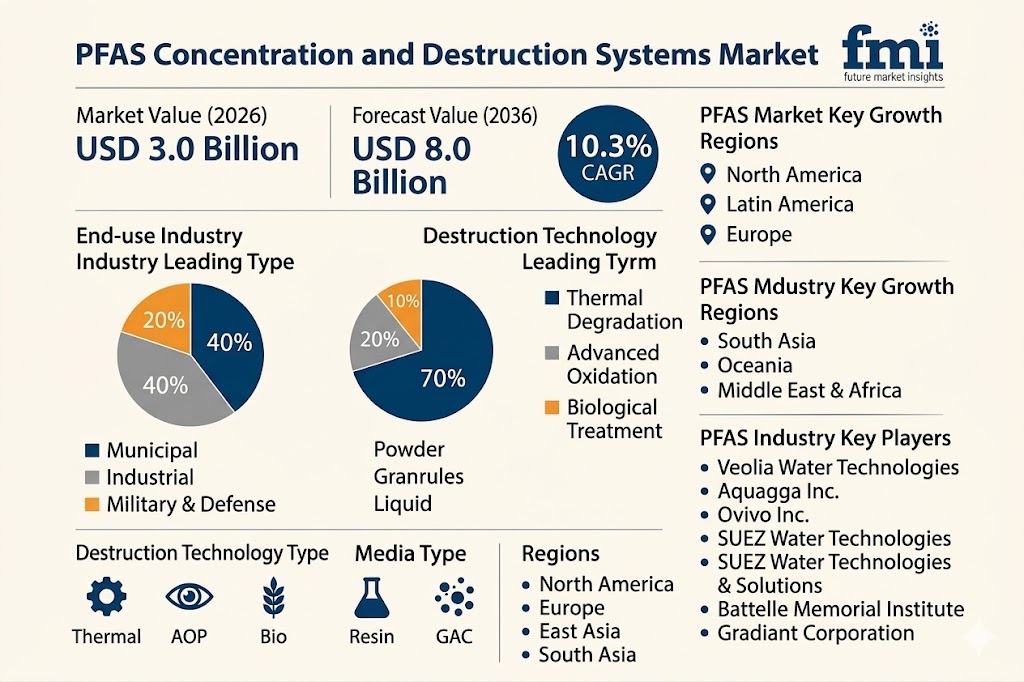

NEWARK, DE / ACCESS Newswire / March 16, 2026 / Rising regulatory pressure on environmental contaminants is reshaping the global water treatment industry. The PFAS Concentration and Destruction Systems Market, valued at USD 3.0 billion in 2026, is projected to reach USD 8.0 billion by 2036, expanding at a CAGR of 10.3% during the forecast period.

The surge in demand is largely driven by the urgent need to eliminate per- and polyfluoroalkyl substances (PFAS) often called "forever chemicals" from drinking water and industrial wastewater systems. Governments, municipalities, and industrial operators are transitioning from temporary containment strategies toward permanent destruction technologies, creating significant opportunities for advanced treatment equipment providers.

Growing concerns about environmental contamination, combined with stricter regulatory frameworks, are accelerating infrastructure investments in next-generation PFAS remediation technologies.

Get Access of Report Sample: https://www.futuremarketinsights.com/reports/sample/rep-gb-32272

Key Market Highlights

Industry value projected to reach USD 8.0 billion by 2036

10.3% CAGR expected from 2026 to 2036

Strong demand driven by EPA regulations and industrial compliance mandates

Municipal water treatment emerging as a major adoption segment

Market Overview

Metric |

Details |

|---|---|

Market Value (2026) |

USD 3.0 Billion |

Forecast Value (2036) |

USD 8.0 Billion |

CAGR (2026-2036) |

10.3% |

Dominant Segment |

Separation & Concentration (62.5%) |

Key Application |

Wastewater Treatment |

Major End-Use |

Municipal Water Utilities |

Regulatory Mandates Drive Infrastructure Transformation

The market's growth trajectory is closely linked to evolving environmental regulations. Governments across North America, Europe, and Asia are implementing strict limits on PFAS concentrations in drinking water and industrial effluent.

For example, the EPA's National Primary Drinking Water Regulation has established extremely low allowable levels for these compounds, compelling municipal utilities to overhaul existing treatment infrastructure.

Instead of relying on traditional filtration or temporary storage solutions, utilities are investing in advanced concentration systems paired with permanent destruction technologies capable of breaking PFAS chemical bonds.

Key Regulatory Drivers

Stricter global drinking water standards

Federal infrastructure funding for remediation

Industrial discharge compliance requirements

Rising public awareness of water safety

These factors are pushing municipalities and industrial facilities to adopt integrated treatment systems that ensure complete mineralization of toxic compounds rather than temporary containment.

Technology Evolution Reshapes PFAS Remediation

Modern PFAS remediation systems combine two critical technological stages: concentration and destruction.

