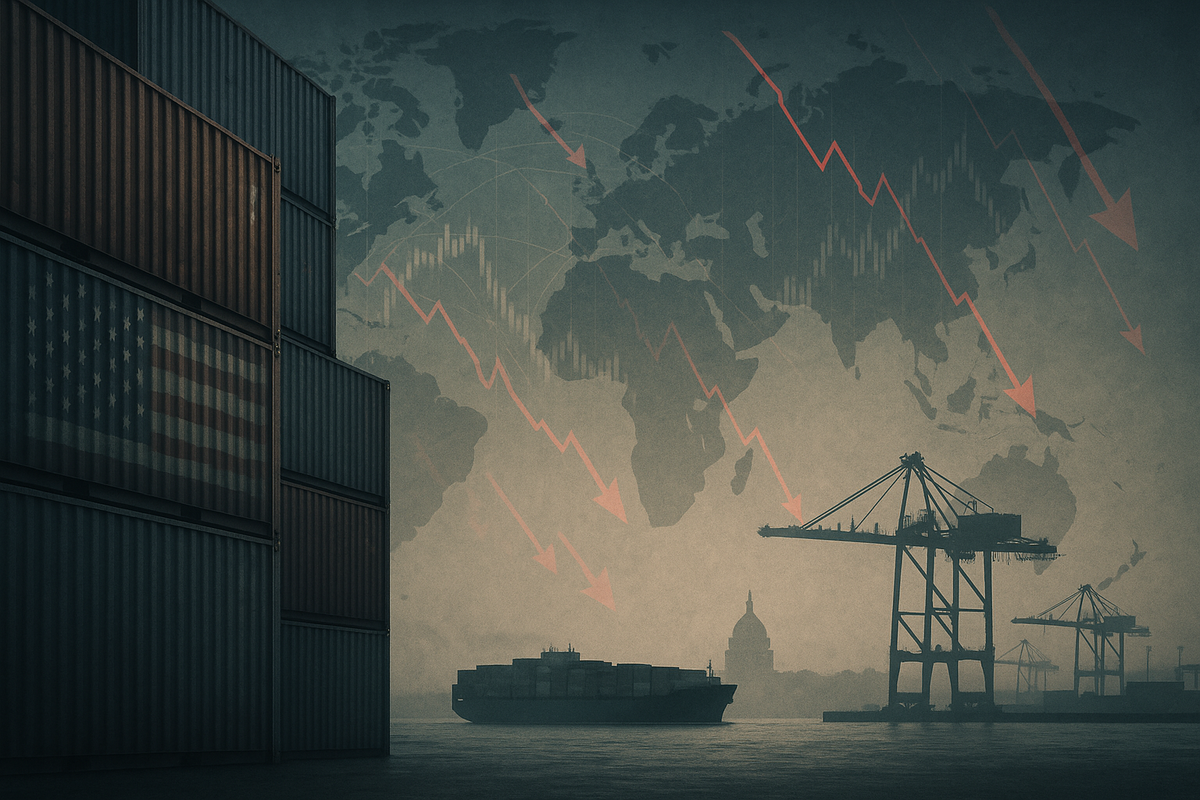

August 2025 has marked a significant turning point in global trade, as the United States enacted a sweeping escalation of trade tariffs, sending shockwaves through international markets and prompting fears of a full-blown global trade war. These aggressive measures, driven by a complex web of economic and geopolitical rationales, have immediately begun to disrupt established supply chains, inflate corporate operating costs, and cast a long shadow over investor sentiment worldwide. The unprecedented scale of these tariffs, with the average U.S. tariff rate estimated to have surged to 18.3%—the highest since 1934—underscores a deliberate strategy by the Trump administration to fundamentally reshape global commerce and assert American economic dominance.

