Since June 2021, the S&P 500 has delivered a total return of 74.5%. But one standout stock has more than doubled the market - over the past five years, Cummins has surged 165% to $668.50 per share. Its momentum hasn’t stopped as it’s also gained 27.4% in the last six months, beating the S&P by 19.9%.

Is now the time to buy Cummins, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Cummins Not Exciting?

We’re happy investors have made money, but we’re cautious about Cummins. Here are three reasons we avoid CMI, plus one stock we’d rather own.

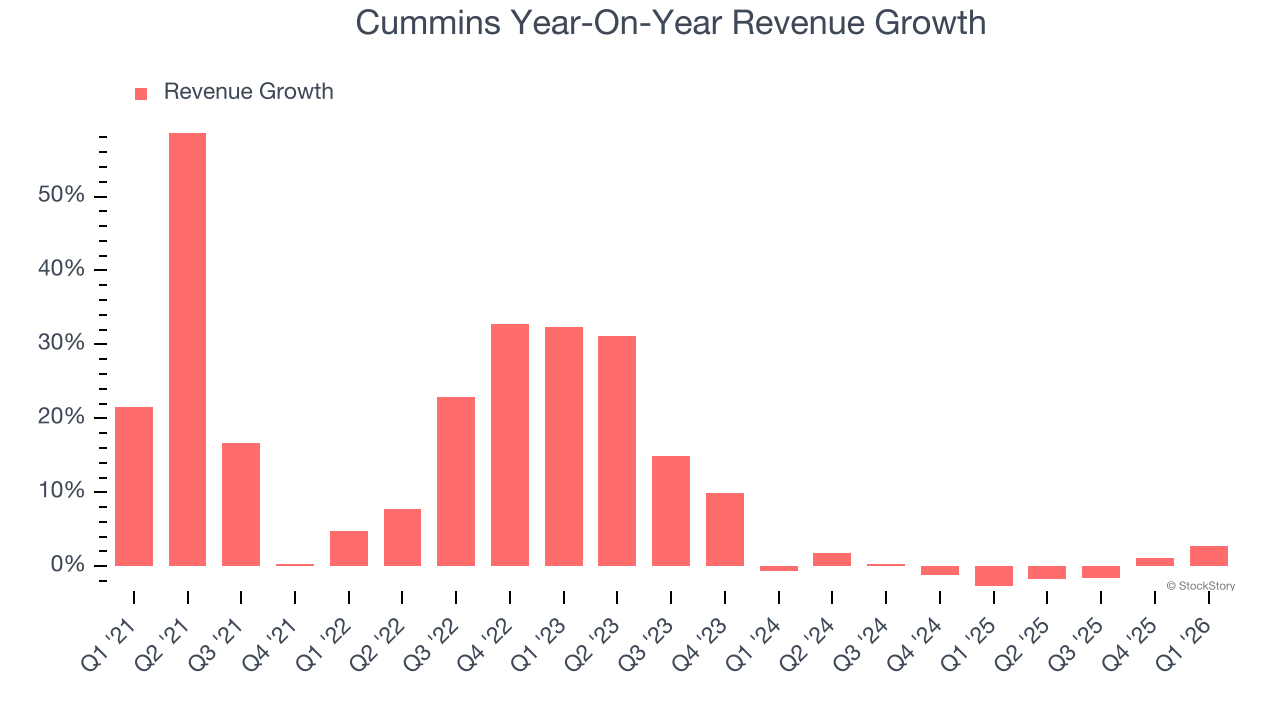

1. Revenue Growth Flatlining

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Cummins’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