The first stage isolates contaminants from large volumes of water into concentrated brine streams. The second stage uses advanced technologies-such as supercritical water oxidation, electrochemical oxidation, and plasma reactors-to permanently break the strong carbon-fluorine bonds that make PFAS compounds persistent in the environment.

Core Technology Components

Reverse osmosis and membrane filtration systems

Foam fractionation concentration units

Ion-exchange resin vessels

Electrochemical oxidation reactors

Supercritical water oxidation modules

These integrated solutions allow utilities and industrial operators to eliminate PFAS contamination directly at the source while reducing long-term environmental liability.

Market Segmentation Highlights

The PFAS concentration and destruction systems market is segmented by technology, application, and end-use sector.

Technology Segment Leadership

Separation and concentration technologies dominate the market, accounting for 62.5% of the total share in 2026. This stage is essential because high-energy destruction technologies become economically viable only after contaminants are significantly concentrated.

Technology Segment Insights

Separation & concentration: 62.5% share in 2026

Essential for reducing treatment energy costs

Enables efficient downstream destruction processes

Application Segment Growth

Wastewater treatment applications represent the largest market share at 45.0% in 2026, driven by strict discharge regulations across industrial sectors.

Key Application Drivers

Industrial effluent compliance requirements

Semiconductor manufacturing wastewater management

Chemical production facilities adopting zero-liquid discharge policies

End-Use Sector Adoption

The municipal water sector holds a 42.0% share, reflecting growing investments in drinking water safety infrastructure.

Municipal utilities face mounting pressure from regulatory agencies and public health authorities to ensure contamination-free water supply systems.

Regional Outlook: North America Leads Global Adoption

Regional growth patterns reveal strong demand across developed and industrializing economies, though adoption rates vary significantly.

United States: Regulatory Leadership

The United States is projected to grow at a 12.5% CAGR, supported by billions of dollars allocated through federal infrastructure programs aimed at addressing emerging contaminants.

China: Industrial Compliance Push

China is expected to expand at 11.8% CAGR, driven by strict zero-liquid discharge mandates and environmental compliance requirements across large manufacturing sectors.

Europe: Regulatory Alignment

Countries such as the United Kingdom and Germany are witnessing rapid adoption due to evolving environmental frameworks and proposed EU REACH restrictions on fluorinated chemicals.

Asia-Pacific Emerging Growth

Japan, South Korea, and India are increasing investments in PFAS remediation infrastructure, particularly within semiconductor, pharmaceutical, and chemical manufacturing industries.

Top Country Growth Forecast (2026-2036)

USA - 12.5% CAGR

China - 11.8% CAGR

UK - 10.9% CAGR

Germany - 10.8% CAGR

Japan - 9.5% CAGR

South Korea - 9.2% CAGR

India - 8.5% CAGR

Market Challenges and Technology Barriers

Despite strong growth prospects, the market faces several operational and economic challenges. Advanced PFAS destruction technologies often require extreme operating conditions, including high temperatures and pressure levels.

This leads to significant capital expenditure and complex engineering requirements.

Key Industry Challenges

High energy requirements for destruction processes

Corrosion risks in high-temperature reactors

Complex regulatory approval processes

High installation costs for municipal utilities

However, ongoing innovations in modular treatment systems and energy-efficient oxidation technologies are gradually reducing these barriers.

Competitive Landscape: Innovation and Engineering Expertise

The PFAS remediation industry remains moderately consolidated, with technology providers focusing heavily on engineering innovation and proprietary treatment processes.

Leading companies are developing integrated treatment solutions capable of both concentrating and destroying PFAS compounds in a single system architecture.

Key Industry Participants

Veolia Water Technologies

SUEZ Water Technologies & Solutions

Aquagga Inc.

Ovivo Inc.

Battelle Memorial Institute

Revive Environmental

Gradiant Corporation

CycloPure Inc.

Calgon Carbon Corporation

Evoqua Water Technologies LLC

Many of these companies are investing in modular, containerized treatment systems that allow rapid deployment across industrial facilities and municipal water plants.

Outlook: Permanent PFAS Elimination Becomes Global Priority

The PFAS concentration and destruction systems market is entering a critical growth phase as governments and industries transition from temporary containment strategies to permanent chemical destruction.

As environmental regulations tighten and water safety concerns intensify, advanced PFAS remediation technologies are expected to become a core component of modern water infrastructure worldwide.

By 2036, the market is projected to evolve into a multi-billion-dollar sector driven by regulatory enforcement, technological innovation, and global environmental sustainability goals.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Composite Insulator Market through 2036, Full Report Request: https://www.futuremarketinsights.com/reports/pfas-concentration-and-destruction-systems-market

Related Reports:

Composite Roller Market- https://www.futuremarketinsights.com/reports/composite-rollers-market

Dredging Equipment Market- https://www.futuremarketinsights.com/reports/dredging-equipment-market

Laser Vibrometer Market- https://www.futuremarketinsights.com/reports/laser-vibrometer-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

View the original press release on ACCESS Newswire