The immediate implications are far-reaching, transforming the landscape for multinational corporations, driving up prices for consumers, and forcing a rapid re-evaluation of global manufacturing and sourcing strategies. With nearly 70 trading partners now grappling with new or increased duties, the stability of the international economic system is under severe strain, pushing many economies into a precarious period of adjustment and uncertainty.

A New Era of Protectionism: What Happened and Why It Matters

The latest round of U.S. trade tariffs, which largely took effect in August 2025, represents a dramatic acceleration of protectionist policies. The administration's rationale is multi-faceted, primarily centered on achieving "reciprocal" trade by imposing duties on imports from countries that tariff U.S. goods, bolstering national security through tariffs on critical materials, coercing trading partners into more favorable bilateral deals, and punishing geopolitical actions deemed contrary to U.S. interests. This aggressive stance aims to upend decades of global trade architecture, assert American economic dominance, and compel domestic production.

Specifically, the tariff hikes have targeted a broad spectrum of nations and goods. Canada faces a hike from 25% to 35% on various imports, while India has been hit with an additional 25% tariff, bringing duties on most Indian goods to 50%, partly in retaliation for its purchases of discounted Russian oil. The European Union, despite some last-minute agreements, is also subject to new tariffs, including a 15% rate on a wide array of goods. Brazil is grappling with 50% tariffs and contemplating legal challenges. China continues to navigate a complex tariff landscape, with overall rates capped at 30% on Chinese imports during a 90-day truce, following a baseline 10% tariff, 20% "fentanyl" tariffs, and 25% Section 301 tariffs that could have escalated much higher. Most Australian goods now face a 10% baseline tariff, and Mexico secured a 90-day extension while negotiations persist. Furthermore, a universal 10% tariff took effect on April 5, 2025, on imports from all countries not subject to specific sanctions, and the de minimis exemption for low-value imports was suspended from August 29, 2025, meaning all commercial shipments are now subject to duty regardless of value.

The targeted goods are extensive, encompassing a broad range of products. Steel and aluminum tariffs were increased to 50%, with new derivative products added, citing national security concerns. Copper also saw a 50% tariff imposed on semi-finished products and copper-intensive derivative goods, such as pipes, wires, rods, and electrical components, effective August 1, 2025. The automotive sector is particularly vulnerable, with a 25% tariff under Section 232 impacting automobiles, light trucks, and certain parts due to their intricate global supply chains. Indian imports, ranging from textiles and footwear to electronics and agricultural products, have also been severely affected. President Trump even threatened a 200% tariff on magnets from China, highlighting concerns over rare earth element supply. This sweeping application of tariffs signifies a profound shift in trade policy, moving beyond targeted disputes to a systemic overhaul of international commerce.

The immediate global reaction has been one of alarm and, in many cases, retaliation. Affected nations have condemned the measures, with some, like Brazil, pledging reciprocal tariffs on U.S.-origin goods. India views the tariffs as "unfair" and is actively diversifying its trade strategy, with some businesses already halting production due to rising costs. The escalating tariffs have led to significant market volatility; benchmark indices like the S&P 500 (SPX) and Nasdaq Composite (IXIC) have experienced declines, and the VIX Index (VIX), often called the "fear index," has soared, reflecting heightened investor anxiety. This climate of uncertainty and the specter of a prolonged trade war underscore the profound impact these policies are having on economic stability and international relations.

Navigating the Storm: Winners and Losers in the Tariff Tussle

The aggressive U.S. tariff escalations are redrawing the lines of profitability and competitiveness, creating clear winners and losers across various industries and companies. Domestically, U.S. industries that compete directly with imports from tariffed countries could see a short-term boost in demand and pricing power. Companies with robust domestic supply chains or those able to quickly reshore manufacturing might gain a competitive edge.