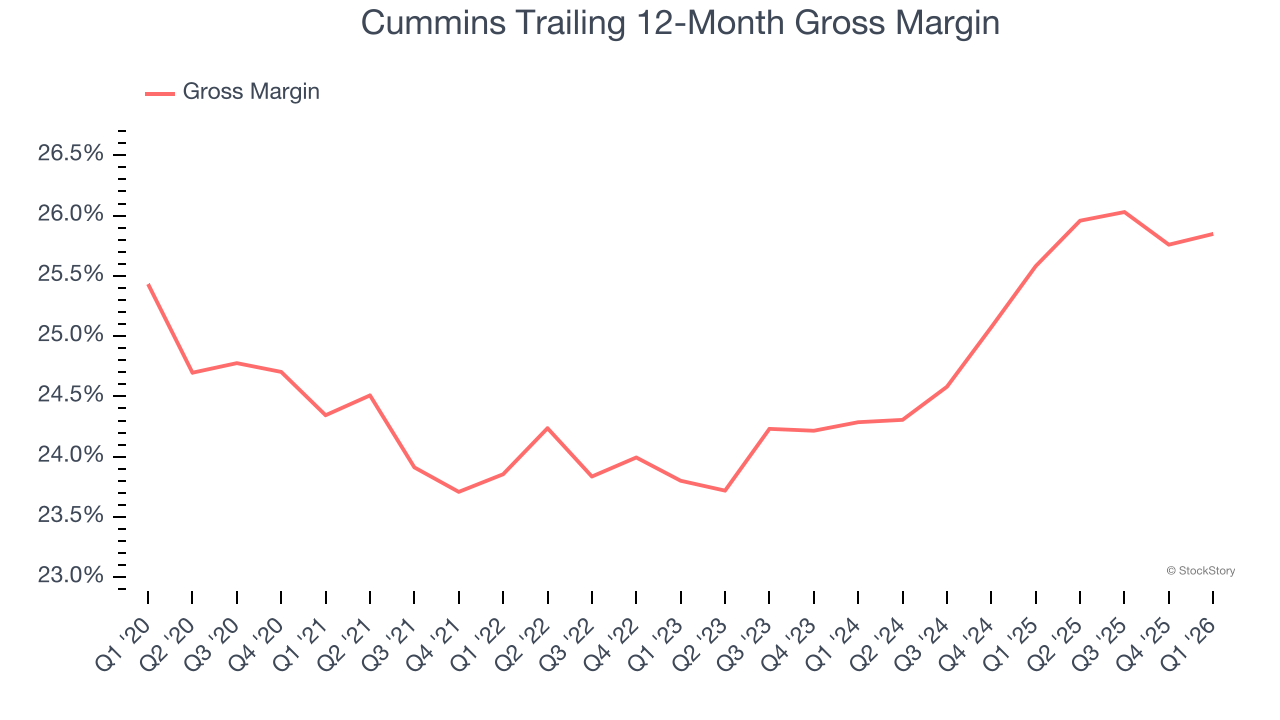

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

Cummins has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 24.7% gross margin over the last five years. Said differently, Cummins had to pay a chunky $75.26 to its suppliers for every $100 in revenue.

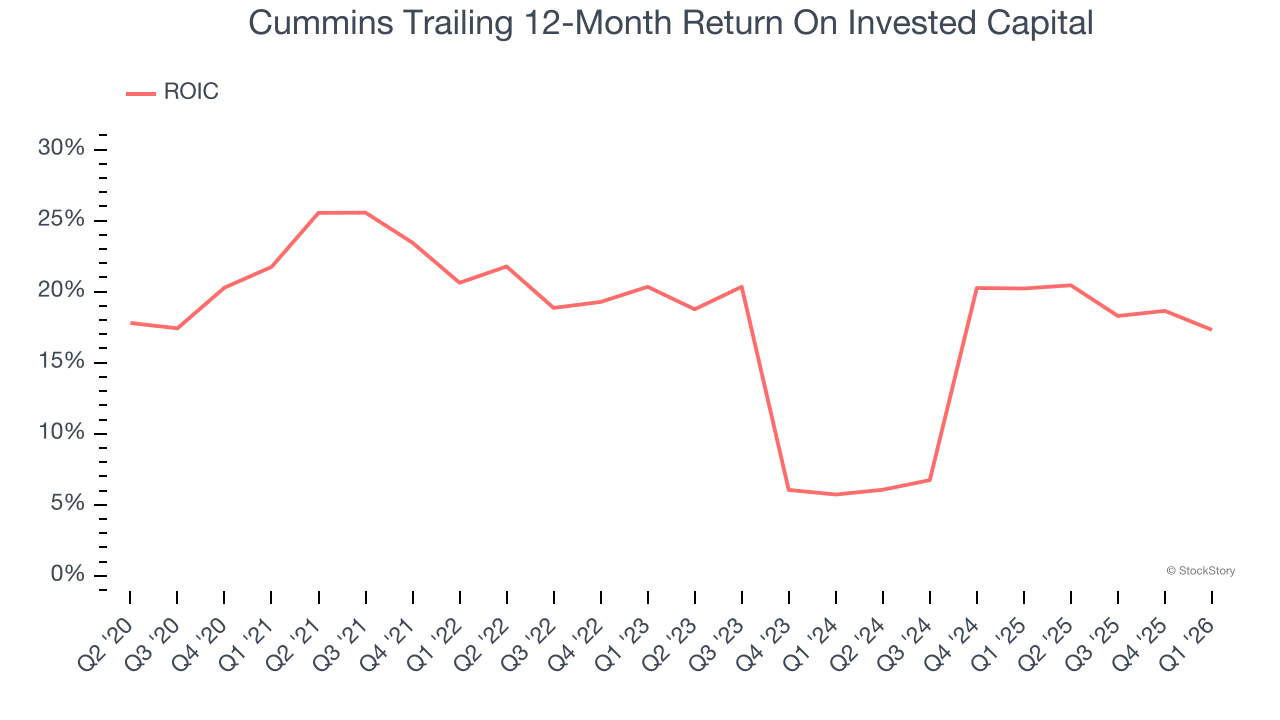

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

Over the last few years, Cummins’s ROIC averaged 1.7 percentage point decreases each year. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Cummins isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 22.1× forward P/E (or $668.50 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our top digital advertising picks.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.