Robust Updated PEA Highlights Ashram's Potential to Become a Strategically Important Long-term Supplier of Rare Earths into Western Critical Minerals Supply Chains

Cautionary Statement

The Preliminary Economic Assessment (PEA) is a preliminary technical and economic study of the potential viability of the Ashram Rare Earths & Fluorspar Project. It is based on low-level technical and economic assessments that are not sufficient to support the estimation of Ore Reserves or to provide assurance of an economic development case at this stage, or to provide certainty that the conclusions of the PEA will be realised. Further exploration, technical, and economic studies are required before the Company will be in a position to estimate any Ore Reserves or to provide assurance of an economic development case. The PEA has been completed to a level of accuracy of ± 50%.

Forward-Looking Statements

The PEA is based on the material assumptions outlined in this announcement. These include assumptions about the availability of funding. While Mont Royal considers all of the material assumptions to be based on reasonable grounds, there is no certainty that they will prove to be correct or that the range of outcomes indicated by the PEA will be achieved.

To achieve the range of outcomes indicated in the PEA, funding in the order of CAD$1.23 billion (initial capital, excluding access road, including 30% contingency) will likely be required. Investors should note that there is no certainty that Mont Royal will be able to raise that amount of funding when needed. It is also possible that such funding may only be available on terms that may be dilutive to or otherwise affect the value of Mont Royal's existing shares. It is also possible that Mont Royal could pursue other value realisation strategies such as a sale, partial sale, or joint venture of the Project. If it does, this could materially reduce Mont Royal's proportionate ownership of the Project.

There is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the determination of Indicated Mineral Resources or that the production target itself will be realised. Given the uncertainties involved, investors should not make any investment decisions based solely on the results of the PEA.

Of the approximately 53 Mt of mill feed underpinning the 30-year production target, approximately 93% is sourced from Indicated Mineral Resources and approximately 7% is sourced from Inferred Mineral Resources.

There is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the determination of Indicated Mineral Resources or that the production target itself will be realised.

The Inferred Mineral Resources do not feature as a significant proportion early in the mine plan. The mine plan is sequenced such that Indicated Mineral Resources predominate in the early years of production, with Inferred Mineral Resources weighted towards the later stages of the mine life. The Company is satisfied that the respective proportions of Inferred Mineral Resources are not the determining factors in project viability.

HIGHLIGHTS1

Updated Preliminary Economic Assessment ("PEA") confirms the Ashram Rare Earths Project ("Ashram" or the "Project") in Québec, Canada, as a large-scale, long-life North American rare earth development.

Large-scale production profile:

Average annual production of ~17,466 tonnes of saleable Rare Earth Oxide (REO)

Average annual production of ~4,035 tonnes of Nd2O3 & Pr2O3 (NdPr)

~100 tonnes of Dy2O3 & Tb2O3 (DyTb)

~ 230 tonnes of Y2O3 (Y)

Initial mine life of 30 years supported by a resource base that remains capable of further expansion, with 93% of the resource schedule in the Indicated category.

Base case utilises only 25% of the current global resource, highlighting significant long-term expansion optionality

Initial nameplate mill throughput of ~1.8Mtpa supporting a long-life open pit operation with a low strip ratio of 0.4:1

Robust project economics:

Post-tax NPV8% (real) of CAD$2.03B

Post-tax IRR (real) of 22.0% and post-tax payback of 3.9 years from commencement of production

Life of Mine (LOM) revenue of ~CAD$24.6B and a life-of-mine EBITDA margin of ~62.7%

Initial CAPEX of ~CAD$1.23B, including 30% contingency, with access infrastructure costs assumed under a contracted/shared logistics model and reflected in operating expenditure

The project is anticipated to benefit from ~CAD$342M of refundable Clean Technology Manufacturing Investment Tax Credits (CTM ITC) incorporated into post-tax cash flows

Competitive cost position:

C1 cash cost of approximately CAD$17.99/kg saleable REO

AISC of approximately CAD$18.58/kg saleable REO

Cost profile supported by low strip ratio, favourable mineralogy, production of a high-grade rare earth concentrate and an integrated hydrometallurgical refining strategy

Strategic project positioning:

Ashram is one of the largest monazite-dominant rare earth deposits in North America

The Project offers exposure to a high-value magnet rare earth basket led by NdPr with additional Dy and Tb content, and potential future fluorspar value upside

Integrated development concept incorporates on-site concentration at Ashram and downstream hydrometallurgical refining in Saguenay, Québec

Located in Québec, one of the world's leading mining jurisdictions

Ashram is well positioned to support Western government and industry initiatives aimed at establishing secure critical minerals supply chains outside China

Additional value upside:

Potential inclusion of a dedicated fluorspar recovery circuit in future studies

Broader district exploration upside across additional targets within the Eldor carbonatite complex, including satellite targets such as Mallard

Potential future inclusion of higher-value zones, including the BD Zone, subject to further test work and study

Downstream and strategic partnership opportunities

Opportunity to optimise road access costs. A regional shared infrastructure strategy is being evaluated as a means of reducing access road costs through potential collaboration with other mining projects, government agencies, and First Nations.

Next steps:

Progression toward a Pre-Feasibility Study (PFS), targeted to commence in H2 CY2026

Ongoing metallurgical optimisation, engineering refinement, and workstreams to further de-risk the flowsheet and development pathway

Advancement of environmental baseline, permitting and stakeholder engagement programs across both the Ashram and Saguenay development footprint

Continued engagement regarding offtake, downstream and strategic partnership opportunities

Mont Royal's Managing Director, Mr. Nicholas Holthouse, said:

"The updated PEA marks a major step forward for the Ashram Project, confirming a large-scale, long-life development with strong underlying economics and a clear pathway to advancement. The study has highlighted Ashram's combination of scale, favourable mineralogy and competitive cost profile, supporting its potential to become a meaningful long-term supplier of rare earth products into Western supply chains. Importantly, we see further upside beyond the base case, including opportunities in fluorspar, resource expansion and downstream partnerships and collaboration.

This is a project that can have a meaningful and long-lived impact on the development of rare earth industries and technologies within Quebec, Canada, North America and Europe.

Our focus now is continuing to work with First Nations and Government agencies on developing infrastructures strategies and on progressing the project into pre-feasibility, advancing permitting and continuing engagement with strategic and offtake partners."

PRELIMINARY ECONOMIC ASSESSMENT OVERVIEW

Montreal, Quebec--(Newsfile Corp. - June 8, 2026) - Mont Royal Resources Limited (ASX: MRZ) (TSXV: MRZL) ("Mont Royal" or the "Company") is pleased to present an updated Preliminary Economic Assessment ("PEA") for its 100%-owned Ashram Rare Earths and Fluorspar Project located in Nunavik, Québec, Canada.

The PEA was completed by Altris Engineering ("Altris") in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") in collaboration with the following specialist firms:

- Altris Engineering

- BBA Inc. (BBA)

- PLR Resources Inc. (PLR)

- DRA Americas Inc. (DRA)

- L3 Process Development (L3)

- ASDR Canada Inc.

- TALA Geotec

- Norda Stelo Inc.

The updated study incorporates significant optimisation work completed since prior economic studies, including:

revised mining and processing assumptions;

optimisation of transportation and logistics pathways;

incorporation of a proposed hydrometallurgical processing facility in Saguenay, Québec;

updated infrastructure assumptions; and

revised engineering and metallurgical inputs.

The PEA highlights the potential for Ashram to become a major long-term supplier of rare earth products into Western and allied critical mineral supply chains.

Ashram is one of the largest monazite-hosted rare earth deposits in North America and contains a favourable distribution of magnet rare earth elements, including neodymium and praseodymium ("NdPr"), which are critical components used in EVs, permanent magnets, wind turbines, robotics, semi-conductors, aerospace technologies and defence applications.

The Economic Summary and metrics for the project are shown below in Table 1 and Table 2.