On the losing side are multinational corporations heavily reliant on global supply chains, particularly those sourcing from the newly tariffed nations. Retailers, for example, are facing immense pressure. Companies like Walmart (WMT) and Target (TGT), which import vast quantities of goods, will likely see increased costs, either absorbing them, thereby squeezing profit margins, or passing them on to consumers, potentially impacting sales volume. The automotive sector is particularly vulnerable; manufacturers such as General Motors (GM) and Ford (F), with their intricate international production networks, will face higher costs for imported parts and finished vehicles, potentially delaying investments and hindering innovation. The tariffs on steel and aluminum disproportionately affect industries like construction, machinery manufacturing, and appliance production, impacting companies like Caterpillar (CAT) and Whirlpool (WHR), which use these materials extensively.

Beyond direct import costs, businesses are grappling with increased administrative burdens and the complexities of re-routing supply chains. Companies like FedEx (FDX) and UPS (UPS), while potentially seeing some short-term gains from re-routed shipments, also face the broader economic slowdown and reduced overall trade volumes that tariffs typically bring. Firms in the electronics sector, such as Apple (AAPL), which heavily relies on manufacturing hubs like China, will experience significant cost pressures, prompting them to explore diversification strategies in Southeast Asia and Eastern Europe. However, relocating established infrastructure is a financially and logistically challenging endeavor, incurring substantial capital expenditure and operational disruptions.

The suspension of the de minimis exemption from August 29, 2025, which previously allowed low-value imports to enter duty-free, will significantly impact e-commerce players and small businesses that rely on direct consumer shipments from abroad. This change means every commercial shipment, regardless of value, is now subject to duty, creating a new layer of complexity and cost for platforms like Amazon (AMZN) and countless smaller online retailers. Indian companies, particularly in textiles, footwear, and electronics, are already seeing production halted or severely impacted, leading to a significant loss of market access and revenue. The immediate effect on corporate earnings reports is already becoming evident, with many economists predicting companies will eventually pass on a substantial portion of these direct tariff costs to the end consumer.

Industry Rerouting: Broad Implications and Historical Echoes

The U.S. tariff escalations represent more than just a trade spat; they signify a profound, structural shift with wider industry implications and potentially enduring geopolitical consequences. This event fits into a broader trend of deglobalization and the increasing weaponization of economic policy, where trade tools are employed to achieve political and strategic objectives. The ripple effects are already evident across entire industries, forcing companies to reconsider deeply entrenched global strategies and accelerating the drive towards regionalization and diversification of supply chains.

The automotive sector is a prime example of an industry facing immense pressure. With complex, just-in-time supply chains spanning multiple countries, tariffs on steel, aluminum, copper, and finished vehicles disrupt the entire production process, leading to higher costs, potential shortages, and a slowdown in investment. This pressure could accelerate the adoption of localized manufacturing, where components are sourced and assembled within closer geographic proximity, potentially benefiting U.S. or North American parts suppliers. Similarly, the electronics industry, traditionally reliant on Asian manufacturing, is being compelled to explore alternative production hubs, which could foster new industrial clusters in regions previously less dominant in electronics manufacturing.

Regulatory and policy implications are also significant. These tariff actions are pushing the boundaries of international trade law, prompting legal challenges from affected nations and questioning the future efficacy of multilateral trade organizations like the World Trade Organization (WTO). The U.S. justification of tariffs under national security provisions (Section 232) is setting a precedent that could be exploited by other nations, leading to a more fragmented and less predictable global trading environment. Furthermore, the enhanced enforcement of acts like the Uyghur Forced Labor Prevention Act (UFLPA) alongside new tariffs on sectors like copper and lithium signals a tighter scrutiny of supply chain ethics and origin, adding another layer of compliance complexity for businesses.

Historically, periods of widespread protectionism, such as the 1930s Smoot-Hawley Tariff Act, have often led to retaliatory measures, a contraction of global trade, and exacerbated economic downturns. While modern economies are more integrated, the current tariff environment bears striking similarities, raising concerns about a potential global recession fueled by trade frictions. The aggressive stance also strains diplomatic relations not only with rivals but also with key allies, as evidenced by the "upended" relationship with India and the ongoing negotiations with the EU and Mexico. This trade war is not just an economic phenomenon; it's a geopolitical power play, redefining alliances and global economic order.

