Over the last six months, Fifth Third Bancorp’s shares have sunk to $40.59, producing a disappointing 6.2% loss while the S&P 500 was flat. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Fifth Third Bancorp, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Fifth Third Bancorp Not Exciting?

Even with the cheaper entry price, we're swiping left on Fifth Third Bancorp for now. Here are three reasons why there are better opportunities than FITB and a stock we'd rather own.

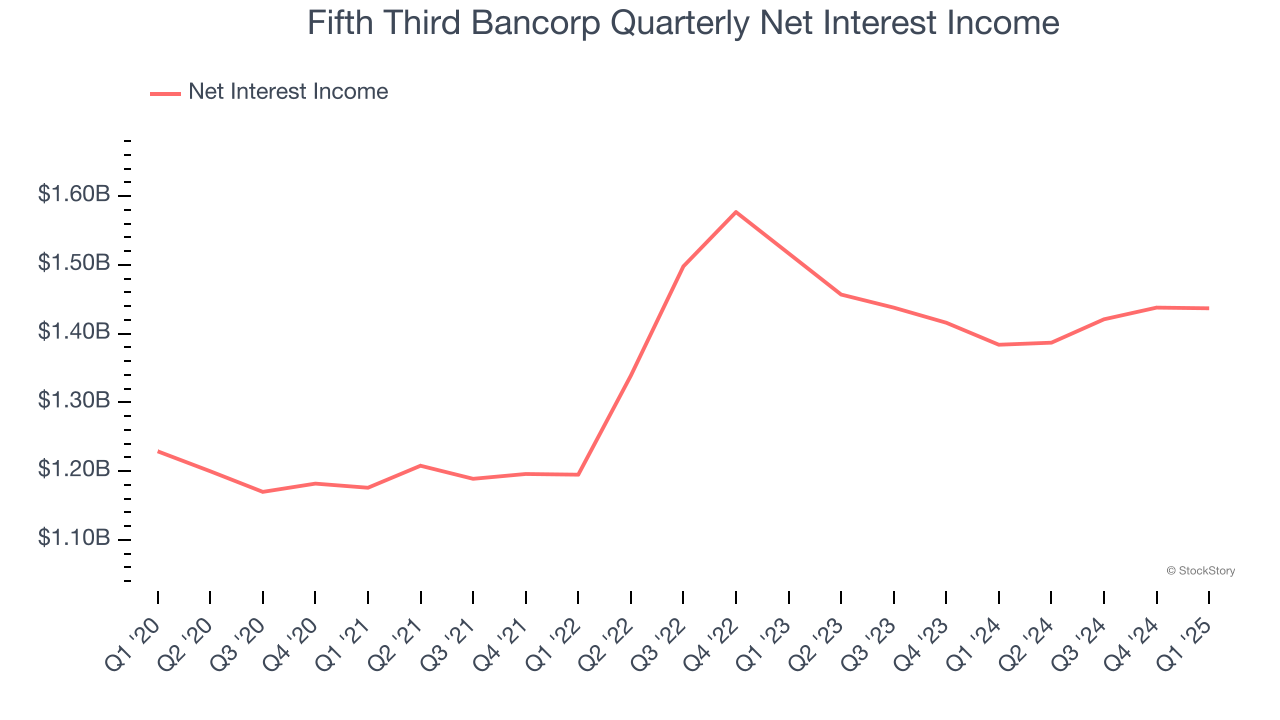

1. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

Fifth Third Bancorp’s net interest income has grown at a 4.7% annualized rate over the last four years, worse than the broader bank industry. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