TABLE 1: Updated PEA - Economic Summary

| Economic Metrics | Unit | Value |

| LOM Revenue | CAD M | 24,638 |

| LOM EBITDA | CAD M | 15,460 |

| EBITDA Margin | % | 62.7% |

| LOM Undiscounted Post-Tax Cashflow | CAD M | 8,365 |

| NPV8% Post-Tax (real) | CAD M | 2,026 |

| NPV8% Pre-Tax (real) | CAD M | 3,440 |

| IRR Post-Tax (real) | % | 22.0% |

| IRR Pre-Tax (real) | % | 25.6% |

| Post-Tax Payback | years | 3.9 |

TABLE 2: Operating cost profile

| Unit Cost Metric | Unit | Value |

| C1 Cash Cost | CAD/kg saleable REO | 17.99 |

| AISC | CAD/kg saleable REO | 18.58 |

PROJECT OVERVIEW AND HISTORY

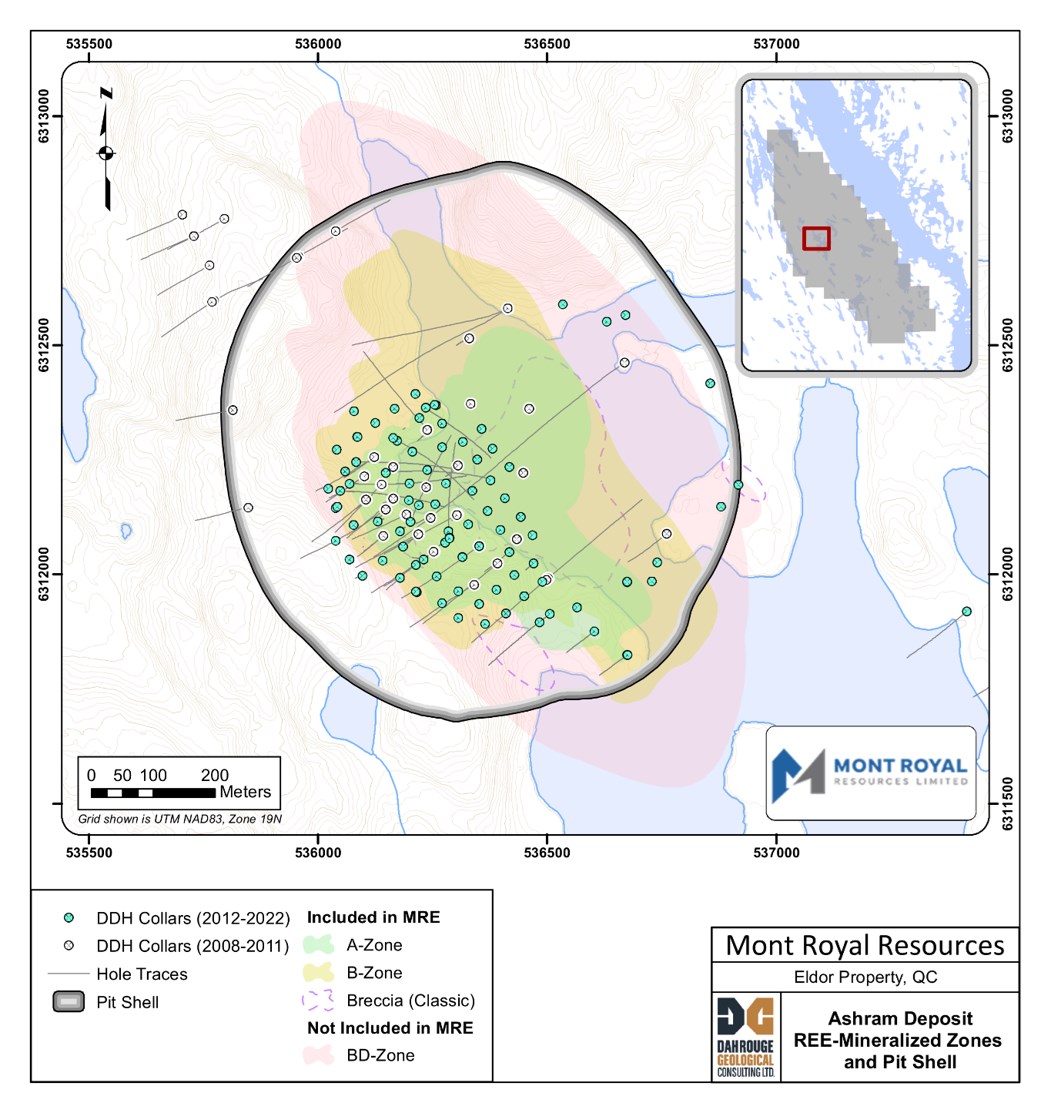

The Ashram Project is located on Mont Royal Resources' 100%-owned Eldor Property in Nunavik, northern Québec, approximately 130km south of Kuujjuaq, and covers 11,475ha across 244 contiguous Exclusive Exploration Rights (EERs) as shown in Figure 1.

Figure 1: Ashram REE and Fluorspar Project location

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_001full.jpg

The Project hosts the Eldor Carbonatite Complex, including the Ashram Rare Earth and Fluorspar Deposit, with additional potential for niobium, tantalum and phosphate mineralisation.

Following the merger between Commerce Resources and Mont Royal Resources in October 2025, the combined group consolidated ownership and strategic direction for the Project.

Commerce Resources Corporation holds a 100% interest in all EERs, which are in good standing until May 2027. Importantly, the Ashram Deposit is not subject to the limited third-party royalties applicable to a small number of original claims. The Property is fully permitted for exploration, with no known material environmental, legal or access constraints.

The Project is accessible via Kuujjuaq, which serves as the primary logistics hub with regular air services from Montréal and seasonal marine supply access. A permanent on-site exploration facility, Camp Valcourt, supports year-round operations and accommodates up to 35 personnel.

The Project benefits from several strategic infrastructure advantages, including:

access to established logistics corridors;

proximity to potential port infrastructure;

access to low-cost renewable hydroelectric power in Québec (Saguenay site);

a supportive mining jurisdiction; and

access to established industrial infrastructure in Saguenay.

Since acquiring the Property in 2007, Commerce has completed extensive drilling, geophysical surveys, trenching and surface exploration programs.

The Ashram REE Deposit was discovered in 2009, with subsequent drilling confirming a large-scale, continuous mineralised system extending from surface to depth.

This work supported the establishment of NI 43-101 compliant Mineral Resource Estimates, which have since positioned Ashram as one of the largest undeveloped rare earth deposits in North America.

GEOLOGICAL SETTING

Ashram is hosted within the Eldor Carbonatite Complex, a large intrusive carbonatite system located within the Paleoproterozoic New Québec Orogen.

Rare earth mineralisation is dominated by monazite, with subordinate bastnäsite, parisite and xenotime. The relatively simple and commercially favourable mineral assemblage is considered advantageous for metallurgical recovery and downstream processing.

The deposit includes several mineralised zones, including:

A-Zone;

B-Zone;

Breccia Zone; and

BD-Zone.

These zones vary in texture and grade, with the A-Zone hosting the highest and most continuous REE grades. Niobium and tantalum mineralisation occurs elsewhere in the complex, mainly hosted in pyrochlore-group minerals within carbonatite and phoscorite units.

The relatively simple mineral assemblage is considered commercially favourable and comparable to other major carbonatite-hosted REE systems globally, including Mountain Pass (USA), Niobec (Québec) and Palabora (South Africa).

MINERAL RESOURCE ESTIMATE

The updated PEA uses the updated JORC MRE for the Ashram Deposit released on October 1, 2025 (Table 3). The Ashram MRE integrates drilling data collected between 2008 and 2022 and was completed using industry-standard geological modelling and geostatistical methods.

A total database of 213 drill holes, six surface channels, and nearly 33,000 samples underpin the estimate, with mineralisation defined within three REE-bearing domains (A-Zone, B-Zone, and Breccia Classic). The drill hole collars are shown below in Figure 2.

Figure 2: Carbonatite Complex Geology of the Ashram Project.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_002full.jpg

Ordinary kriging was applied within a detailed 3D block model constrained by a conceptual open-pit shell developed to demonstrate reasonable prospects for eventual economic extraction.

The estimate is classified in accordance with CIM standards, defining Indicated and Inferred Resources based on drill spacing, geological confidence, and grade continuity; no Measured Resources are defined at this stage. The confidence categories assigned under the CIM Definition Standards were reconciled to the confidence categories under the JORC Code, as disclosed in the Company's Prospectus released to ASX on 1 October 2025.

