When someone mentioned buying a game boost five years ago, the conversation usually came with a disclaimer. It happened quietly, in private Discord servers, and rarely surfaced in communities where any form of assistance was treated as a personal failure. In 2026 that framing has collapsed. Boosting now operates in the open, supported by platforms, escrow payments and customer service that would look ordinary in any other online marketplace. This is an analysis of how a service that once lived at the margins moved to the centre — and why the conditions that created it are structural, not temporary.

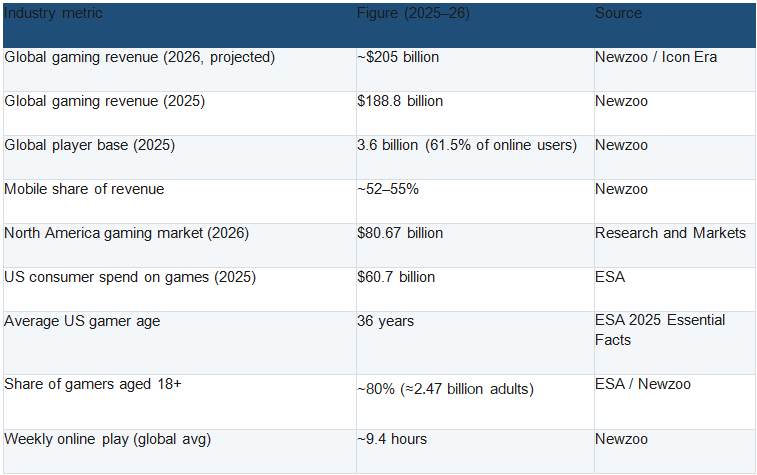

The starting point is scale. The global games market is on track for roughly $205 billion in revenue in 2026 (link https://icon-era.com/statistics/video-game-statistics/ ), up from $188.8 billion in 2025, with about 3.6 billion players worldwide — more than 60% of everyone online. A market that large, attached to an audience that broad, inevitably generates demand for services around it. The table below sets the stage.

The Numbers That Set the Stage

These figures matter because they describe the conditions a boosting market needs to exist. An audience of 3.6 billion, skewing adult and spending freely, produces an enormous population of players who want high-level content but are blocked by time, skill, or both. Boosting lives precisely in that gap — and three structural drivers have widened it.

Why Boosting Became an Industry: Three Structural Drivers

1. The audience got massive — and older — with money to spend

The defining demographic fact of gaming in 2026 is age. The average US player is now 36, roughly 80% of gamers are adults, and the single largest global segment is players aged 25–34. This is not a teenage hobby anymore; it is a mainstream adult pastime carried by people with careers, families and disposable income. Console and PC players in their thirties and forties still log close to ten hours a week, but those hours now compete with mortgages, children and jobs.

That changes how players think about time. A professional who values an hour at a real hourly rate evaluates a six-hour pickup raid differently than a student with an open weekend. For this player, paying for a two-hour carry is not morally distinct from paying for food delivery, cleaning or transport — it is the same trade: money for hours spent on a task that falls within their ability but below the priority of their time. As the median gamer aged, this framing became the dominant one.

Boosting is not a teenager's shortcut anymore. It is an adult's time-saving purchase — and the median gamer in 2026 is a time-constrained adult.

2. Live-service design manufactures time-gated demand

The second driver is built into how modern games are made. Live-service titles never end. Their content refreshes on a four-to-eight-week cycle, rewards are increasingly time-limited, and falling behind a season carries a real competitive and social cost. The question stopped being “have you finished the game?” and became “are you current with the season?” — a question that resets perpetually.

World of Warcraft: Midnight, which launched on March 2, 2026 and anchors the single largest segment of the carry market, illustrates the design perfectly. Its first season ships three raids across nine bosses, eight Mythic+ dungeons, the new Prey hunting system across three difficulties, and a perpetual cadence of seasonal goals — all gated behind coordinated, time-intensive play. Each patch produces a fresh wave of players who want to keep pace without quitting their jobs, which is exactly why demand for a WoW boost consistently forms one of the largest slices of the entire market. The treadmill is the product, and the treadmill never stops.