The Road Ahead: What Comes Next

The current trajectory suggests a prolonged period of adjustment and uncertainty for the global economy. In the short term, companies will continue to prioritize mitigation strategies: aggressively diversifying supply chains to non-tariffed countries, renegotiating supplier contracts, and exploring options for reshoring or nearshoring production. This will involve significant capital expenditures and operational reconfigurations for many businesses. Consumers, meanwhile, should brace for higher prices across a range of goods as import costs are passed down the value chain, potentially fueling inflation and impacting purchasing power.

Looking further ahead, the long-term possibilities point towards a fundamental restructuring of global trade. We may see the emergence of more regionalized trade blocs, with companies increasingly focusing on producing and sourcing within specific geographic zones to minimize tariff exposure and supply chain risks. This could lead to a less efficient, but more resilient, global production system. Potential strategic pivots will include increased investment in automation and advanced manufacturing technologies within domestic markets to offset higher labor costs associated with reshoring. Furthermore, there may be a resurgence in bilateral trade agreements, as countries seek to carve out exceptions and preferential access outside of the fragmented multilateral system.

Market opportunities could emerge for countries and regions that are either exempt from U.S. tariffs or actively sought out as alternative manufacturing hubs. Nations in Southeast Asia, parts of Eastern Europe, and Latin America, with stable political environments and developing infrastructure, could see an influx of foreign direct investment as companies shift production. Conversely, challenges will persist for export-dependent economies and companies with deeply embedded supply chains in currently tariffed regions. The automotive sector, in particular, will face ongoing pressure to localize production and innovate to manage increased costs.

Potential scenarios range from a gradual de-escalation of tariffs through negotiated settlements, leading to a period of recovery, to a full-blown and protracted global trade war that severely dampens economic growth and exacerbates geopolitical tensions. The latter could lead to further market volatility, reduced corporate profitability, and a significant slowdown in global GDP. The overarching outcome will largely depend on the political will of the involved nations to find common ground and the resilience of businesses to adapt to this rapidly evolving trade landscape.

Conclusion: A New Normal for Global Trade

The U.S. trade tariff escalations of August 2025 represent a pivotal moment, marking a definitive shift towards a more protectionist and fragmented global economic order. The immediate takeaways are clear: heightened corporate costs, disrupted supply chains, and a significant blow to investor confidence. The move has not only impacted bottom lines but has also strained diplomatic relations with allies and rivals alike, ushering in an era of unpredictable trade policies. The market moving forward will be characterized by increased volatility and a constant need for adaptability, as businesses and nations alike navigate a landscape where trade policy is a primary instrument of geopolitical strategy.

This era of aggressive tariffs is forcing a fundamental re-evaluation of how goods are produced, distributed, and consumed globally. While some domestic industries may see temporary benefits, the broader consensus among economists points to a long-term drag on global economic growth, potentially leading to higher inflation and reduced consumer purchasing power. The shift away from efficient global supply chains towards more resilient, regionalized ones is a structural change that will redefine international commerce for years to come, impacting everything from manufacturing footprints to consumer product availability and pricing.

Investors should remain vigilant in the coming months, closely monitoring geopolitical developments, corporate earnings reports for signs of tariff impacts, and the strategic adjustments of multinational companies. Particular attention should be paid to the resilience of supply chains, the ability of companies to pass on costs without significant demand destruction, and the emergence of new trade agreements or retaliatory measures. The overarching message is that the "new normal" for global trade is one of heightened uncertainty and complexity, demanding dynamic strategies and a keen understanding of both economic and political currents. The lasting impact of these tariffs will be felt for generations, reshaping economic partnerships and potentially altering the course of global prosperity.