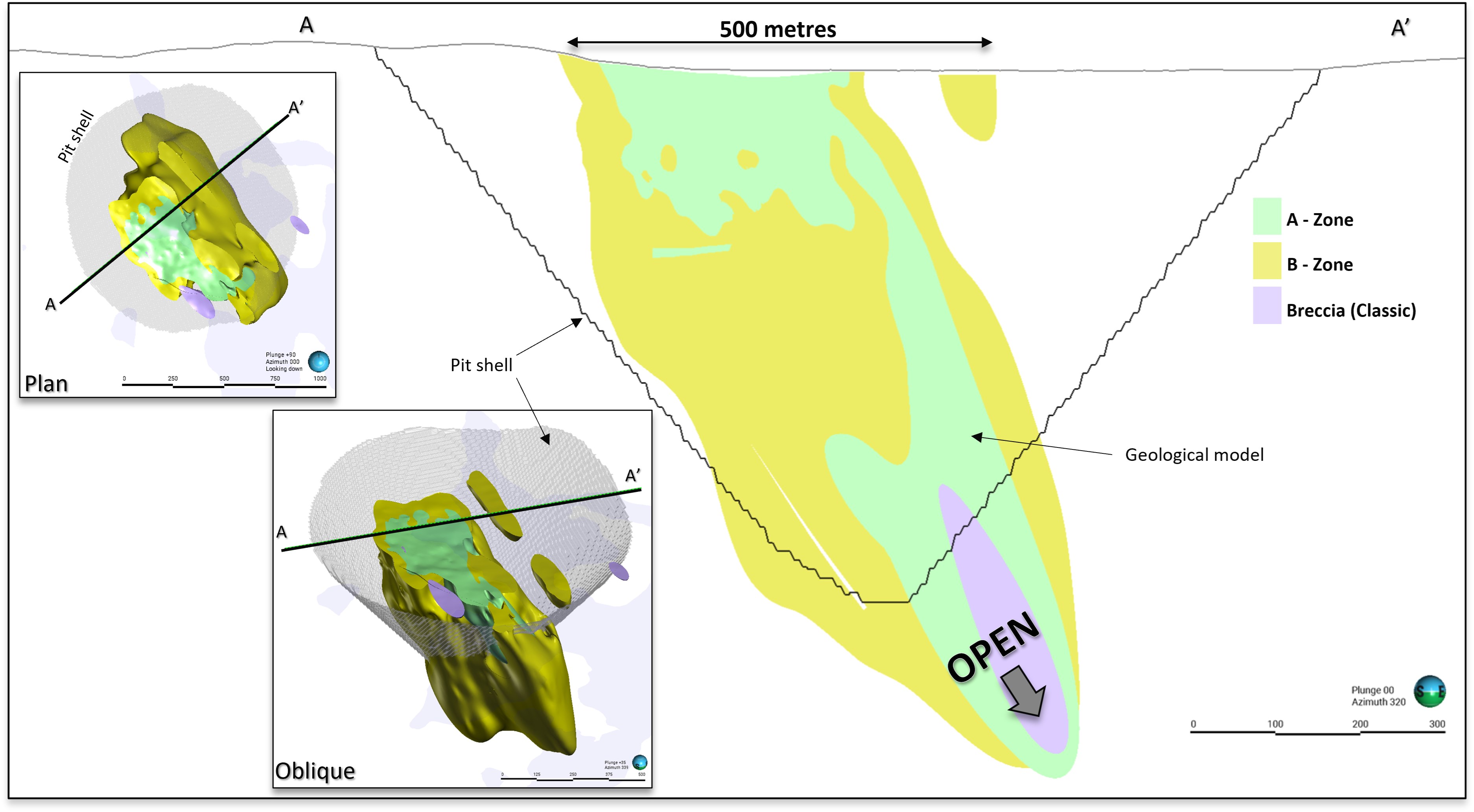

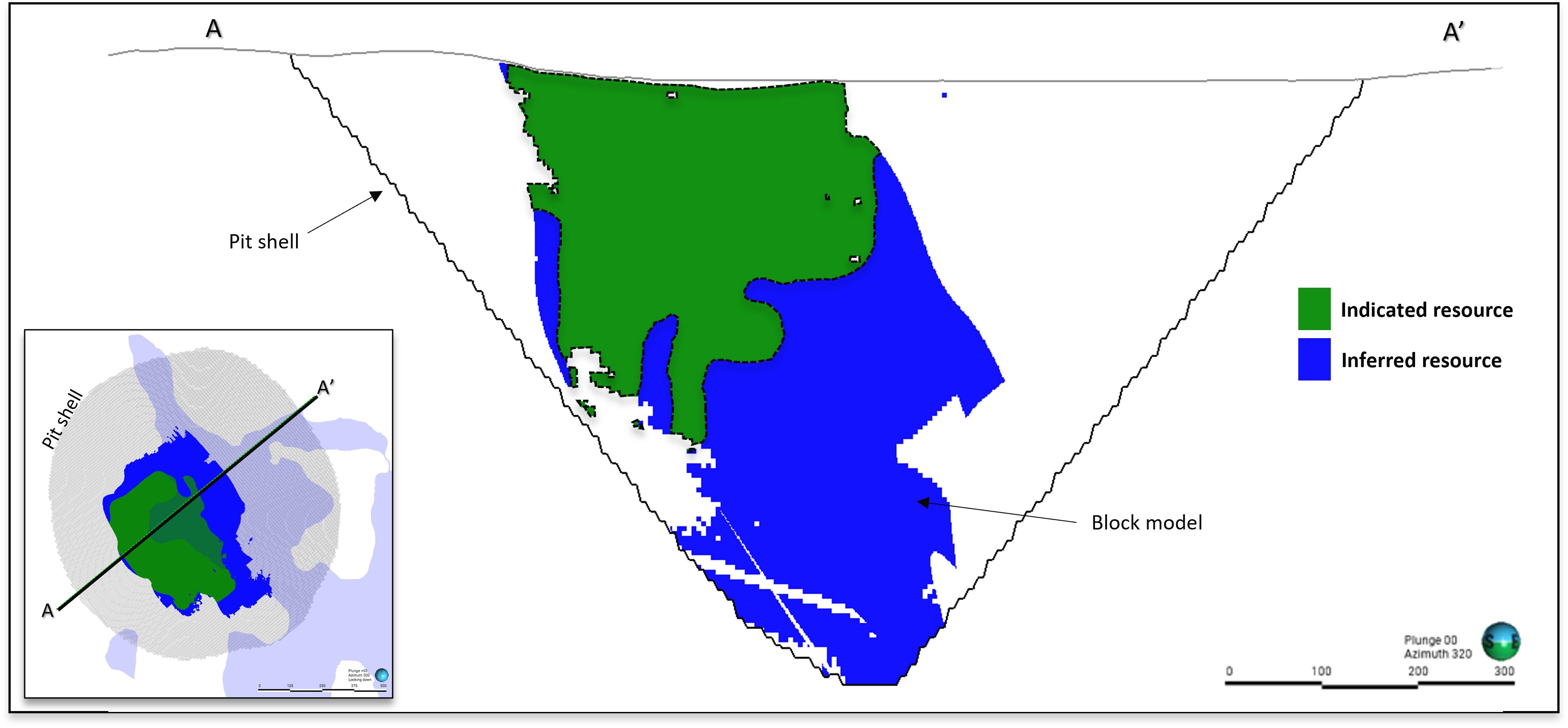

Interpreted zones are shown below in the cross-section in Figure 3 with Figure 4 showing the block model coloured by resource classification within the resource shell.

Figure 3: Geological model cross-section of the Ashram Deposit, highlighting carbonatite lithological domains considered in the MRE.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_003full.jpg

Figure 4: Cross-section showing Indicated and Inferred classifications within the block model.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_004full.jpg

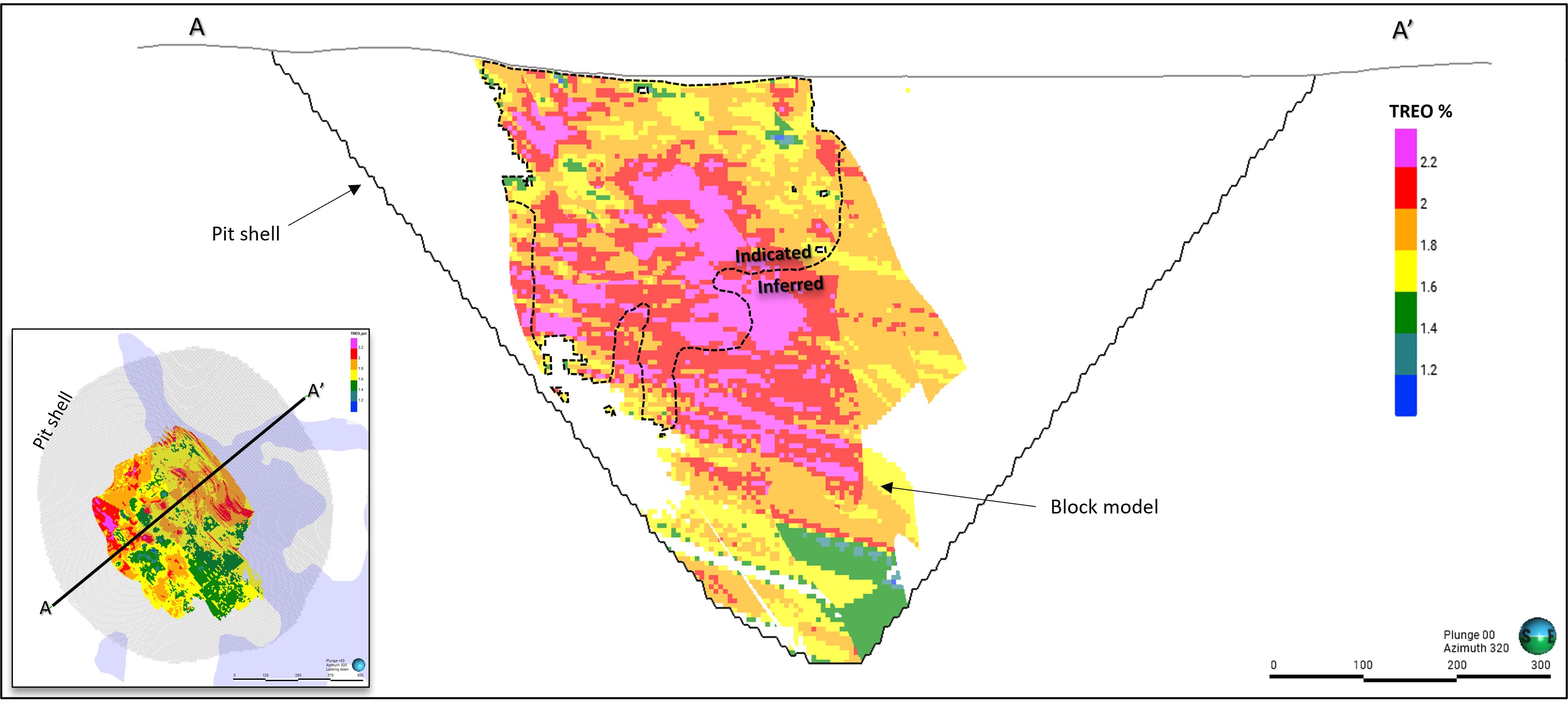

Figure 5: Cross-section showing the TREO % distribution.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_005full.jpg

Using a base case, net metal return (NMR) cut-off of CAD$287/t, the MRE defines 73.2 Mt of Indicated Resources grading 1.89% Total Rare Earth Oxides (TREO) and 131.1 Mt of Inferred Resources grading 1.91% TREO. The resource exhibits a favourable rare-earth distribution, with NdPr accounting for approximately 21% of TREO and meaningful contributions from the critical heavy rare earths Tb and Dy with Figure 5 showing TREO distribution.

Mineralisation remains open laterally and at depth, and the estimated pit shell outlines a large, continuous deposit with a conceptual strip ratio across the entire MRE of approximately 2.7:1.

Table 3: 2025 Ashram Project Mineral Resource Estimate

| Cut-off NMR | CAD $287 / tonne | ||

| Category | Unit | Indicated | Inferred |

| Tonnes | Mt | 73.2 | 131.1 |

| Total TREO | % | 1.89 | 1.91 |

| Nd+Pr Oxide/TREO | 21.2 | 21.4 | |

| Dy+Tb Oxide/TREO | 0.7 | 0.5 | |

| La2O3 | ppm | 4,829 | 4,969 |

| Ce2O3 | 8,753 | 8,933 | |

| Pr2O3 | 907 | 927 | |

| Nd2O3 | 3,112 | 3,162 | |

| Sm2O3 | 412 | 385 | |

| Eu2O3 | 98 | 87 | |

| Gd2O3 | 223 | 195 | |

| Tb2O3 | 24 | 19 | |

| Dy2O3 | 102 | 73 | |

| Ho2O3 | 14 | 10 | |

| Er2O3 | 31 | 21 | |

| Tm2O3 | 3 | 2 | |

| Yb2O3 | 18 | 13 | |

| Lu2O3 | 2 | 2 | |

| Y2O3 | 419 | 280 | |

| Fluorspar (CaF2) | % | 6.6 | 4.0 |

(a) TREO is sum of lanthanides (as oxides) + yttrium oxide

(b) NdPr distribution calculated as (Nd2O3 + Pr2O3) / TREO x 100

(c) CaF2 calculated from fluorine assay using factor of 2.055 (F to CaF2). Assumes all fluorine is contained within the mineral fluorite ("fluorspar")

(d) Cut-off expressed as NMR ($)/t only considers payable elements La-Nd-Pr-Tb-Dy

(e) DyTb distribution calculated as (Dy2O3 + Tb2O3) / TREO x 100

(f) Prices shown are in CAD

(g) Differences may occur in totals due to rounding

The MRE confirms Ashram as a large, well-defined rare earth deposit with strong grade continuity and favourable metallurgical characteristics. The BD-Zone, also an REE-bearing unit, was excluded from the estimate pending further metallurgical evaluation and therefore represents additional resource upside.

Overall, the MRE provides a solid basis for advanced technical studies and future resource definition through continued drilling.

DEVELOPMENT PATHWAY

The updated PEA contemplates a mine and concentrator operation located at Ashram, with production of an intermediate mixed rare earth concentrate ("MREC") product for downstream processing.

The Project development strategy incorporates:

on-site concentration;

multi-modal logistics transportation;

hydrometallurgical processing in Saguenay;

production of saleable mixed rare earth products; and

future optionality for additional downstream processing initiatives.

The Company believes this approach:

materially improves execution certainty;

reduces development complexity;

enhances scalability;

supports financing pathways; and

aligns with broader Québecois and Canadian critical minerals strategies.

MINING

The Ashram Project mine design and mine plan are based on a conventional open-pit, truck-and-shovel operation using drill-and-blast mining on 10m benches, operated by an owner fleet on a continuous 7-day, 12-hour shift basis.

While the Mineral Resource supports a theoretical 169-year mine life at 4,900tpd, a 30-year life-of-mine (LOM) was adopted for the PEA as it captures most of the Project's value. Based on technical and economic parameters and metal selling prices, the Net Metal Return (NMR) cut-off for the Project was calculated at CAD$88/t.

A trade-off study assessing the impact of higher cut-off values on Project economics and concentrator feed quality resulted in the selection of an elevated cut-off strategy being adopted and an NMR cut-off of CAD$217/t was ultimately selected for the PEA.