3. Supply professionalized into a real service industry

The third driver is on the supply side. The serious operators stopped resembling lone sellers and started resembling service businesses — with vetted players, secure handling, defined deliverables, published refund policies and verified review profiles. Crucially, the market shifted away from account-sharing toward self-play and duo formats, where the customer keeps control of their account and the booster simply joins them. A modern platform such as XBoosty competes less on raw price and more on this trust infrastructure, covering multiple titles under one accountable provider relationship.

This professionalization is the part outsiders miss. The reputation of boosting was set during its chaotic early years, but the category that exists in 2026 has far more in common with freelance marketplaces and digital-service platforms than with the back-alley image it inherited.

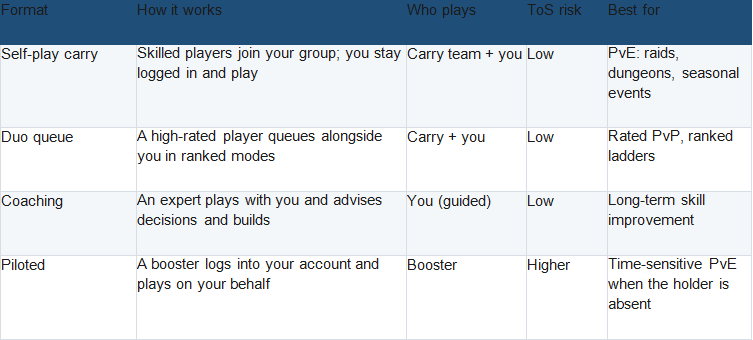

What the Modern Market Looks Like: Four Service Formats

The market is not monolithic. In 2026 it organizes around four primary formats, each with a distinct method and risk profile. The shift toward self-play and duo queue — rather than account-sharing — is itself a sign of an industry maturing toward consumer-grade norms.

Service formats and relative ToS risk, 2026. Self-play and duo queue have become the market default.

Where Demand Concentrates in 2026

Demand is not spread evenly. It clusters around titles that share three traits: a heavy time investment to reach endgame, a large active player base, and content that gates desirable rewards behind coordinated performance. Four titles dominate the 2026 picture:

World of Warcraft: Midnight — the largest segment by volume, driven by Mythic+, raid progression and seasonal PvP titles. ARC Raiders — 2026's breakout extraction shooter, whose recurring seasonal events create monthly demand spikes. Diablo 4 — whose roughly three-month seasons reset progression and concentrate demand in each season's opening weeks. Path of Exile 2 — whose league economy makes early-season progression economically valuable, a time-pressure unique to the ARPG genre.

Why the Trajectory Points Up, Not Down

None of the three drivers is reversing. The audience keeps aging into higher incomes and tighter schedules. Live-service design keeps multiplying time-limited rewards. And the supply side keeps professionalizing, which lowers perceived risk and pulls in buyers who would never have touched an anonymous Discord seller. The cultural shift compounds the trend: what was once whispered about is now discussed openly on mainstream forums, and established providers operate with the same trust signals — reviews, refunds, support — that buyers expect from any other service.

The honest conclusion is not that boosting is universally embraced; plenty of players still object on principle. But the structural case for the market is strong and durable. A $205 billion industry built on 3.6 billion mostly-adult players, fed by games engineered to manufacture time pressure, will keep generating demand for services that sell time back to the people who no longer have enough of it. The grey-area side gig has become a real industry — and the conditions that built it are still building.

Frequently Asked Questions

How big is the game boosting industry in 2026?

There is no single authoritative figure, and dedicated “boosting market” reports vary wildly in quality. What is well-established is the context: a ~$205 billion global games market with 3.6 billion players (Newzoo), within which boosting has matured from informal deals into a structured, platform-based service category widely described in industry commentary as worth billions.

Why has game boosting grown so much?

Three structural forces: an aging, higher-income player base that values time, live-service game design that creates time-limited rewards and seasonal pressure, and a supply side that professionalized into trustworthy platforms. Together they widen the gap between what games offer and what time-constrained players can reach alone.

Is game boosting legal?

Boosting is a service in which one player helps another; it is not illegal. It is governed by each game's terms of service rather than by law, and the risk profile depends heavily on the method — self-play and duo formats keep account access private, while piloted play does not.

Which games drive the most boosting demand?

Titles with heavy endgame time costs and large active bases: World of Warcraft: Midnight leads by volume, followed by ARC Raiders, Diablo 4 and Path of Exile 2. All share content that gates desirable, often time-limited rewards behind coordinated play.