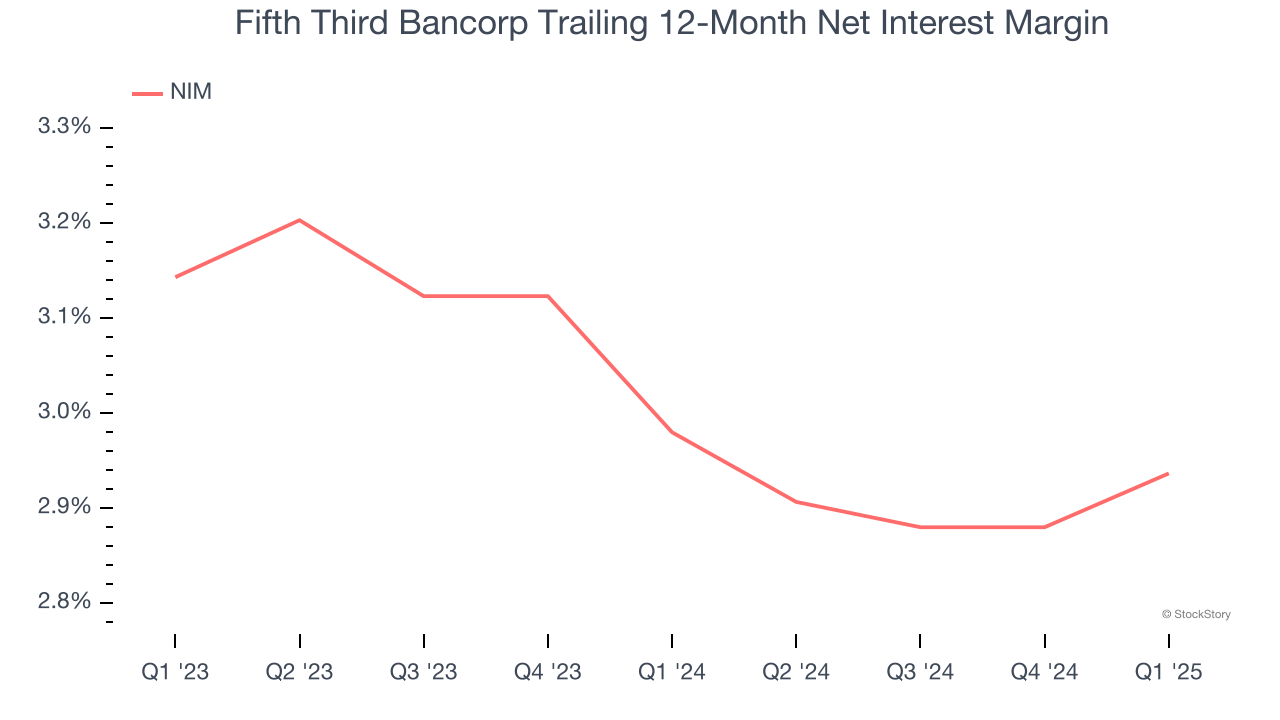

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Revenue is a fine reference point for banks, but net interest income and margin are better indicators of business quality for banks because they’re balance sheet-driven businesses that leverage their assets to generate profits.

Over the past two years, we can see that Fifth Third Bancorp’s net interest margin averaged a weak 3%. This metric is well below other banks, signaling its loans aren’t very profitable.

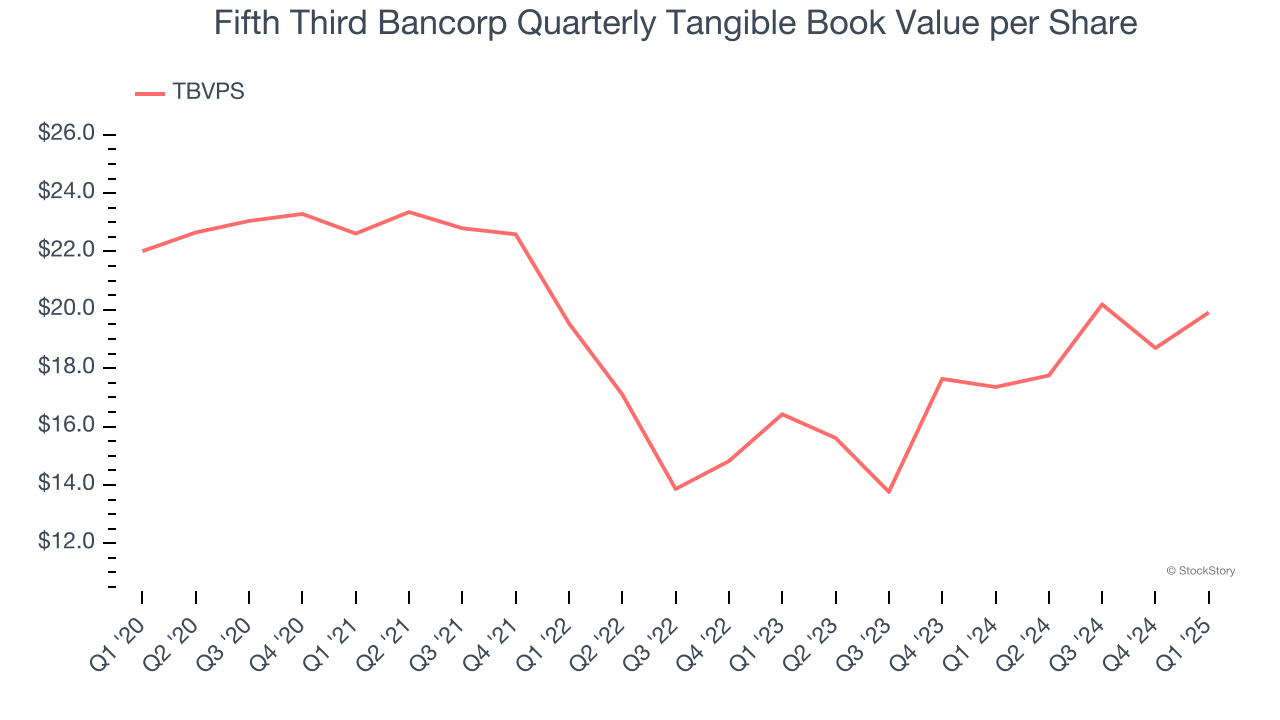

3. TBVPS Growth Demonstrates Strong Asset Foundation

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Although Fifth Third Bancorp’s TBVPS declined at a 2% annual clip over the last five years. the good news is that its growth inflected positive over the past two years as TBVPS grew at a decent 10.1% annual clip (from $16.42 to $19.91 per share).

Final Judgment

Fifth Third Bancorp’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 1.4× forward P/B (or $40.59 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.