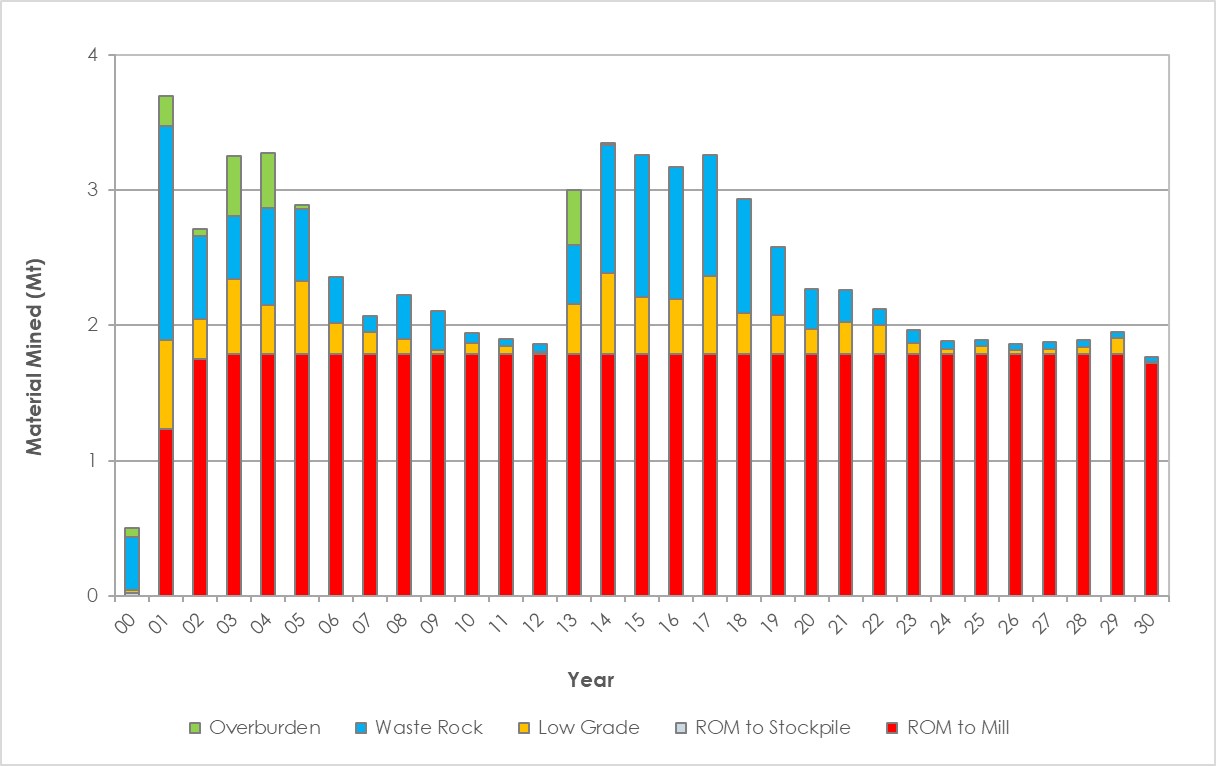

The resulting open pit design for the 30-year mine life includes 53 Mt of mill feed at a strip ratio of 0.4:1. Access to mineralisation beneath the shallow centre pond will require the construction of dewatering dykes and controlled pond dewatering. Mine design, scheduling and cost estimation were completed using MinePlan 3D software, supported by geological, topographical and material property data.

Of the approximately 53 Mt of mill feed underpinning the 30-year production target, approximately 93% is sourced from Indicated Mineral Resources and approximately 7% is sourced from Inferred Mineral Resources. There is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the determination of Indicated Mineral Resources or that the production target itself will be realised.

The mine plan has been sequenced such that Indicated Mineral Resources predominate in the early years of production, with Inferred Mineral Resources weighted towards the later stages of the mine life. The Company is satisfied that the respective proportions of Inferred Mineral Resources are not the determining factors in project viability and that Inferred Mineral Resources do not feature as a significant proportion early in the mine plan.

A phased mining approach was developed to prioritise higher-value material and manage technical risk, commencing with a starter pit that can be mined prior to the full dewatering of the centre pond from Year 2 to Year 3, followed by two deeper mining phases to a final pit depth of approximately 240m.

The mine plan targets steady-state production of 1.8Mtpa following a staged ramp-up, with average total material movement of 2.5Mtpa over the LOM. Waste rock, low-grade material and topsoil will be strategically stockpiled, with waste rock largely utilised for tailings dyke construction. Mining fleet requirements and workforce estimates underpin the mining cost model used in the PEA financial analysis.

Figure 6: Final Pit design

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_006full.jpg

Figure 7: Mine Production Schedule.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_007full.jpg

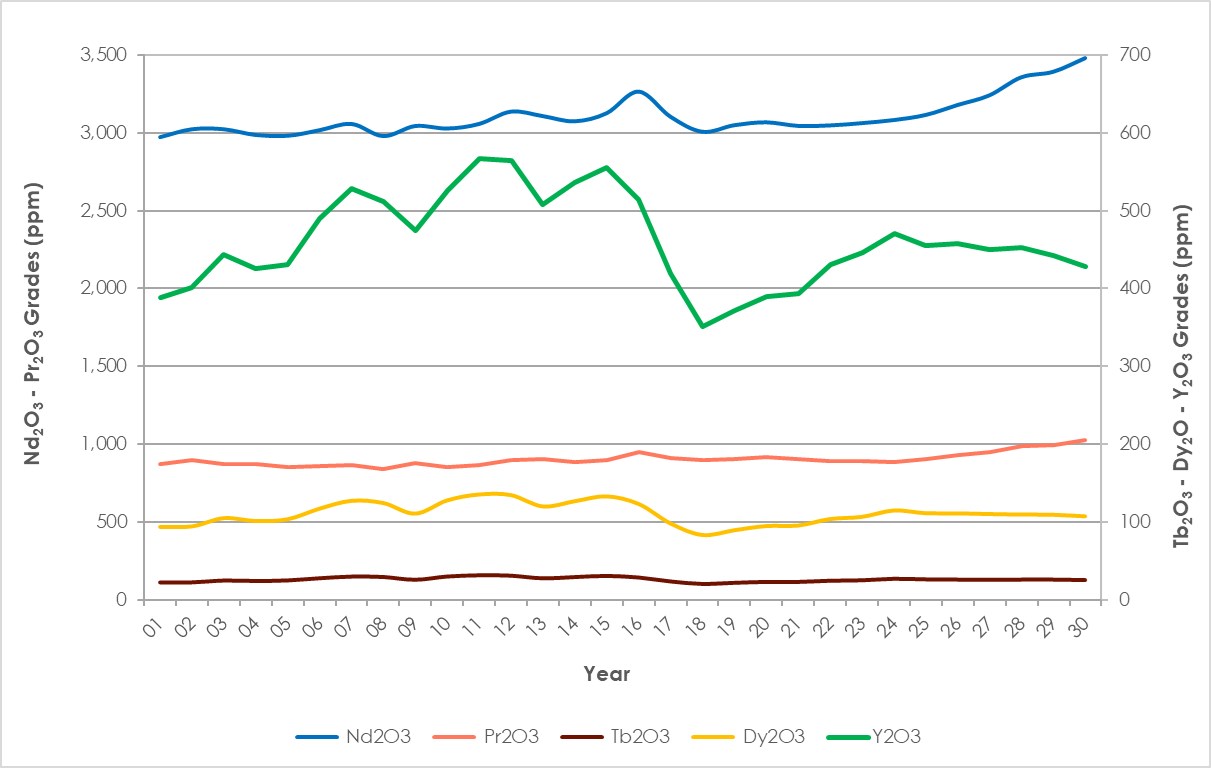

Figure 8: Crusher feed grades for five payable oxides.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_008full.jpg

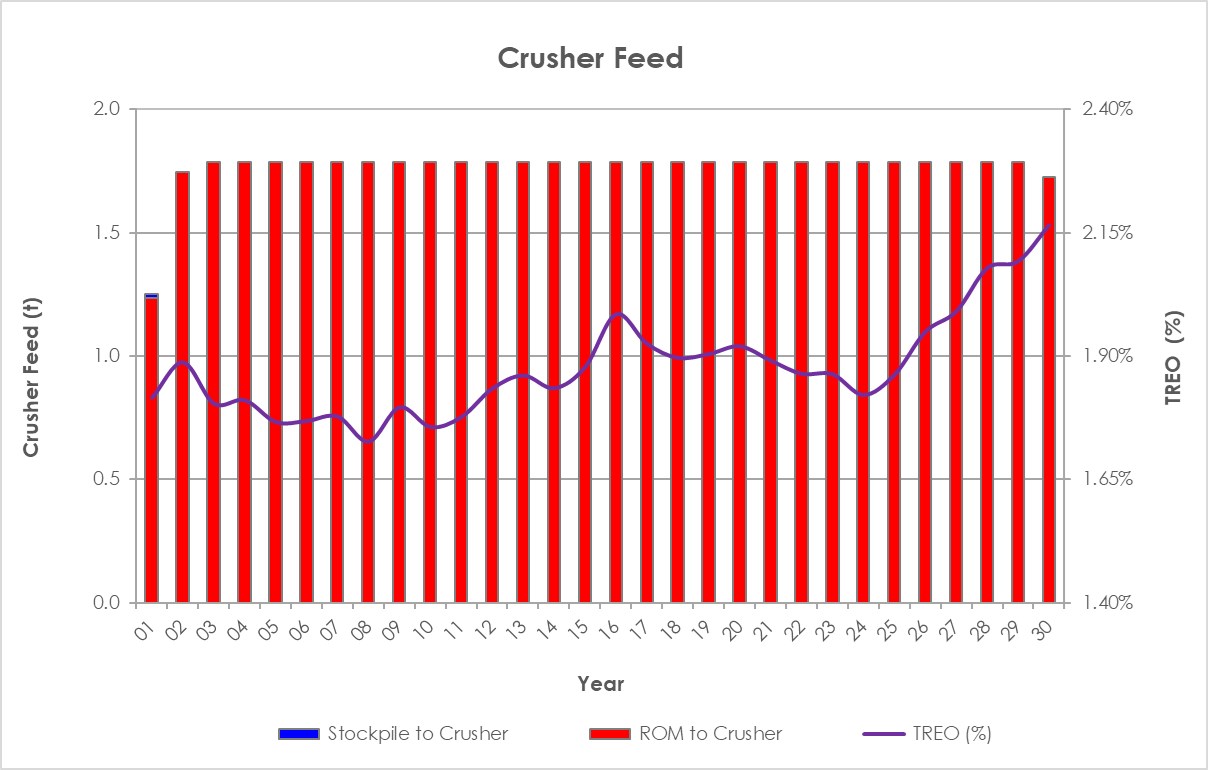

Figure 9: Crusher feed by year with contained TREO (%).

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_009full.jpg

METALLURGY AND PROCESSING

Minerals Processing Testing and Results

Several mineral processing test work programs have been completed for the Ashram Project to develop a beneficiation flowsheet capable of producing a rare earth mineral concentrate suitable for cost-effective hydrometallurgical processing.

The objectives of the various test work programs differed, with some focused on producing a high-grade mineral concentrate, while others investigated generating a lower-grade concentrate to maximise REE recovery and produce a fluorspar by-product.

The current beneficiation flowsheet strategy for REE processing is focused on producing a high-grade mineral concentrate to reduce the complexity and cost of downstream hydrometallurgical processing. This flowsheet does not consider fluorspar by-products.

Historical metallurgical test work campaigns were undertaken at UVR-FIA GmbH in Germany, Université Laval in Québec City, Canmet MINING in Ottawa, and Hazen Research Inc. in Colorado, USA. SGS Canada was subsequently engaged to investigate alternative flowsheets based on the historical work and the current project objectives.

SGS completed several test programs, including sample preparation, mineral characterisation, comminution testing, batch and locked-cycle flotation testing, and solid-liquid separation testing. The SGS work programs formed the basis for the process design criteria and support the production of high-grade rare earth mineral concentrates.

Hydrometallurgical Testing and Results

Extensive bench-scale and scoping metallurgical test work has been completed to evaluate hydrometallurgical recovery pathways for the Ashram flotation concentrate and support flowsheet selection for the PEA.

Early development work by Hazen (Gagnon et al., 2012) successfully demonstrated the production of commercial-grade mixed rare earth carbonate via a multi-step process incorporating pre-leaching, magnetic separation, sulphuric acid bake and water leach, selective thorium removal via solvent extraction, rare earth extraction and purification, oxalate precipitation, and metathesis to carbonate. High recoveries were achieved across most rare earth elements.

The flowsheet was subsequently simplified, optimised and validated through test work undertaken by L3 Process Development. Key processing steps were refined and de-risked, demonstrating effective gangue removal during pre-leach, strong and acid-efficient acid bake performance, and high water-leach recoveries. Thorium was completely and selectively extracted and recovered using Cyanex 923 without significant REE losses.

Additional scoping studies assessed alternative processing concepts, including high-activity direct hydrochloric acid leaching of flotation concentrates.

While it was successful on earlier flotation concentrates, this approach proved sub-optimal on concentrates generated under the latest flotation flowsheet conditions, reflecting changes in concentrate grade, mineralogy and impurity levels.

The cumulative test work confirms the technical robustness of the selected recovery flowsheet and highlights clear optimisation opportunities to be advanced during the Pre-Feasibility Study.

Table 4 shows the hydrometallurgical recoveries applied to monazite concentrates fed into the hydromet plant.

TABLE 4: Overall Hydrometallurgical Rare Earth Element Recoveries

| Element | Hydromet Recovery |

| Sc | 72% |

| Y | 78% |

| La | 77% |

| Ce | 83% |

| Pr | 91% |

| Nd | 91% |

| Sm | 84% |

| Eu | 84% |

| Gd | 84% |

| Tb | 78% |

| Dy | 78% |

| Ho | 78% |

| Er | 78% |

| Tm | 78% |

| Yb | 78% |

| Lu | 78% |

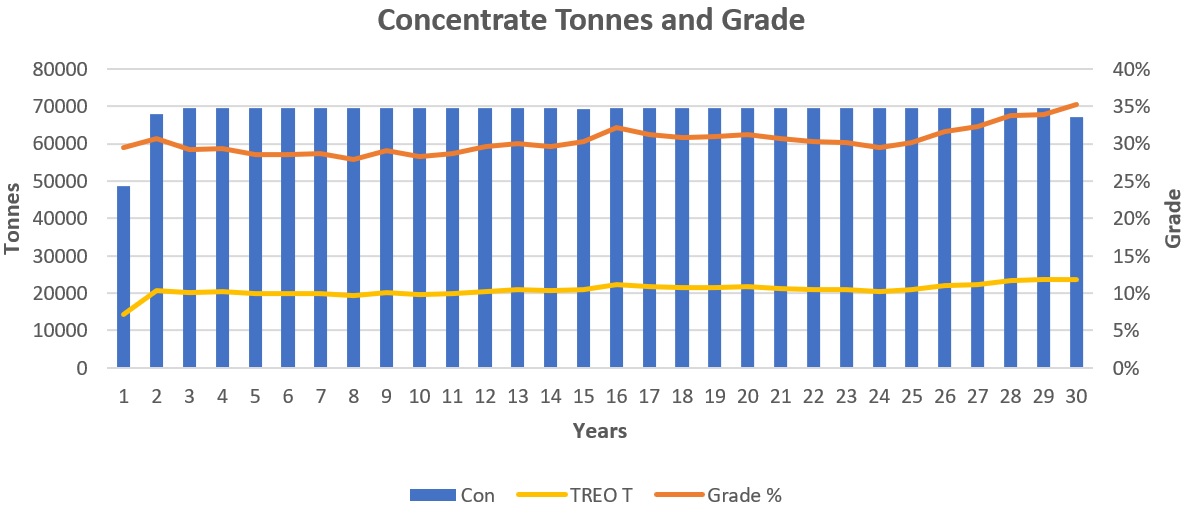

On-site Mineral Processing Facility

The Ashram Rare Earth Element Mineral Processing Facility ("MPF" or "concentrator") will be located immediately north of the open pit mine. The concentrator will comprise crushing, grinding, flotation and dewatering circuits.

The facility is designed to process nominal throughput of 4,900 dry tonnes per day (tpd) of run-of-mine (ROM) mineralised material at an average feed grade of 1.88% rare earth oxide ("REO"), producing approximately 190tpd of concentrate grading around 30% REO, varying between 28% and 34% depending on feed grade.

Figure 10: Concentrate tonnes and grade produced onsite at Ashram by year.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_figure11.jpg

The concentrator is designed to achieve an average REO recovery of 63% based on flotation test work, although recovery is expected to vary according to feed composition. Filtered concentrate will be loaded into 20-foot containers and transported south to the hydrometallurgical processing facility at Saguenay. Concentrator tailings, referred to as processed carbonatite, will be thickened and pumped to the processed carbonatite storage facility.

Figure 10 above shows concentrator tonnes and grades recovered onsite for shipment to Saguenay by years.

Hydrometallurgical Processing Facility

The hydrometallurgical processing facility, to be located in Saguenay, will upgrade flotation concentrate into a Mixed Rare Earth Carbonate (MREC) product using a proven process route incorporating acid bake, water leach, solvent extraction, oxalate precipitation and metathesis.

The hydromet plant is designed to process approximately 69,500tpa of flotation concentrate and produce approximately 33,800tpa of MREC, while ensuring effective removal and management of thorium and other impurities.

Process design is based on preliminary heat and material balance modelling and metallurgical test work, with individual circuit recoveries resulting in overall rare earth recoveries typically ranging from approximately 72% to more than 90%, depending on the element.

Comprehensive effluent treatment, scrubbing and reagent management systems have been incorporated to meet environmental and safety requirements.

Together, the concentrator and hydromet facilities form a technically robust recovery flowsheet that supports the Project's production targets and provides a clear pathway from mine feed to a marketable rare earth product at the PEA level.

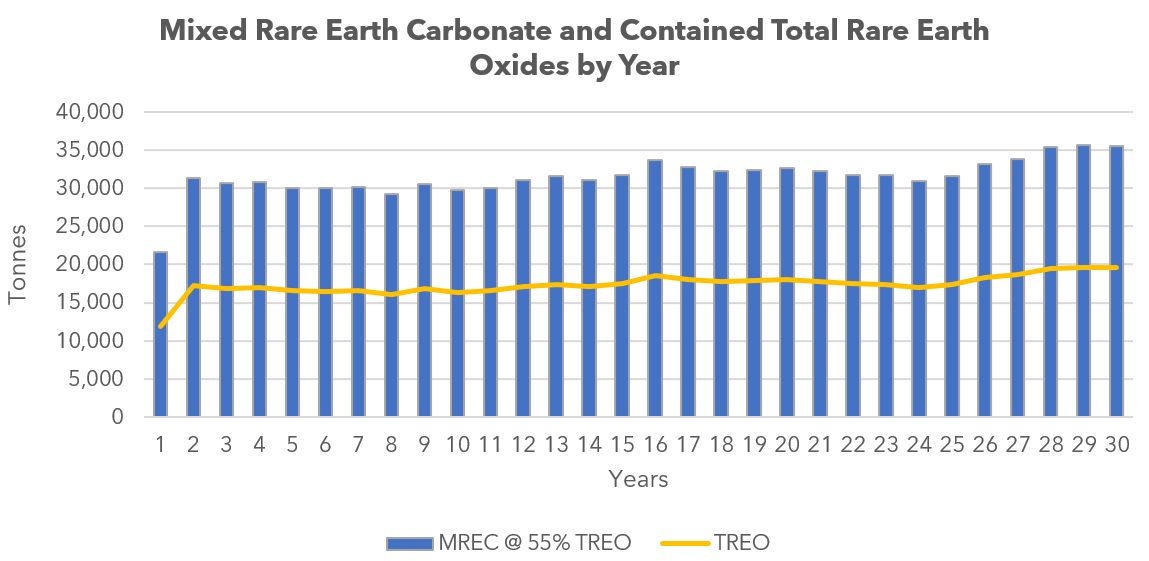

Figure 11: MREC production schedule (contained TREO).

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_figure12.jpg

INFRASTRUCTURE

The Ashram Project infrastructure strategy is underpinned by a comprehensive transport and logistics framework designed to support a remote mining operation with limited existing infrastructure and services in the surrounding region.

A 2025 transport route trade-off study identified a southern logistics corridor as the preferred development pathway. Under this scenario, concentrate would be transported via a 320km road link from Ashram to Schefferville, where it would connect to existing rail infrastructure for shipment to Sept-Îles. From there, containerised concentrate would be transported approximately 570km either by road or marine transport along the St. Lawrence River to Saguenay.

This intermodal logistics solution is designed to provide reliable, year-round transport while avoiding reliance on the previously considered northern shipping route, which would have required construction of new port infrastructure.

Transport logistics consider the naturally present thorium radionuclide content, which becomes concentrated during mineral processing on site at Ashram. The beneficiate concentrate will leave the Ashram mine-concentrator site as a class 7 material. During hydrometallurgical processing, thorium is expected to be concentrated into a separate, stable product (approximate 35% thorium oxide), while the final MREC product will contain very low thorium levels and is not expected to trigger radioactive transport regulations. The stable thorium-rich material will be transported separately to any other product or waste stream for disposal in Saskatoon in a third party approved and permitted radionuclide storage facility.

Supporting mine site infrastructure includes internal access roads, an aerodrome, diesel-based power generation, telecommunications systems, fuel storage, explosives facilities, and administrative and accommodation buildings for a workforce of up to 200 personnel.

Mont Royal is currently exploring options to share the infrastructure development with other local mining projects, government agencies, and First Nations.

At the downstream Saguenay site, additional non-process infrastructure will support concentrate handling, storage, and refining activities.

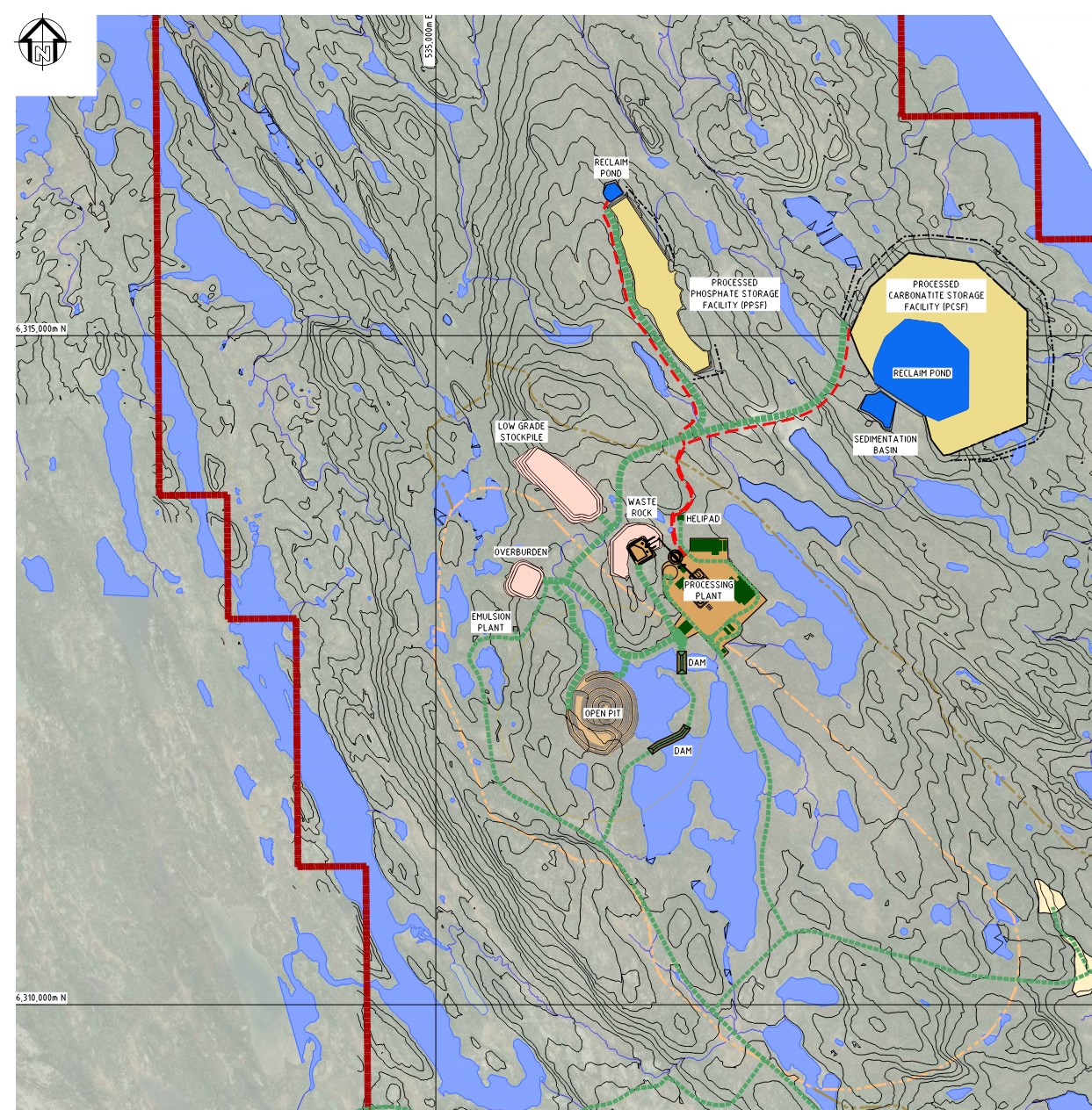

Figure 12: Ashram site general arrangement showing main infrastructure requirements including access roads.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_95e7c890d431a8a5_012full.jpg

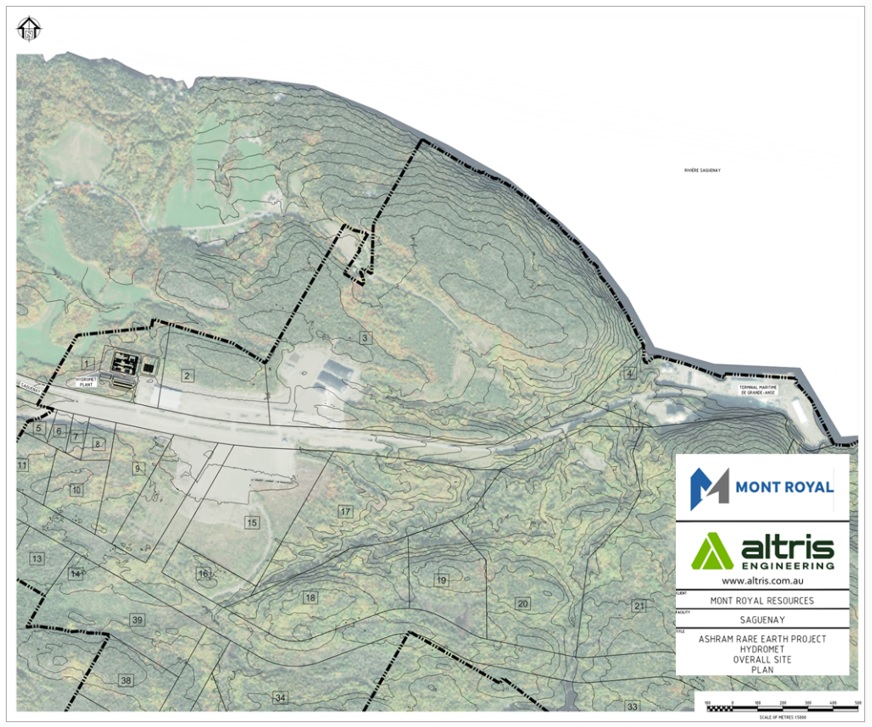

Figure 13: Hydromet facility footprint and plot selection in the Port of Saguenay industrial area.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/12033/300685_figure13.jpg

Processed mine waste will be managed through two on-site facilities: a large Processed Carbonatite Storage Facility (PCSF) and a smaller Processed Phosphate Storage Facility (PPSF). Hydromet waste is backhauled from Saguenay to Ashram. The PCSF is designed to store approximately 40Mm³ of flotation tailings using a staged centreline dam construction method, with decanted water recycled to support mill operations.

The PPSF has a planned capacity of approximately 2.5Mm³ and is proposed within a natural depression to minimise construction requirements. It is expected to store wet conventional gypsum-rich by-product or potentially dry-stacked gypsum-rich material, subject to further study.

Both facilities will incorporate seepage collection systems, water recirculation infrastructure and monitoring programs aligned with industry best practice and applicable regulatory guidance, including GISTM and Directive 019.

Site selection and design have prioritised minimising environmental disturbance, avoiding fish habitats, reducing dam heights and footprint, and maximising water reuse. Preliminary assessments indicate a "significant" consequence classification, subject to confirmation through future environmental and geotechnical investigations.

The site-wide water management strategy is designed to maximise water recycling, minimise freshwater intake and control environmental discharge. Runoff and seepage from waste facilities, stockpiles and the pit will be collected via ditches, sumps and ponds, then reused in processing where practical or treated prior to discharge.

The PCSF is a ring-based configuration designed to direct water away from the storage embankments towards a decant basin. The PCSF decant basin is sized to supply winter process water requirements, manage excess flows during spring freshet and summer conditions, and accommodate design flood events.

Two modular water treatment plants are proposed: one for solids removal, including overburden and lake dewatering water, and a second for metals and other contaminants, primarily from the ore stockpile and PPSF contact water, with additional capacity for seasonal excess flows.

Preliminary water balance modelling indicates sufficient recirculation capacity to sustain operations under normal conditions. Further studies are planned to refine hydrology, water quality, treatment requirements, including potential fluoride removal, and climate resilience considerations.

PERMITTING & APPROVALS

The Ashram REE Project is located in a sensitive northern environment in Nunavik, Québec, characterised by extensive surface water systems, boreal-tundra ecosystems, and the presence of Inuit, Naskapi and Innu communities with established land rights.

Environmental baseline data remains limited and is largely based on studies completed between 2011 and 2013, highlighting the need for updated and expanded environmental programs to support future ESIA and permitting activities.

Preliminary studies indicate generally low acid rock drainage risk, although there remains potential for localised metal and fluoride leaching that will require further assessment. Project design, environmental management strategies and closure concepts remain at a conceptual stage and will be refined during future study phases.

The Project is subject to a complex regulatory framework, including federal impact assessment requirements and Québec provincial processes under the James Bay and Northern Québec Agreement and the Environment Quality Act.

Permitting will cover the mine, associated infrastructure, concentrate transport corridor and hydrometallurgical processing facility, with approvals required across environmental, water, wildlife and industrial regulations and is expected to take several years to complete.

Early stakeholder engagement has commenced, including agreements and consultation with Inuit, Naskapi and Innu groups. Ongoing engagement is expected to play an important role in project development, particularly in relation to infrastructure planning, environmental protection and Indigenous participation.

Preliminary closure and rehabilitation planning is focused on achieving long-term environmental stability, public safety and progressive land restoration. Current concepts include natural flooding of the open pit, infrastructure removal, revegetation and ongoing water management until discharge criteria are achieved. The total estimated closure costs for both sites is CAD$74M.

Further technical studies, stakeholder input and regulatory engagement will be required to refine closure strategies and support compliance with evolving environmental and social expectations.

MARKET POSITION

Global rare earth markets are increasingly being shaped by supply chain security concerns, electrification trends, defence requirements, energy transition demand and Western government critical minerals policies. China currently dominates global rare earth refining and magnet manufacturing capacity, increasing the urgency among Western governments and industry participants to establish alternative supply chains.

Ashram is well positioned in this environment due to its jurisdiction, scale, mineralogy, product basket, logistical advantages and development optionality.

The Ashram Project is well positioned to supply high-value magnet rare earth elements (Nd, Pr, Dy and Tb) into a market expected to experience strong structural deficits, particularly for Dy and Tb.

The global REE supply chain remains heavily dominated by China, which accounted for approximately 77% of global mine production and ~90% of separation capacity in 2025, while non-Chinese supply remains limited.

Ashram is a large-scale, monazite-dominant carbonatite deposit located in Québec, Canada, a Tier-1 mining jurisdiction. The Project demonstrates high NdPr content, significant Tb and Dy distribution, and potential fluorspar by-product credits.

Its monazite-dominant mineralogy, including an approximately 21% NdPr distribution, positions Ashram to supply meaningful volumes of high-value magnet feedstock into Western markets.

Demand for magnet REEs is projected to grow at a CAGR of 8-12% through to 2050, driven by electric vehicles, wind turbines, robotics and defence applications.

The PEA economics were based on long-term pricing forecasts from Adamas Intelligence (Q1 2026, updated Q2 2026). No off-take agreements are currently in place.

The Project's proposed high-purity mixed rare earth carbonate (MREC) product is considered suitable for processing by North American and European separation facilities.

Pricing assumptions for the PEA were based on Adamas Intelligence's Rare Earth Pricing Quarterly Outlook, with yearly forecast prices applied for the period 2026-2040 and 2040 pricing estimates carried forward for the remainder of the mine life due to the increasing uncertainty associated with long-term forecasts beyond that period.

TABLE 5: REE oxide price forecast (US $/kg)

| Oxide | 2026 Q2 | 2026-2030 average | 2031-2035 average |

| Pr2O3 (2N5) | 125.93 | 125.93 | 174.01 |

| Nd2O3 (2N5) | 125.00 | 125.00 | 172.73 |

| Sm2O3 (3N) | 12.00 | 13.60 | 12.00 |

| Eu2O3 (5N) | 26.50 | 29.50 | 34.40 |

| Gd2O3 (2N5) | 43.00 | 50.60 | 76.00 |

| Tb2O3 (4N) | 1700.00 | 1940.00 | 1950.40 |

| Dy2O3 (2N5) | 420.00 | 484.00 | 517.60 |

| Ho2O3 (2N5) | 83.70 | 112.07 | 175.22 |

| Er2O3 (2N5) | 50.00 | 54.60 | 58.00 |

| Yb2O3 (4N) | 13.25 | 14.10 | 15.50 |

| Lu2O3 (4N) | 1250.00 | 1250.00 | 1250.00 |

| Y2O3 (5N) | 35.00 | 33.00 | 22.00 |

Source: Adamas Intelligence, Rare Earth Pricing Outlook Quarterly, Q2 2026.

a) La and Ce not considered as payable elements in the economic assessment

ECONOMIC ANALYSIS

Capital Expenditure (CAPEX)

Capital costs were divided into four categories: initial, sustaining, closure and post-closure. The initial capital costs are phased over two years of construction, with sustaining capital costs phased evenly over the 30-year life of the Project. Sustaining capital costs include all expenditures necessary to sustain operations throughout the life-of-mine.

Closure costs are phased in Year 31, with post-closure costs phased over seven years of monitoring post-closure. Cumulative Life-of-Mine (LOM) capital expenditures including all phases, and including contingency was estimated at CAD$1,605M.

TABLE 6: Capital cost estimate summary by phase and area

| Area | Capital costs (CAD$M) | ||||

| Initial | Sustaining | Closure | Post-closure | Total | |

| Ashram Mine | 18 | 17 | - | - | 35 |

| Ashram Concentrator | 295 | - | - | - | 295 |

| Ashram Non-Processing Infrastructure | 192 | - | - | - | 192 |

| Ashram Tailings Storage | 23 | 210 | - | - | 232 |

| Ashram Tailings - Hydromet Cell | 4 | 4 | - | - | 8 |

| Ashram Site Water Management | 15 | - | - | - | 15 |

| Ashram Site Water Treatment | 7 | - | - | - | 7 |

| Saguenay Hydrometallurgical Refinery | 358 | - | - | - | 358 |

| Saguenay Non-Processing Infrastructure | 32 | - | - | - | 32 |

| Saguenay Site Water Treatment | 5 | - | - | - | 5 |

| Closure | - | - | 51 | 7 | 57 |

| Contingency (30%) | 284 | 69 | 15 | 2 | 370 |

| Total | 1231 | 299 | 66 | 9 | 1605 |

The Project is anticipated to qualify for the Clean Technology Manufacturing Investment Tax Credit (CTM ITC), enacted under section 127.49 of the Income Tax Act (Canada). $342M in refundable tax credits are anticipated and have been included in the post-tax cashflows in the financial model.

The overall capital cost estimate developed in this Preliminary Economic Assessment Study meets the AACE Class 5 requirements and has an accuracy range of between ±50%. The costs include Direct and Indirect capital cost estimates.

Operating Expenditures (OPEX)

The operating cost estimate is based on a combination of experience, reference project, budgetary quotes, and factors as appropriate with a preliminary study. No cost escalation or contingency has been included within the operating cost estimate. The average annual operating cost was estimated at CAD$306M, and total LOM operating cost was estimated at CAD$9,178M.

Production ramp-up profiles were developed for both the mine concentrator and refinery and achieves steady state at nameplate capacity for each facility by Year 3 (concentrator) and Year 4 (refinery).

The notional capital cost of the access road (~CAD$684M on a standalone basis) has been converted into an equivalent usage charge within operating costs for the PEA, consistent with a third-party infrastructure access model. This approach reflects a scenario where the Project will pay a tariff for road usage rather than incurring full upfront construction capital.

While no formal infrastructure agreements are currently in place, the Company notes that shared infrastructure development is common in northern Canadian jurisdictions and is supported by both provincial and federal critical minerals strategies. The Company will continue to advance discussions to support this development pathway.

Sensitivity analysis indicates that the Project remains economically robust under a range of infrastructure funding scenarios; however, changes to the assumed infrastructure ownership model may impact capital intensity and project returns.

TABLE 7: Operating cost estimate summary by area

| Area | Per Avg Operating Year (CAD M, real) | CAD/t ore processed | CAD/kg REO | LOM (CAD M, real) |

| Mining | 22 | 12.29 | 1.28 | 652 |

| Processing - Concentrator | 120 | 67.89 | 7.06 | 3,599 |

| Processing - Hydrometallurgy | 72 | 40.55 | 4.21 | 2,149 |

| General & Administrative* | 83 | 46.84 | 4.87 | 2,483 |

| Tailings management | 5 | 2.73 | 0.28 | 145 |

| Owner's cost | 4 | 2.06 | 0.21 | 109 |

| Waste Water Treatment | 1 | 0.78 | 0.08 | 42 |

| Total | 306 | 173.13 | 18.00 | 9,178 |

*General & Administrative costs include: concentrate transport, waste material transport, access road costs, flights and accommodation at the Ashram mine-concentrator site, etc

Funding Assumptions

The PEA contemplates initial capital expenditure of approximately CAD$1.23 billion (excluding access road, including 30% contingency) and total life-of-mine capital expenditure of approximately CAD$1.605 billion.

The Company intends to continue development funding discussions through the course of the impending PFS and further studies to strengthen the potential of investment from both government agencies and strategic groups that have already expressed interest in the project given the scale and strategic importance. Funding of the Project through a combination of equity capital markets, debt financing, government grants and incentives (including applicable Canadian and Québecois critical minerals programs), strategic partnerships, and/or joint venture arrangements, subject to market conditions and the outcomes of further feasibility studies are all sources of credible financing streams that will be progressed by the Company.

During the past 12 months, the Canadian government has announced several significant funding schemes for the development of critical minerals projects of geopolitical and strategic importance, with rare earths being one of the highlighted commodities. The Company will continue to engage with these entities to advance the potential for gaining investment and assurance for its ongoing project development strategy.

There is no certainty that the Company will be able to raise the required funding on acceptable terms or at all. If equity funding is required, this may be dilutive to existing shareholders. The Company may also consider alternative value realisation strategies, including a partial or full sale of the Project or the introduction of a joint venture partner, which could materially reduce the Company's proportionate ownership of the Project.

The assumptions regarding funding availability are based on the Company's assessment of current capital markets conditions, the strategic importance of critical minerals supply chains, and the Company's ongoing engagement with potential strategic and financial partners. While the Company believes it has a reasonable basis for the funding assumptions contained in the PEA, investors should note that these assumptions may not prove to be correct and that the availability of funding on acceptable terms is subject to significant uncertainty.

Financial Metrics and outputs

A Preliminary Economic Assessment has been prepared to determine the economic viability of the Project at scoping-study level.

The base case PEA has a 2-year construction period (exclusive of road construction) followed by 30 years of production, processing ore through a flotation concentrator to produce a beneficiated concentrate, which is transported to the hydrometallurgical refinery and converted into a saleable Mixed Rare Earth Carbonate (MREC).

The Project is designed to produce an average* 17,466 tonnes per annum of saleable REO, including 4,035 tonnes per annum of NdPr. Initial capital cost is estimated at CAD$1,231M (including 30% contingency).

At a real basket price of CAD$44.40 per kilogram of saleable REO, the Project generates life-of-mine revenue of CAD$24,638M, life-of-mine EBITDA of CAD$15,460M (62.7% margin) and undiscounted post-tax cash flow of CAD$8,365M.

As shown in Table 9, the project metrics are robust, with post-tax NPV at an 8% real discount rate of CAD$2,026M, post-tax IRR of 22.0% and payback from start of production of 3.9 years. Pre-tax NPV at 8% real is CAD$3,440M and pre-tax IRR is 25.6%. Average C1 cash cost over LOM is CAD$17.99 per kilogram saleable REO and average LOM all-in sustaining cost is CAD$18.58 per kilogram saleable REO. The economic analysis indicates that the Project is technically viable on a stand-alone basis and supports advancement to Pre-Feasibility Study.

The Project is subject to the standard Canadian federal and Québec provincial taxation regime applicable to mining operations, together with Québec-specific mining duties.

Corporate income tax on chargeable income from the Project has been applied at the following rates:

- Federal corporate income tax: 15.0% on taxable income.

- Québec provincial corporate income tax: 11.5% on taxable income.

- Combined statutory income tax rate: 26.5%.

The corporate tax rate is applied to profits after allowances for all cash operating expenses and capital depreciation. All expenses incurred during operations are assumed to be tax deductible, with capital costs depreciable. Prior year tax losses are accumulated and used to offset tax payments in future years.

A series of sensitivity analyses has been performed to determine the impact on NPV 8%, post-tax (real) of changes in the principal economic assumptions. Each variable has been flexed ±30% from base case.

The variables tested are:

- REO basket price (±30%).

- Overall recovery (±30%).

- Initial capital cost (±30%).

- Operating cost (±30%).

- Payability factor (±30%).

- Diesel fuel price (±30%).

Single variable sensitivity results are presented in Table 8.

The project is most sensitive to changes in revenue-side assumptions. REO basket price, recovery and payability factors are equivalent in a single variable framework, each multiplying directly into Project revenue.

Table 8: Project Sensitivities on post Tax NPV8%, (Cad $M)

| REO Basket Price / Recovery / Payability | ||||||

| -30% | -20% | -10% | 0% | 10% | 20% | 30% |

| 667 | 1,129 | 1,580 | 2,026 | 2,469 | 2,912 | 3,354 |

| Operating Cost | ||||||

| -30% | -20% | -10% | 0% | 10% | 20% | 30% |

| 2,518 | 2,355 | 2,190 | 2,026 | 1,861 | 1,693 | 1,522 |

| Initial Capital Cost | ||||||

| -30% | -20% | -10% | 0% | 10% | 20% | 30% |

| 2,220 | 2,155 | 2,091 | 2,026 | 1,962 | 1,896 | 1,830 |

| Diesel Fuel Price | ||||||

| -30% | -20% | -10% | 0% | 10% | 20% | 30% |

| 2,030 | 2,029 | 2,028 | 2,026 | 2,025 | 2,024 | 2,022 |

| Discount rate | ||||||

| 5% | 8% | 10% | 15% | |||

| 3,363 | 2,026 | 1,448 | 577 | |||

TABLE 9: Project outcomes summary

| Parameter | Unit | Value |

| Production Profile | ||

| Construction period | years | 2 |

| Production life | years | 30 |

| Mill throughput (nameplate) | Ktpa | 1,788 |

| Average head grade | % TREO | 1.88% |

| Overall TREO recovery (inc. ramp up) | % | 51.3% |

| Annual saleable REO production | tpa | 17,466* |

| Annual NdPr production | tpa | 4,035* |

| LOM saleable REO | t | 510,000 |

| Economic Results | ||

| LOM revenue | CAD M | 24,638 |

| LOM EBITDA | CAD M | 15,460 |

| LOM EBITDA margin | % | 62.7% |

| LOM undiscounted post-tax cashflow | CAD M | 8,365 |

| NPV 8% post-tax (real) | CAD M | 2,026 |

| NPV 8% pre-tax (real) | CAD M | 3,440 |

| IRR post-tax (real) | % | 22.0% |

| IRR pre-tax (real) | % | 25.6% |

| Payback from start of production (post-tax) | years | 3.9 |

| Unit Costs | ||

| C1 cash cost | CAD/kg saleable REO | 17.99 |

| All-in sustaining cost (AISC) | CAD/kg saleable REO | 18.58 |

*Average output excluding ramp-up

FORWARD WORK PROGRAM

Based on the strong outcomes of the updated PEA, the Company intends to progress to higher level feasibility studies and scale-up test work activities. These include, but are not limited to:

- Pre-Feasibility Study (PFS) for the Ashram Project to commence in the second half of CY2026.

- Permitting and baseline studies for the Ashram and Saguenay sites.

- Metallurgical test work for potential inclusion of Fluorspar recovery circuit in future Ashram flowsheets.

- BD-Zone test work and potential MRE inclusion.

- Ongoing optimisation of Ashram site power costs and initiatives to reduce these through renewable energy initiatives.

In addition, Mont Royal will also collaborate with industry to assess potential opportunities to capture additional value along the rare earth oxide and magnet supply chain.

For and on behalf of the Board

ENDS

Joel Ives | Company Secretary

| For Further Information: Nicholas Holthouse Managing Director info@montroyalres.com | Peter Ruse Corporate Development info@montroyalres.com | Nicholas Read Investor and Media Relations nicholas@readcorporate.com.au |

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

About Mont Royal Resources

Mont Royal Resources Limited (ASX: MRZ) (TSXV:MRZL) is a critical minerals development and exploration company with projects in Quebec, Canada. The Company is dedicated to advancing its 100%-owned Ashram Rare Earth and Fluorspar Deposit in Québec, Canada - one of the largest monazite-dominant carbonatite-hosted Rare Earth Elements deposits in North America.

In addition, the Company owns 75% of Northern Lights Minerals 536km2 tenement package located in the Upper Eastmain Greenstone belt. These projects are in the emerging James Bay area, a Tier-1 mining jurisdiction of Quebec, and are prospective for lithium, precious (Gold, Silver) and base metals mineralisation (Copper, Nickel).

For further information regarding Mont Royal Resources Limited, please visit the ASX platform (ASX: MRZ) or the Mont Royal's website www.montroyalres.com.

Competent Persons

The estimated Mineral Resources underpinning the production target have been prepared by a Competent Person in accordance with the requirements of the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (JORC Code). The Mineral Resource Estimate for the Ashram Rare Earth Elements and Fluorspar Deposit, Nunavik, Quebec, Canada (Ashram Project) was first reported in in the Company's replacement prospectus dated 30 September 2025 and released to ASX on 1 October 2025 (Prospectus). The Company confirms that it is not aware of any new information or data that materially affects the information relating to the estimate included in the Prospectus and that all material assumptions and technical parameters underpinning the estimate in the Prospectus continue to apply and have not materially changed.

Qualified Persons

The NI 43 101 technical report was prepared by Qualified Persons in accordance with the National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43 101") and the Canadian Institute of Mining, Metallurgy, and Petroleum (CIM, 2014) Definitions and Standards for Mineral Resources and Reserves.

The following individuals, by virtue of their education, experience and professional association, are considered QPs as defined in NI 43-101, and are members in good standing of appropriate professional institutions. Table 10 outlines the responsibilities for the various sections of the Report and the name of the corresponding Qualified Person.

Table 10: Qualified Persons contributing to the NI 43 101 Technical Report.

| Name | Organisation | Scope area |

| Lucas Bullen, CPEng., CEng. | Altris Engineering | Opex /Capex estimates; General and Administration, process infrastructure and overall project coordination |

| Jeffrey Cassoff, P.Eng. | BBA Inc. (BBA) | Mine design and mine planning; Opex / Capex estimates for mining |

| Colin Hardie, P.Eng. | BBA Inc. (BBA) | Environmental; Financial Analysis, Overall report integration |

| Pierre-Luc Richard, P.Geo, M.Sc. | PLR Resources Inc. (PLR) | Geology and Mineral Resource Estimate |

| Jordan Zampini, P.Eng. | DRA Americas Inc. (DRA) | Concentrator; Opex and Capex for concentration |

| Tommee Larochelle, PE, P.Eng., MBA, PhD | L3 Process Development (L3) | Hydrometallurgical processing, market analysis; Opex and Capex for hydrometallurgical refining |

| Christian Dubé, PMP, ing., P.Eng. | ASDR Canada Inc. | Water treatment; Opex and Capex for water treatment and infrastructure |

| Thomas Lépine, ing., P.Eng. | TALA Geotec | Processed carbonatite and processed phosphate waste facilities; Opex/Capex for processed waste facilities and water management infrastructure |

| David Sims, P.Geo (B.C.), Géo (QC), P.Geo (ON) | Norda Stelo | Processed carbonatite and processed phosphate waste facilities, site water management and balance |

Important Notices & Disclaimers

Forward-looking Statements

This announcement contains certain "forward-looking statements" within the meaning of Australian securities laws and "forward-looking information" within the meaning of Canadian securities laws (collectively referred to as "forward-looking statements"). All statements, other than statements of historical fact, that address circumstances, events, activities or developments that could, or may or will occur are forward-looking statements. These forward-looking statements are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking information. Risks that could change or prevent these events, activities or developments from coming to fruition include: actual results of current and future exploration activities; that Mont Royal may not be able to fully finance any additional exploration on the Ashram Project; that even if Mont Royal is able raise capital, costs for exploration activities may increase such that Mont Royal may not have sufficient funds to pay for such exploration or processing activities; the timing and content of the proposed drill program and any future work programs may not be completed as proposed or at all; geological interpretations based on drilling that may change with more detailed information; potential process methods and mineral recoveries assumptions based on limited test work and by comparison to what are considered analogous deposits that, with further test work, may not be comparable; testing of our process may not prove successful or samples derived from the Ashram Project may not yield positive results, and even if such tests are successful or initial sample results are positive, the economic and other outcomes may not be as expected; the anticipated market demand for rare earth elements and other minerals may not be as expected; the availability of labour and equipment to undertake future exploration work and testing activities; geopolitical risks which may result in market and economic instability; and despite the current expected viability of the Ashram Project, conditions changing such that even if metals or minerals are discovered on the Ashram Project, the project may not be commercially viable, or other risks detailed herein and from time to time in the public filings made by Mont Royal. Although Mont Royal has attempted to identify important factors that could cause actual actions, events or results to differ from those described in forward-looking statements, there may be other factors that cause such actions, events or results to differ materially from those anticipated. These forward-looking statements are based on Mont Royal's current expectations, estimates, forecasts and projections about its business and the industry in which it operates and management's beliefs and assumptions, including the non-occurrence of the risks and uncertainties that are described above and in the public filings made by Mont Royal or other events occurring outside of our normal course of business, and are not guarantees of future performance or development and involve known and unknown risks, uncertainties and other factors that are in some cases beyond Mont Royal's control.

Forward-looking statements in this announcement include, but are not limited to; the plans, operations and prospects of Mont Royal and its properties; the continued advancement of the Ashram Project to development; that Ashram's fluorspar component which makes it one of the largest potential sources of fluorspar in the world and could be a long-term supplier to the met-spar and acid-spar markets; that Mont Royal is positioning to be one of the lowest cost rare earth element producers globally, with a focus on being a long-term global supplier of mixed rare earth carbonate and/or NdPr oxide; and that Mont Royal may explore the potential of other high-value commodities on the Ashram Property and the expected timetable for dual listing of Mont Royal's shares; and statements about market and industry trends, which are based on interpretation of market conditions. Forward-looking statements can generally be identified by the use of forward-looking words such as "anticipate", "expect", "likely", "propose", "will", "intend", "should", "could", "may", "believe", "forecast", "estimate", "target", "outlook", "guidance" (including negative or grammatical variations) and other similar expressions. No representation, warranty, guarantee or assurance, express or implied, is given or made in relation to any forward-looking statement. In particular no representation, warranty or assumption, express or implied, is given in relation to any underlying assumption or that any forward-looking statement will be achieved. There can be no assurance that the forward-looking statements will prove to be accurate. Actual and future events may vary materially from the forward-looking statements and the assumptions on which the forward-looking statements were based, because events and actual circumstances frequently do not occur as forecast and future results are subject to known and unknown risks such as changes in market conditions and regulations.

Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements, and should rely on their own independent enquiries, investigations and advice regarding information contained in this announcement. Any reliance by a reader on the information contained in this announcement is wholly at the reader's own risk.

To the maximum extent permitted by law or any relevant listing rules of the ASX/TSX-V, Mont Royal and their respective related bodies corporate and affiliates and their respective directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to disseminate any updates or revisions to the information in this announcement to reflect any change in expectations in relation to any forward-looking statements or any such change in events, conditions or circumstances on which any such statements were based. Nothing in this announcement will, under any circumstances (including by reason of this announcement remaining available and not being superseded or replaced by any other announcement or publication with respect to Mont Royal or the subject matter of this announcement), create an implication that there has been no change in the affairs of Mont Royal since the date of this announcement.

Not Investment Advice

This announcement is not financial product, investment advice or a recommendation to acquire securities of Mont Royal or Commerce and has been prepared without taking into account the objectives, financial situation or needs of individuals. Each recipient of this announcement should make its own enquiries and investigations regarding all information in this announcement, including, but not limited to, the assumption, uncertainty and contingencies which may affect future operations of Mont Royal and the impact that different future outcomes may have on Mont Royal. Before making an investment decision, prospective investors should consider the appropriateness of the information having regard to their own objectives, financial situation and needs, and seek legal, taxation and financial advice appropriate to their jurisdiction and circumstances.

Unless otherwise stated, all dollar values in this Announcement are reported in Canadian dollars.

1 There is a low level of geological confidence associated with Inferred Mineral Resources and there is no certainty that further exploration work will result in the determination of Indicated Mineral Resources or that the production target itself will be realised. Refer to the cautionary statement on page 1 of this announcement for further details.

![]()

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/300685